In 2011, BBVA Bancomer achieved earnings figures that set it apart from its main competitors.

Net interest income reached €3,827m, up 7.2% on the previous year, thanks to greater business volumes and proper price management. This offsets the effect of low interest rates and the reduced contribution from wholesale banking and asset management. In terms of profitability, net interest income over average total assets demonstrated great stability during the year.

Fee and commission income remained at the same level as the previous year, at €1,194m, as the performance of asset management fees (investment companies and pension funds) was able to offset the less favorable evolution of banking fees, influenced by regulatory changes.

The situation of the financial markets, especially in the last part of the year, led to lower brokerage revenues. Consequently, as of December 31, 2011, NTI dropped to €302m (down 20.9% year-on-year). Finally, other income and expenses totaled €227m, up 31.0% year-on-year, boosted mainly by the insurance business. As a result, gross income reached €5,550m, 4.3% higher than the figure for 2010.

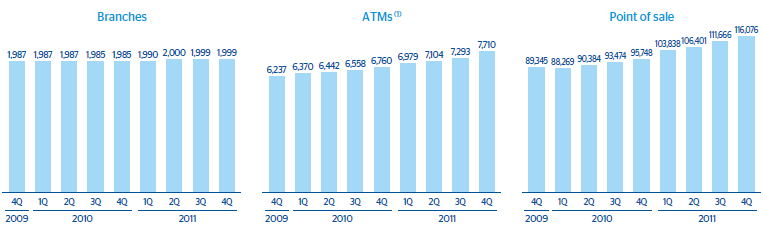

BBVA Bancomer continues to take advantage of the opportunities of the Mexican market through the development of its expansion plan, which was launched in March, 2010. The plan entails a significant investment effort in innovation, technology and infrastructure, being the main reason for the 9.4% year-on-year increase of operating expenses to €2,012m. In 2011, BBVA Bancomer’s distribution network grew by 14 branches, 950 ATMs and more than 20,300 POS. The efficiency ratio stood at 36.2%, confirming that BBVA Bancomer is one of the most efficient banks in the Mexican banking system.

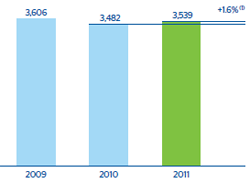

With this evolution of revenues and expenses, operating income reached €3,539m, 1.6% above 2010 figure.

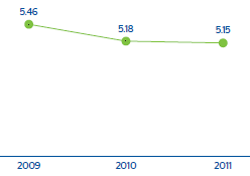

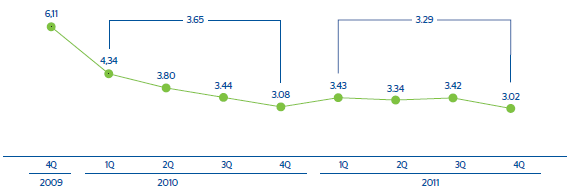

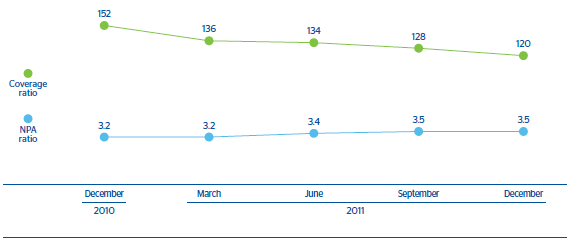

Lending growth has been accompanied by proper risk management. This has enabled impairment losses on financial assets to remain at similar levels to those of the previous year and the cumulative risk premium to improve by 36 basis points in the year to 3.29%. The NPA and coverage ratios closed the year at 3.5% and 120%, respectively. The reduction in the coverage ratio is due to the early termination of the Federal Government’s Punto Final program in January 2011. The program provided support for mortgage debtors affected by the 1994 crisis through discounts granted by the Federal Government and banks. The application of a discount by the Federal Government is repayable in equal amounts over 5 years, while the discount corresponding to BBVA Bancomer represents a reduction in the reserves associated with the discount. The result of this has been a fall in the balances of the housing portfolio (1.5% of the total outstanding portfolio as of 31-Dec-2010), with its respective associated income.

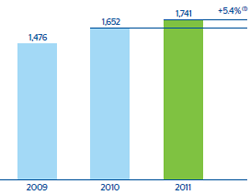

As a result of the above, the area’s net attributable profit reached €1,741m, 5.4% up on the previous year. BBVA Bancomer closed 2011 with a ROE of 21% (according to local accounting criteria), making it one of the most profitable entities in the Mexican banking system.

Banking Business

The banking business in Mexico generated a net attributable profit of €1,426m in 2011 (up 5.6% year-on-year).

