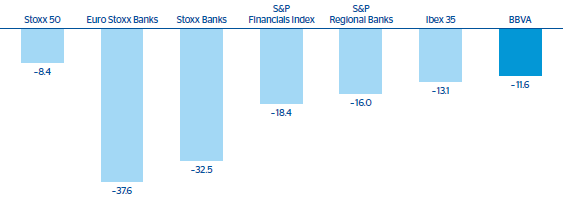

The macro-global context in 2011 was very complicated, and this became even more evident in the second quarter: there was a fall in confidence indicators, an increase in the likelihood of risk scenarios in Europe, a downward review of the growth projections for developed economies and, unlike in 2010, a contagious effect was observed towards emerging economies, though they remain very dynamic. This was all reflected in the performance of the stock market indexes in the different regions. In the United States, the S&P 500 remained flat, while the Stoxx 50 in Europe fell 8.4% as compared to the close of 2010. In Spain, the Ibex 35 fell back 13.1%.

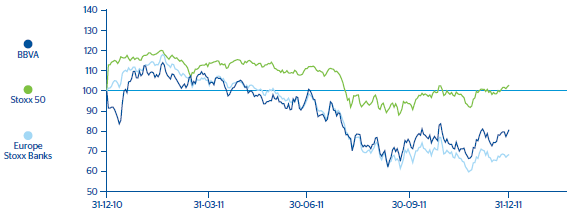

In 2011, BBVA shares achieved a clear outperformance with respect to the sector and demonstrated the best performance of its peers in Europe

The sovereign debt crisis in Europe has infected the financial sector, as it raised concerns about banking solvency, financial tensions and risk premiums. In this context, the sector has had to face fragmented markets and liquidity pressures, which have made their financing more difficult and costly. As a result, the Stoxx Banks and the Euro-Stoxx Banks in Europe fell by 32.5% and 37.6%, respectively, while the S&P Financials Index and the S&P Regional Banks index in the United States dropped 18.4% and 16.0%, respectively.

BBVA earnings 2011 figures have, in general, been favorably received. Analysts pointed out the Group’s solvency and good liquidity position, which will comfortably comply with the EBA’s capital recommendations as of the end of June 2012. They also praised its resilient earnings, with a strong emphasis on the growing course of the most recurrent-type earnings, thanks to the dynamism of activity in emerging markets. By business area, Mexico and South America were quite noteworthy, as was the Group’s competitive position and the stability of the risk indicators in Spain. Furthermore, the increased contribution from Eurasia was also positively viewed.

BBVA continues to be an attractive investment

Therefore, the market took the Entity’s distinguishing factors into consideration. Thus, BBVA recorded an 11.6% loss in the year, while the Eurostoxx Banks index fell by 32.5%. In sum, in the current environment of macroeconomic weakness and difficult access to financing sources, the market positively valued the profile of BBVA’s results, its diversification via emerging markets, the strength of its retail franchise, as well as its comfortable position in terms of liquidity and capital.

BBVA’s share price varied between €5.03 and €9.49, closing at €6.68 per share on 31-Dec-2011, giving a market capitalization of €32,753m. This resulted in a price/book value of 0.8x and a P/E ratio (calculated on the Group’s 2011 net attributable profit) of 10.9x.

BBVA continues with its differential shareholder remuneration policy

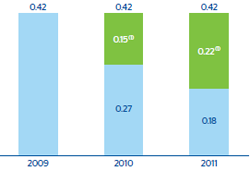

Shareholder remuneration corresponding to 2011 stood at €0.42 per share, remaining at the same level as in recent years and maintaining the current dividend scheme: two cash dividend payments of €0.10 per share were made; moreover, the distribution of €0.10 per share was carried out as part of a system of flexible remuneration called the “dividend option”, for which more than 91% of the Bank’s shareholders opted. A proposal will also be made to the Annual General Meeting (AGM) in relation to the payment of a final dividend of €0.12 per share. This dividend will imply an increase in the payout ratio, which stood at 49% (excluding one-offs) as compared to the 37% of the previous year, and a dividend yield (calculated according to the average dividend per share estimated by analysts for 2011 and the share price as of December 30) at 6.3%, one of the most attractive in the sector. It is worth noting that BBVA not only offers attractive and differential shareholder remuneration, but also renders shareholders a variety of exclusive products and services in very advantageous conditions.

Capital ownership remains well diversified

At the close of 2011, the number of BBVA shareholders stood at 987,277, compared with 952,618 on 31-Dec-2010, a new 3.6% increase. The only significant individual stake that BBVA is aware of is that of the company Inveravante Inversiones Universales, which as of December 31, 2011 held 5.05% of the Group’s shareholders’ equity. It is worth highlighting that in 2011, shareholder dispersion was practically maintained: as of December, 90.6% of the shareholders held less than 4,500 shares (compared to 92.7% as of December 31, 2010), representing 13.0% of the share capital (compared with 12.6% as of 12-31-2010) and an average investment per shareholder of 4,966 shares (4,714 in 2010).

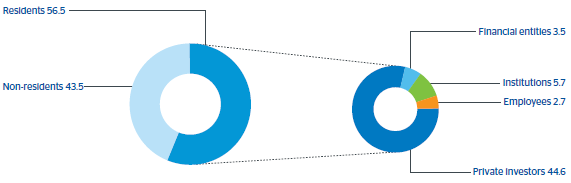

A total of 56.5% of the Group’s shareholders’ equity belongs to residents in Spain. In terms of type of shareholder, 44.6% of the share capital belongs to private investors (40.5% the previous year), 2.7% to employees and the remaining 9.2% to institutional investors. Therefore, the percentage of non-resident shareholders stands at 43.5%, which once again reflects the confidence in and recognition of the BBVA name in the current difficult environment.

As in 2010, the shares were traded on the continuous market in Spain, on the New York Stock Exchange (as ADSs represented by ADRs) and also on the London and Mexico stock markets.

The BBVA share was traded on each of the 256 days in the stock market year of 2011. A total of 15,406 million shares were traded on the stock exchange in this period, representing 314.2% of the Groups’ shareholders’ equity. Thus the daily average volume of traded shares was 60 million, 1.23% of the total number of shares and an effective daily average of €452 million.

Finally, BBVA shares were included in the Ibex 35 and Euro Stoxx 50 reference indexes, with a 10.02% weight in the former and 2.34% in the latter, as well as in several banking industry indexes, most notably the Stoxx Banks, with a weighting of 5.96% and the Euro Stoxx Banks, with a weighting of 13.77%. BBVA is also present in the market’s leading sustainability indexes, such as the Dow Jones Sustainability, FTSE4Good and the various MSCI indexes, among others.