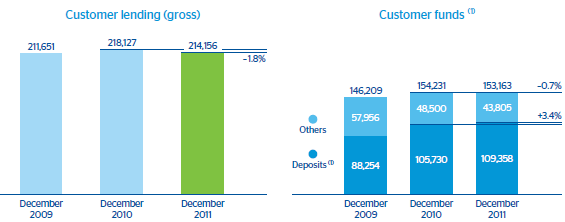

In the aforementioned macroeconomic and sector context that has taken place during 2011, BBVA Spain closed on December 31, 2011 with a gross lending to customers balance of €214,156m, which implies a lower decrease than that of the market (–1.8% in BBVA vs.

–3.2% in the sector). However, the yield increased by 13 basis points since the last quarter of last year.

In terms of customer funds (deposits, mutual funds and pension funds, as well as promissory notes), a total of €153,163m were managed. In the year, BBVA achieved a significant increase in market share in current and savings accounts in households and corporates of 12 basis points up to 9.7%. In addition, the area has improved its positioning in stable resources on the balance sheet with a share increase of 11 basis points in the aggregate of time deposits and promissory notes since the beginning of the year.

In off-balance-sheet funds, the Group manages €19,598m in mutual funds in Spain, which corresponds to a market share of 15.3%. Assets under management fell by 12.2% in the last twelve months. This figure is lower than the one recorded by the entire market, due to BBVA’s greater weight in more conservative products. In terms of pension funds, BBVA pension fund manager remains in the leading position in Spain, with a share of 18.9% as of 31-Dec-2011 and assets under management of €17,224m.

It is worth noting that in December BBVA successfully closed the exchange of preferred securities for mandatory subordinated bonds convertible into newly issued ordinary shares of BBVA. The acceptance of the offer among investors was 98.7%, amounting to a total of €3,430m. The successful uptake of this operation and others reveals the great capillarity of the BBVA network, the trust of its customers in BBVA and the mutual commitment between them and the Bank.

Stable quarterly figures for net interest income and other revenue, the high level of efficiency, and competitive advantages in terms of asset quality with respect to the sector as a whole, have all characterized earnings for the area in 2011.

A combination of loan repricing, the greater weight of current and savings accounts, the high proportion of time deposits renewed at prices adjusted to the degree of customer bundling, and risk selectiveness have resulted in a net interest income for the year of €4,399m

(–9.8% year-on-year). This was achieved despite the last six months of the year being characterized by more expensive wholesale funding and the loss of asset values as a result of market difficulties.

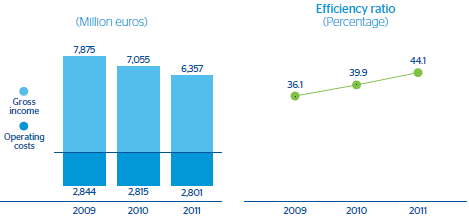

Furthermore, fees and commissions, at €1,468m, were down 12.2% during the year in an environment of pressure from the financial markets influencing the fees linked to mutual funds, reduced M&A activity in the corporate sector, and discounts to ensure greater customer loyalty. The good performance of the insurance business did not offset the adverse performance of NTI in the period, which was hit by the economic situation, the low level of activity in Wholesale Banking and the fall in asset prices. Overall, the resilience of net interest income and the positive performance of the insurance business, balanced against the negative performance of other income, have resulted in accumulated gross income of €6,357m.

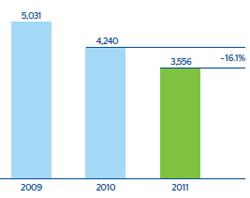

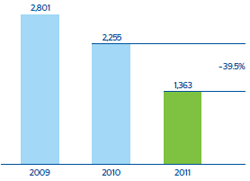

The area’s operating expenses stayed contained and amounted to €2,801m in 2011. This marked a year-on-year fall of 0.5%, despite the fact that its number of branches remained practically the same, unlike its competitors. As a result, the efficiency ratio stood at 44.1%, which stands out against the rest of the sector. Operating income reached €3,556m (€4,240m in 2010). The above reflects, on one hand, the resilience of the area’s recurrent revenues in a year plagued by economic and financial difficulties. And, on the other hand, it reveals it has room to meet the needs for loan-loss provisioning, with impairment losses on financial assets at €1,711m, representing 48% of the operating income.

