PD is a measure of credit rating that is assigned internally to a customer or a contract with the aim of estimating the probability of non-compliance within a year. It is obtained through a process using scoring and rating tools.

Scoring

These tools are statistical instruments designed to estimate the probability of default according to features of the contract-customer binomial. They are focused on management of retail credit: consumer finance, mortgages, credit cards of individuals, corporate loans, etc. There are different types of scoring: reactive, behavioral, proactive and bureau.

The main aim of reactive scoring is to forecast the credit quality of loan applications submitted by customers. It attempts to predict the applicant’s probability of default if the application were accepted (applicants may or may not be BBVA customers at the time of application).

The level of sophistication of the scoring model and its capacity to adapt to the economic context enables it to give more accurate customer profiles and improve the Bank’s capacity to identify different levels of creditworthiness within specific groups (young people, customers, etc.). The result is a significant improvement in the discrimination capacity of tools in groups of particular interest to the business.

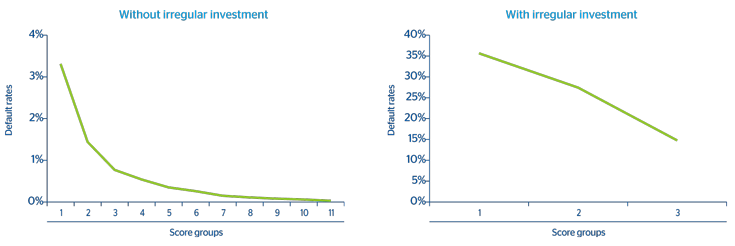

The accompanying charts 5 and 6 show the default rates of some of the reactive scoring tools used by the Group.

5 BBVA Spain consumer finance tool calibration

(Default rates for the domestic customer segment, excluding young people and refinancing, based on scoring and irregular investment) (1)

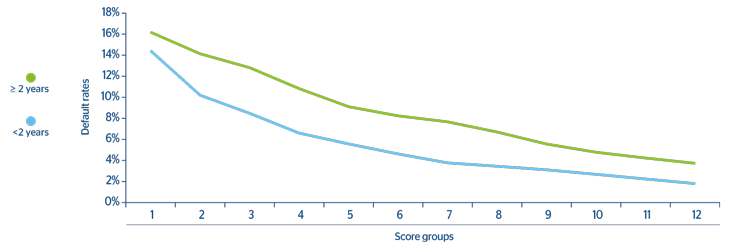

6 Reactive scoring tool calibration for Autos Finanzia, BBVA Spain

(Based on score and original term of the transaction)

They show how different axes can serve to assess the risk of a retail-type transaction. Chart 5 presents the different one-year consumer default rates of BBVA Spain based on scoring and irregular investment for the domestic customer segment, excluding young people and refinancing. Chart 6 presents the different default rates for transactions granted for a period of less than 2 years and those for 2 years or more in BBVA Spain Autos Finanzia. As expected, the highest probabilities of default are observed for transactions granted for a longer term.

A distinguishing feature of reactive scorings is that the default rates of the various segments tend to converge over time. In BBVA, this loss of screening capacity is mitigated by combining reactive with behavioral and proactive scorings.

Behavioral scoring is used to review contracts that have already been formalized by incorporating information on customer behavior and on the contract itself. Unlike reactive scoring, it is an analysis, i.e. once the contract has been granted. It is used to review credit card limits, monitor risk, etc., and takes into account variables directly linked to the transaction and the customer that are available internally: the behavior of a particular product in the past (delays in payments, default, etc.) and the customer’s general behavior with the Entity (average balance on accounts, direct debit bills, etc.).

Proactive scoring tools take into account the same variables as behavioral scorings, but they have a different purpose, as they provide an overall ranking of the customer, rather than of a specific transaction. This customer perspective is supplemented by adjustments that depend on the type of product. The availability of proactive scorings has enabled the Group to monitor customers’ credit risk more precisely, to improve risk screening processes and to manage the portfolio more actively by offering credit facilities adapted to each customer’s risk profile.

