The most remarkable events affecting the capital base in 2011 were as follows:

- The acquisition of 24.9% of the Turkish bank Garanti in March at a cost of €4,391m, which implies a reduction in core capital consumption figures compared with those of 2010.

- The deduction in the third quarter of the investment made to subscribe the capital increase by CNCB.

- In the fourth quarter of 2011, takes place the publication by the European Banking Authority (EBA) of new capital recommendations applicable to certain financial institutions in Europe, aimed at recovering investor confidence in their solvency. This recommendation consists of a minimum core capital ratio of 9% (using the specific criteria defined by the EBA), including an additional exceptional and temporary coverage for exposure to sovereign debt, which will have to be achieved by June 2012.

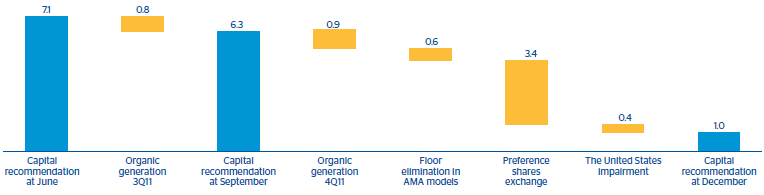

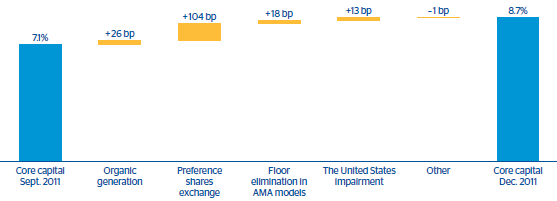

- For the BBVA Group, and according to estimates made in October using the information from June 2011, this recommendation would be met with €7.1 billion. The Group’s strategy to reach the recommended capital is based on the following fundamental pillars: organic generation of capital quarter by quarter; management of capital instruments; and, to a lesser extent, compliance with the forecast timetable for implementing the internal models approved by the Bank of Spain. With data for the close of September, the figure fell to €6.3 billion, of which €2.3 billion correspond to sovereign exposure. The reduction of the initial figure was mainly due to organic capital generation in the third quarter of 2011. As a result of this and with an additional €5.3 billion generated in the fourth quarter of the year, as of December 31, 2011, BBVA had met 84% of the EBA recommendation. In the first half of 2012, the Group’s organic generation of capital will cover the remaining amount. This will allow BBVA to meet with ease the core Tier I ratio (according to EBA criteria) of 9% by June 2012.

- Those €5.3 billion obtained in the fourth quarter of 2011 were originated primarily from the organic generation in the period and the successful completion of the exchange of preference shares for mandatory convertible bonds into BBVA shares, which are 100% eligible as core capital. The exchange was subscribed by nearly all the investors, at 98.7% of the nominal amount, or a total of €3.4 billion. There were also two additional positive effects: the tax deduction from the goodwill impairment in the United States, and the elimination of the capital floor in the advanced measurement approach (AMA) models of operational risk. This floor was established in December 2009 when the internal operational risk models for Spain and Mexico entered into force.

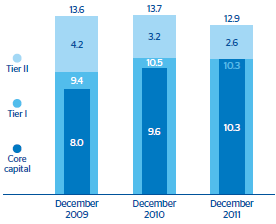

As a result of the above, the capital base according to BIS II standards also substantially improved its quality over the year as a whole. As of December 31, 2011, core capital stood at €34,161m, 13.5% up on the figure for December 2010. The core ratio went up to 10.3% (9.6% as of 31-Dec-2010).

Tier I capital increased by €4,064m over the year, a rise of 12.3%. The Tier I ratio stood at 10.3% (10.5% as of 31-Dec-2010), a year-on-year fall of 24 basis points, due to the rise in risk-weighted assets (RWA) from the acquisition of Garanti.

Other eligible capital (Tier II) at the same date, which includes subordinate debt, surplus generic provisions, eligible unrealized capital gains, and the deduction for holdings in financial and insurance entities, was down 13.1% over the last 12 months to €8,609m. The fall is mainly due to the investment in CNCB mentioned above, the fall in unrealized capital gains resulting from the market turmoil, and the amortization of a subordinated debt issue. As a result, Tier II stood at 2.6% as of 31-Dec-2011 (3.2% as of 31-Dec-2010).

The capital brings the capital base to €42,770m, 0.4% down on the previous year, when payment for the acquisition of 24.9% of Garanti had not been made.

Risk-weighted assets (RWA) amounted to €330,771m, an increase of 5.6% on the figure for December 2010, basically due to the acquisition of Garanti, and to the slight growth in lending over the year, above all in Mexico and South America. The entry into force of the tighter Basel 2.5 requirements (increased RWA for market risk when including stressed VAR) was offset by a lower operational risk requirement due to the elimination of the capital floor in the advanced models.

Finally, the BIS II ratio as of 31-Dec-2011 stood at 12.9% (13.7% as of December 2010).