Exposure at default (EAD) is another of the inputs required to calculate expected loss and capital. It is defined as the outstanding debt pending payment at the time of default.

A contract’s exposure usually coincides with its outstanding balance, although this is not always the case. For example, for products with explicit limits, such as cards or credit lines, exposure should include the potential increase in the outstanding balance from a reference date to the time of default.

The EAD is obtained by adding the risk already drawn on the operation to a percentage of undrawn risk. This percentage is calculated using the CCF, which is defined as the percentage of the undrawn balance that is expected to be used before default occurs. Thus the EAD is estimated by calculating this conversion factor. In addition, the relevance of adding to EAD the possibility of using an additional percentage of the limit for transactions that exceed it on a reference date is assessed, according to the risk policy of each product.

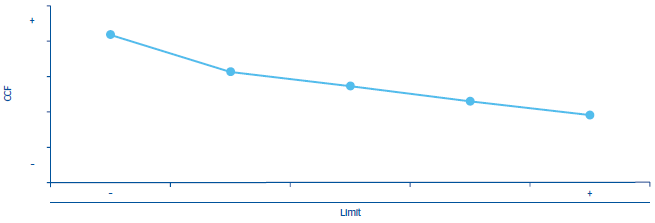

The estimate of these conversion factors also includes distinguishing factors that depend on the characteristics of the transaction. For example, in the case of BBVA Spain credit lines, the conversion factor is estimated based on the amount of the line’s limit and the initial usage percentage, which is defined as the ratio between current risk and limit. Chart 15 shows the CCF for credit lines based on their limit, in such a way that a reverse relationship can be seen between the limit and the conversion factor.

In order to obtain CCF estimations for low-default portfolios, the LDPs, external studies and internal data are combined, or behavior similar to other portfolios is assumed and their CCFs compared.