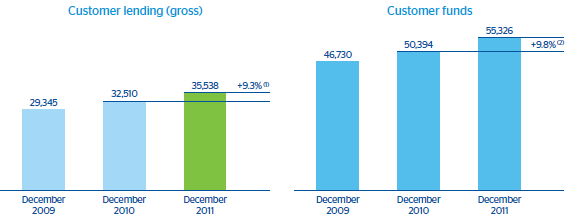

BBVA Bancomer continues to take advantage of market opportunities and, through an adequate commercial management strategy, it recorded €35,538m gross lending to customers (excluding the old mortgage portfolio) as of December 31, 2011, up 9.3% year-on-year. The figure was mainly boosted by the retail portfolio. Wholesale lending was affected by specific events that limited its growth. These include the Federal Government prepayment of a credit line underwritten with a number of banks in the country; and the substitution of existing loans with new wholesale financing carried out by large corporations due to the lower interest rates.

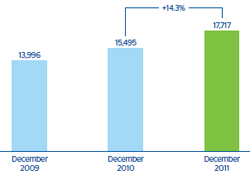

The retail portfolio performed strongly and grew 14.3% year-on-year as of December 31, 2011 to €17,717m. It includes consumer finance, credit cards, individual mortgages and loans to small businesses.

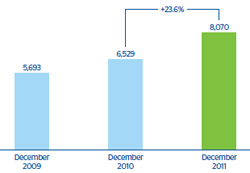

Within the retail portfolio, consumer finance (including credit cards) grew 23.6% to €8,070m. On the one hand, a significant increase in consumer loans (car, payroll and personal) was observed. This has allowed the placement of new loans to record a 16.3% increase in the last twelve months. On the other hand, credit cards also rose 15.0% to €4,486m. This dynamism enabled BBVA Bancomer to maintain its leadership position in this lending segment, with a market share above 35% (figures as of December 2011).

BBVA Bancomer’s extensive expertise in the mortgage market enabled it to grant the largest number of new mortgages of all banks and Sofoles (one out of every three). Thus, the bank granted more than 32,900 individual mortgages in the country. As of December 31, 2011, this represented a year-on-year increase of 13.2% in new production and, therefore, a mortgage loan balance (excluding the old mortgage portfolio) of €8,234m.

At the same time, the wholesale portfolio, which includes loans to corporations, SMEs, financial institutions and the public sector, rose 3.7% over the figure of 2010. By segment, loans to corporations were up 6.2% to €6,371m, loans to SMEs went up 14.8%. Finally, loans to the public sector increased by 10.4% to €3,316m.

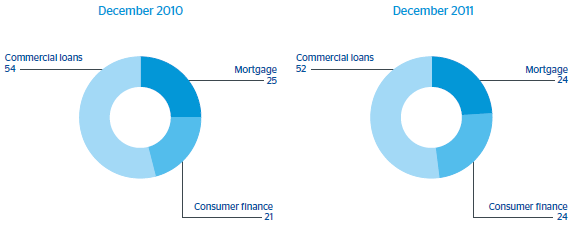

The above explains the gradual shift in the structure of the loan portfolio over the year towards a more profitable composition. In this regard, the weight of consumer loans grew from 21% in 2010 to 24% in 2011, while mortgage loans represented 24% of the total in 2011 and the commercial portfolio, the largest in volume, accounted for 52% as of the close of the year.

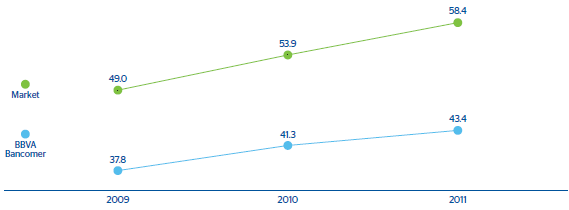

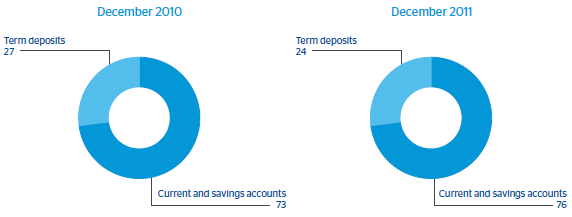

Customer funds (bank deposits, repos, mutual funds and investment companies) closed at €55,326m on December 31, 2011, with a year-on-year increase of 9.8%. The increase in the gathering of demand deposits was noticeable (10.0% year-on-year), up to €55,326m as of December 31, 2011. A profitable mix is also maintained on the liability side, since 76% of customer deposits are low-cost funds. BBVA Bancomer continues to hold the largest market share in demand deposits, with 30% as of December 2011 (latest data available) according to information from the CNBV (the National Banking and Securities Commission). In terms of off-balance-sheet funds, mutual funds’ performance has been excellent, reaching a balance of €15,612m as of December 31, 2011, with a year-on-year increase of 11.0%.

BBVA Bancomer, through an autonomous management model that is independent of the parent company, maintained adequate liquidity and solvency levels. In this regard, more than 118,000 million pesos were issued over the year. To ensure adequate capital management, BBVA Bancomer made a capital notes issue on the international markets of $2,000m. Thus, the total capital ratio stood at 15.8% (according to local accounting standards) at year end.