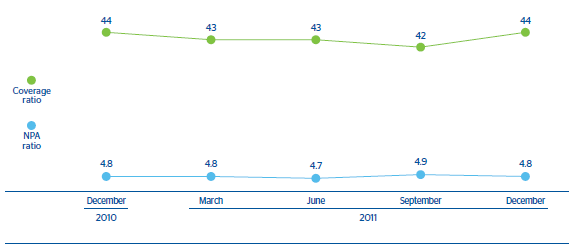

Another competitive advantage with respect to its sector is BBVA’s asset quality in Spain, with a very stable NPA ratio of 4.8% as of 31-Dec-2011, notably lower than the 7.6% figure for the market average. There was practically no increase of asset impairments over the year in the area, while in the system as a whole the ratio was up 180 basis points. The coverage ratio closed at the same levels as the previous year, at 44%. The practically stable volume of distressed assets is due to a moderation of gross additions with an increase of recoveries.

In all, the area’s net attributable profit for the year amounted to €1,363m.

Retail and Commercial Banking

This unit includes the Retail Network, with the household customers, private banking, small companies and retailer segments in the Spanish market; Corporate and Business Banking (CBB), which handles the needs of the SMEs, corporations, public sector and developers; and other businesses, among which is BBVA Seguros.

As of December 31, 2011, this unit managed loans and receivables of €190,817m, 2.8% lower than the amount recorded on December 31, 2010. This is due, in large part, to the reduction of positions in the greater risk groups. However, BBVA’s commitment to its customer base resulted in a new market share gain in households and companies with less risk. Balance sheet funds managed, including promissory notes, stood at €99,455m, up 2.2% on the previous year. Thus there is a clear improvement in the unit’s liquidity gap.

Within the Retail Network, lending closed 2011 with a balance of €102,158m (down 4.0% year-on-year). Customer deposits (including promissory notes) stood at €77,114m (up 4.0%).

Commercial activity worth mention in the unit includes:

- BBVA, anticipating the effects of the crisis, has been implementing a range of financial solutions since 2008 designed to resolve the financial problems of 47,000 families, by adapting to their capacity to pay.

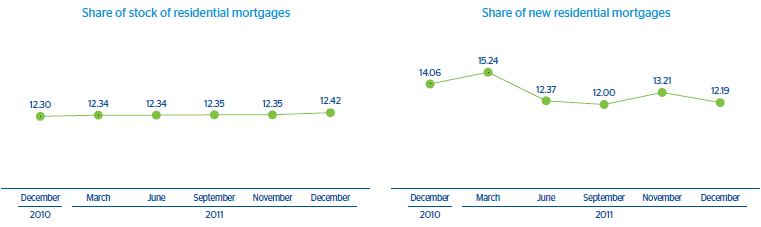

- When compared to the market, the Bank presents positive progress in residential mortgage lending, which has allowed the managed stock of mortgages to remain stable and gain 12 basis points in the market share (November data, latest available) in the year.

- In 2011, two new “Quincenas de Cuentas Abiertas” (Open Account Fortnights) were carried out that allowed access to a promotional gift for opening deposits, setting up a direct deposit for payrolls and pension payments, taking out consumer loans and pension plans, in addition to deposits funds and lending. A total of 399,333 gifts were given, and €1,183m in funds were gathered.

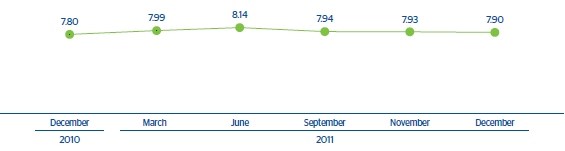

- In time deposits, the market share in households increased 9 basis points in the year to 7.9%.

- Also outstanding were the “Pagarés de Banco de Financiación” promissory notes that, since their launch in September, invoiced €2,381m.

- ICO Funds totaling €814m were placed to SMEs and the self-employed segments in 27,600 transactions through the agreements made with the ICO. This put BBVA in second place as issuer of this type of institutional loan.

- Agreements were renewed with: the National Association of the Self-Employed (ATA), with 450,000 members; the National Federation of Lottery Associations (ANAPAL) with more than 5,000 members; the Spanish Modern Hotel and Catering Association (FEHRCAREM) with more than 3,000 franchises; the Spanish Retail Confederation (CEC) with 450,000 members; IAC Automoción, with 1,500 members; and the Union of Tobacconists (UAEE), with 11,000 affiliates.

- In the retail trade segment, the new campaigns both to attract new customers and maintain the loyalty of existing ones have focused on the “Bono TPV” and “transactional” offers. Thanks to the solid efforts of the sales force, excellent earnings were recorded, with a year-on-year increase in point-of-sale turnover of 8.1%.

