Risk management in insurance business is based on five fundamental elements:

- Identification, calculation, monitoring and management of the risks of the products offered by the Group’s insurance companies, as well as anticipation of such risks in newly commercialized products.

- The methodology used to measure this kind of risks is validated at the corporate level and has been designed according to similar principles to those used in the banking activity.

- Inclusion of the risk premium into product prices as the first step in contributing to the solvency of the business.

- Limits and controls are also established in line with the target risk profile of BBVA, while adapting to the specific features of insurance products in order to preserve solvency and recurrent business earnings.

- A risk overview that takes into account the reporting needs and the requirements of the Group’s business units and of the different regulators in the countries in which business is carried out.

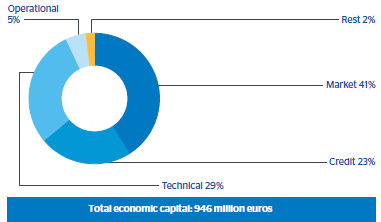

Economic capital in insurance activity in 2011 stood at €946m, a similar figure to the previous year’s one. Market risk represented 41.0% of the total economic capital, technical risk accounted for 29.3%, credit risk for 23.4% and operational risk for 5.4%.