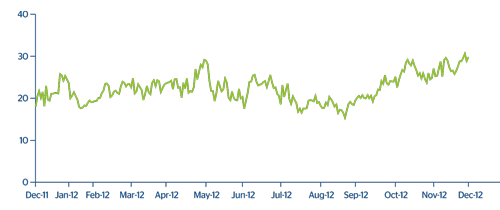

The Group’s market risk remains at low levels compared with the aggregates of risks managed by BBVA, particularly in terms of credit risk. This is due to the nature of the business and the Group’s policy of minimal proprietary trading. In 2012, the market risk of the Group’s trading book decreased on the previous year to an average economic capital of €242m.

34 BBVA Group. Market risk evolution in 2012

(VaR, million euros)

The main risk factor in the Group continues to be linked to interest rates, with a weight of 72% of the total at the end of 2012 (this figure includes the spread risk). Equity risk accounts for 5%, a decrease on the figure 12 months prior. The exchange-rate risk also decreased its weight slightly to 5%. Finally, the volatility risk increased and accounts for 18% of the total portfolio risk.

BBVA Group. Market risk by risk factor in 2012

(Million euros)

Download Excel

Download Excel

| VaR by risk factor | Interest/ Spread risk |

Currency risk |

Stock-market risk | Vega/ Correlation risk | Diversification effect (*) | Total |

|---|---|---|---|---|---|---|

| Average VaR |

|

|

|

|

|

22 |

| Maximum VaR | 35 | 2 | 3 | 11 | (21) | 31 |

| Minimum VaR | 21 | 3 | 1 | 11 | (21) | 15 |

| End-of-period VaR | 35 | 3 | 3 | 9 | (19) | 30 |

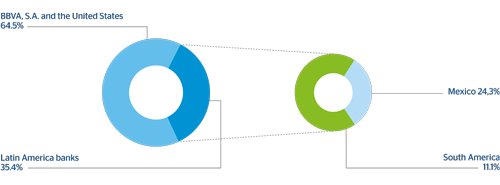

By geographical areas, and as an annual average, 64.5% of the market risk corresponded to the BBVA, S.A and The United States trading floors and 35.4% to the Group’s banks in Latin America, of which 24.3% is in Mexico.

35 BBVA Group. Market risk by geographical area

(Average 2012)

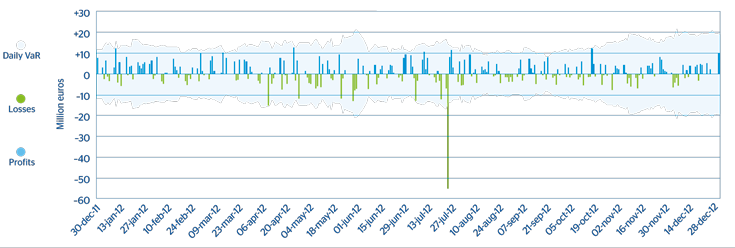

The backtesting comparison performed with market risk management results for the parent company (which accounts for most of the Group’s market risk) follows the principles set out in the Basel Accord. It makes a day-on-day comparison between actual risks and those estimated by the model, and proved that the risk measurement model was working correctly throughout 2012 (Chart 36).

36 BBVA, S.A. internal backtesting model in 2012

(Estimated VaR without smoothing versus daily results)