- Commercial actions for the capture of new cooperatives as customers stood out in the agricultural sector. The number of agricultural entities in the client base rose to 900 as of December 31, 2011, with a business volume of €145m.

As a result of its customer focus, this unit gained 488,000 new customers in 2011 and increased the degree of loyalty of its existing customers. This was demonstrated in the 3.5% increase in the number of products per customer and the increased weight of the non-basic customer.

Several relevant projects were carried out in 2011, including:

- Internet: whose objective is to digitize BBVA relations with its customers in order to reach its goal of 2 million active Internet users by December 2012. Currently, more than 4,000 customers register every day for the BBVA Internet service.

- “BBVA Contigo”: a pioneer, innovative remote management service designed for customers demanding personalized consulting to complement the use of remote channels, such as the Internet, phone or ATMs. BBVA already has more than 230 specialized consultants and 185,000 customers who have chosen this relationship model. The objective for 2012 is to make this initiative universal.

- Within the Means of Payment, several actions have been carried out to reinforce BBVA’s leadership position, by increasing the invoicing volumes in the main business lines and, especially, in prepayment services, which was up 6.4% year-on-year. Likewise, in order to boost its position as reference Bank for companies and the self-employed segment, BBVA launched a new range of company credit cards that, while simplifying its current range, meets the needs of this segment. The year 2011 marked the culmination of the migration process for the credit card stock to EMV (Europay Mastercard Visa) chip, and an important effort was made in process improvement by enabling new channels, like mobiles phones, ATMs and the Internet for requesting and managing the cards. Finally, at the end of 2011, BBVA revolutionized the market with the launch of the new contactless payment cards that provide customers with speed, security and innovation.

- Within the Multichannel banking unit, BBVA was able to increase online customer support functionalities, with the incorporation of new tax and receipts modules, descriptive videos, social networks, alerts area, etc. The contracting systems have been simplified and mobile device developments have continued. These efforts led Apple to select “BBVA Móvil” as the first Spanish bank highlighted in the Apple Store. Finally, ATMs have undergone major improvements, making their use easier and incorporating the option to receive statements and confirmations through SMS or email.

- BBVA’s Contact Center, in its commitment to quality, continues to offer the highest standards of service in the market. It was granted awards for “Efficiency and Speed in Telephone Banking” and “Business Intelligence in Customer Service” at the 2nd Contact Center Awards, in addition to the “CRC GOLD” for collections management.

- Finally, the complete self-service relationship model at BBVA, provided through Uno-e, developed a new range of products on its website and has transformed telephone customer service, enabling it to end the year with a positive balance sheet.

CBB unit manages lending of €88,173m and customer deposits including promissory notes totaling €21,602m. The following are the most important points in this respect in 2011:

- Supporting Spanish companies was a priority. BBVA did so primarily using two vehicles: commercialization of ICO lines, as well as collaboration with the Official Credit Institute (ICO) in the dissemination and development of ICO Directo, and with the European Investment Bank (EIB), through a new Public Sector line. BBVA has, for another year, played a key role as one of the most active banks in the distribution of various ICO credit facilities, with the conclusion of 31,745 transactions for a total of €2,393m, a market share of 12.7%.

- In terms of working capital, BBVA marketed factoring assignments of €12,920m and accounts payable advances and deferments for €14,109m, thus consolidating its leadership position in this business.

- In the corporate segment BBVA also maintains a leading position with large companies, with a penetration share of 67.5% and a 27% market share as the leading financial supplier (according to the FRS-Inmark-2011 report). Within SMEs (corporate entities with a turnover of under €50m and more than 10 employees), the penetration share is 34% and the share as leading financial provider stands at 12.1%, according to the same sourc.

- In corporations, BBVA is the absolute market leader, with 96.7% of the penetration share. It is the primary or reference bank for the most customers thanks to its outstanding service and the customer-relationship model that defines this group.

BBVA private banking serves customers with more than €300,000 in liquid assets and also encompasses the wealth management unit (Patrimonios) for customers/family groups with more than €2m available. In 2011, BBVA increased its number of customers by 1% by virtue of greater consulting and its exclusive range of products: portfolios managed and advised, exclusive funds in the segment, third-party funds, personalized structure, Visa Infinite, etc. BBVA private banking was also recognized, for the second consecutive year, as the best private bank in Spain in the 2011 Global Private Banking Awards, held annually by The Banker, the prestigious Financial Times Group magazine specializing in international banking. This year, BBVA Private Banking remained the leading entity in terms of assets under management with more than €2,700m (11.2% market share), pertaining to 290 SICAVs.