Finally, BBVA Bancomer, achieved the third place out of 55 companies in the “Most sustainable bank” ranking, due to its community involvement in Mexican society. This award is granted by the Inter-American Development Bank (IDB) and covers the areas of environmental sustainability, social responsibility and corporate governance. Likewise, BBVA Bancomer holds the third place out of 86 participating companies in the list of the most transparent companies according to the “Transparency and Corporate Sustainability Index in Mexico”.

Below are some of the most important aspects of the performance of the various business units in 2011:

Commercial Banking

Commercial Banking has a broad distribution network that has allowed productivity to rise by 14.4% in 2011. This unit manages a loan-book of €6,160m and total customer funds of €34,451m. During 2011, Commercial Banking launched numerous innovative products and services that have, among other effects, boosted the banking penetration process in the country. It is worth mentioning: Movimiento PYME (SME movement) for small companies; Micronegocios (Microenterprise) card, supported by Nacional Financiera (Mexico’s Development Bank) guarantees; “Cuenta Express”, the first account linked to the customer’s mobile phone that does not require a minimum balance to be opened and permits all types of basic financial transactions to be made by phone quickly, easily and securely; Hipoteca Selecta (Exclusive Mortgage) to help customers buying a home; and the B+28 Fund, which invests in short-term debt instruments with an automatic rollover clause and monthly availability of funds. In addition, BBVA Bancomer has received numerous prizes and awards. On the one hand, it was again awarded with the “SME 2011” prize by the Secretary of the Economy for being the financial institution supporting the highest number of microenterprises and SMEs in the country. On the other hand, Standard & Poor’s rating agency confirmed its classification as an Excellent mortgage administrator, the highest possible rank.

Consumer Finance Unit

This unit, which basically manages the Bank’s consumer and credit card portfolio, has been growing steadily and enabled the Bank to maintain a market share above 36% as of the end of 2011. The boost of lending through alternative channels other than branches carried out this year had an impact on the high percentage of new loans granted through these channels, accounting for 15% of the global amount. This unit thus encourages a multi-channel approach, which allows for an increase in product distribution options, customer loyalty and efficiency in the process of opening and approving loans. This approach also helps to maintain very positive risk indicators, since the unit grows primarily through granting loans to customers already known by the Bank. The alliance with car financing entities contributed to an increase in loans for purchasing vehicles. In this regard, as of December 31, 2011, more than 97,000 loans of this type were granted. This unit also manages payroll loans and personal loans.

Government & Corporate Banking

This unit has a specialized network of 85 branches for companies and 37 for public sector clients, and manages a loan-book of €8,320m. The corporate segment reached 8,238 customers, 16% more than in 2010, and granted more than 1,000 new loans to customers who did not have asset products. Thanks to this, a total of 21% of the customers in the unit already had at least one investment product by the end of 2011. Likewise, new collection solutions were offered by increasing the number of terminals for companies and for regions, states and cities to help the government with its tax collection.

In order to strengthen the leasing business, BBVA Bancomer acquired FacilLeasing, a Mexican leasing company with more than 23,000 vehicles for lease and more than 5,000 million pesos in assets.

Corporate and Investment Banking

In 2011, this unit completed the integration of the Corporate & Investment Banking and Global Markets team under a new model allowing revenues to increase through better cross-sectional business management. Moreover, this unit was very active in the innovation of products and services fitting the needs of its customers. Thus, in 2011, it launched a new product called “Bancomer Net Cash”, which provides a global online banking solution for corporate clients, businesses and governments, as it integrates various solutions designed to streamline their administrative tasks, payments and collections and cash management. It also launched the “ETF CHNTRAC” fund in Mexico, allowing customers to invest in China, a country with a huge growth potential and one of the largest economies in the world. This makes BBVA Bancomer the second most important player in Latin America in ETF’s since 2009.

Pensions and Insurance business

In 2011, the pensions and insurance business generated a net attributable profit of €317m (up 5.2% year-on-year).

In the pensions sector, Afore Bancomer continues to perform extremely well, leveraged on a stable labor market. As a result of the good management of business activity, it closed the year with assets under management of €13,132m, up 12.1% year-on-year, and with a 4.4% growth in fund gathering. Both variables are key to achieving increased income from fees and commissions (which rose 6.7% on 2010) and a net attributable profit of €76m. This latter figure is very positive (up 5.1% year-on-year), considering the instability and volatility of the financial markets worldwide throughout 2011.

Commercial performance in the insurance business in 2011 was very positive. It is worth mentioning the uptake on the ILP (Free Wealth Investment), the solid performance of the “Creditón Nómina” loan and “HogarSeguro” and “VidaSegura Preferente” insurance, as well as the progress made in “AutoSeguro” boosted by the campaign carried out in the first months of the year. The new “Auto Alerta” product is an outstanding example of technological innovation. It uses GPS to report accidents, by simply pressing a key on a mobile telephone. The reduced level of claims in the car and life insurance branches favorably contributed to earnings in 2011.