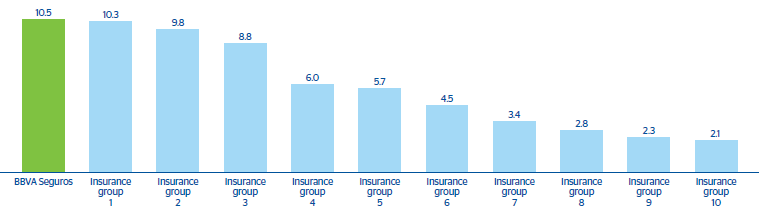

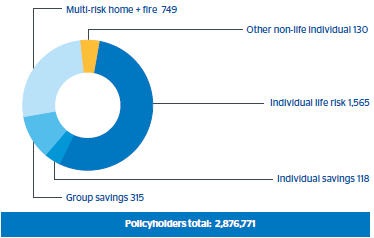

The Insurance unit comprises several companies with the strategic objective of becoming the leader in the insurance business among the different BBVA customer segments. It manages an extensive range of insurance products through direct insurance, brokerage and reassurance, using different networks. In terms of activity, BBVA Seguros written premiums in 2011 reached €1,877m (up 73% year-on-year). Of that, 1,354m correspond to the positive course of the insured savings business (up 178% year-on-year), especially as regards the growth of the company insurance schemes that, with €464m of written premiums (up 152% year-on-year), has become a clear reference in this market. As a result, the volume of funds under management in insurance savings policies amounted to €8,792m (up 8% year-on-year). BBVA Seguros remained the market leader in individual life and accident insurance policies, with a market share of 10.5% as of September (latest available figure), after issuing €288m. The level of activity in the non-life business has been maintained, after writing premiums for €236m (up 2% year-on-year). The unit has also brokered premiums for other companies for €161m.

In order to increase pension savings solutions for its customers, BBVA Seguros has broadened its product catalog with the launch of PPA (insured pension plan income schemes): an accumulation PPA, with the objective of saving capital for retirement based on an insured yield, and in which the premiums contributed are deductible on the taxable base of individual income tax; and income PPA, which allows the savings customers have accumulated up to their retirement in other PPAs or PPIs (Individual Pension Plan) to transform into monthly life annuities. Likewise, two new issues were made, for 15 and 36 months, for the Europlazo product, a mixed life-savings deferred capital insurance product. Also, in order to boost the capture of new insurance policy holders and to reward their loyalty, the “Seguros Remunerados BBVA” (Remunerated Insurance BBVA) line was launched. It offers a range of life, home and temporary disability insurances that give money back to customers while the policy is in effect. Through it, they can even earn a 25% discount after three years.

The unit achieved more than 2.8 million policyholders, with an increased quality of service, as reflected by the complaint-free resolution of more than 96% of life insurance claims reported and the complaint-free resolution of 99% of home insurance policies. Periodic independent measurements granted the home insurance policies a score of 7.6 out of 10 for service received during the claims process.

Wholesale Banking

This unit manages the business with large corporations and multinational groups in the domestic market through Corporate and Investment Banking, and the activity of Global Markets in the same geographical area, with their trading floor business and distribution. It is a customer base with diversified business and high cash flows from other countries. BBVA is able to offer a full range of products and services, supported by its extensive international presence.

In Spain, at the end of the year Wholesale Banking managed a loan book of €23,339m and on-balance-sheet customer funds (not including repos) of €9,903m, a growth of 7.2% and 18.3%, respectively, on the close of the previous year. This unit continues to focus strongly on customers with the highest levels of loyalty, profitability and credit quality; therefore, the portfolio is characterized by a low NPA level and low provisioning needs.

The most significant aspects of earnings are as follows:

- Resilient recurrent revenue in the unit (net interest income plus fees): the figure for the year as a whole is very similar to 2010, at €945m. Specifically, in WB&AM this revenue was up 3.3% in the last 12 months.

- The current economic situation, the low level of business and the fall in asset prices in general, explain the negative NTI for the year, although it is less negative than the figure for 2010.

- As a result, the gross income of €921m is 1.3% under the figure for the close of 2010. However, it is worth highlighting the favorable performance of gross income in the WB&AM unit, which was up 7.2% year-on-year, and the positive trend in customer revenue in Global Markets, particularly in those businesses that are strategic for the unit, such as credit.

- Year-on-year growth in operating expenses was 8.0%, explained by the investment project underway; as a result, the operating income was down 7.2% year-on-year to €532m.

- Impairment losses on financial assets were stable and net attributable profit at the close of 2011 came to €363m (€397m in 2010).