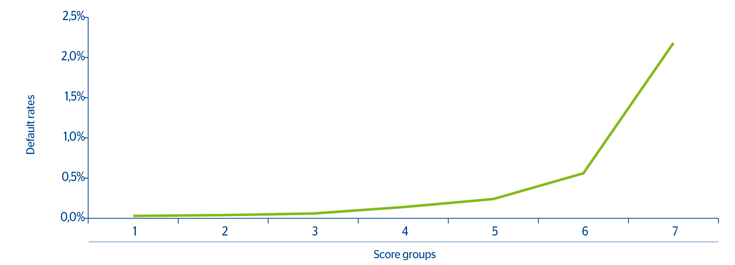

Chart 7 presents the probability of default curves of the proactive scoring tool for BBVA Spain mortgages in the domestic “positive experience” segment with low loyalty, and excluding refinancing, according to the score. The “positive experience” segment covers customers with good payment behavior over the previous 24 months and with loyalty to the Bank. Chart 8 depicts the behavioral scoring for BBVA Bancomer credit cards.

7 Proactive scoring tool calibration for mortgages of individuals in BBVA Spain

(Default rates for the domestic “positive experience” segment with low loyalty, excluding refinancing, based on scoring)

8 Credit card behavioral scoring tool calibration, BBVA Bancomer

(Default rates by score)

The so-called bureau scoring models, widely used in the Americas, are also of great importance. This kind of tool is similar to the scorings explained above, except that while the latter are based on the Bank’s internal information, bureau scoring requires credit information from other credit institutions or banks (on default events or customer behavior). In countries with positive bureau information, existing external and internal information is combined. This information is provided by specialized agencies that compile data from other entities. Not all banks collaborate in supplying this information, and usually only participating entities have access to it. In Spain, the Bank of Spain’s Risk Information Center (CIRBE) makes such information available. Bureau scorings are used for the same purpose as the other scorings: i.e. authorizing transactions, setting risk limits and monitoring risk.

An adequate management of the reactive, behavioral, proactive and bureau tools by the Group means that updated risk parameters can be obtained and are adapted to economic reality. This results in precise knowledge of the credit health of transactions and/or customers. This task is particularly relevant in the current economic situation, as it makes it possible to identify the contracts or customers that are in difficulties, and thus take the necessary measures to manage risks that have already been assumed.

Rating

These tools focus on wholesale customers: companies, corporations, SMEs, the public sector, etc. In such cases, default events are predicted at the customer level rather than at the contract level.

The risk assumed by BBVA in the wholesale customer portfolio is classified in a standardized way by using a single master scale in economic terms for the whole Group that is available in two versions: a reduced one with 22 degrees and an extended one with 34. The master scale allows discrimination amongst credit quality levels, taking into account geographical diversity and the different types of risk in the different wholesale portfolios in the countries where the Group operates.

The information provided by the rating tools is used when deciding on accepting transactions and reviewing limits.

Some of the wholesale portfolios managed by BBVA are low default portfolios, in which the number of default events is low (sovereign risks, corporations, etc.). To obtain PD estimates in these portfolios, the internal information is supplemented by external data, mainly from external rating agencies and the databases of external suppliers.

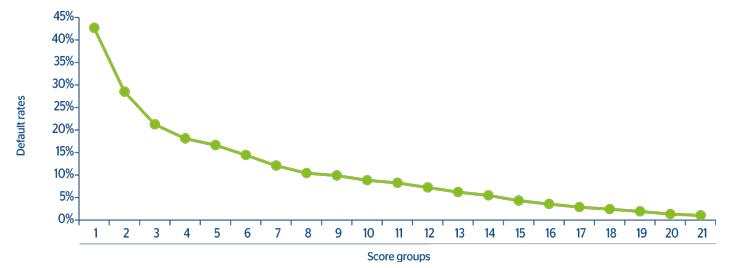

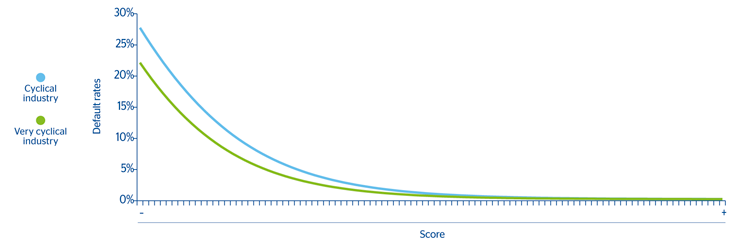

There are different axes that permit the risk of different customers to be assessed. Chart 9 is an example of a rating tool calibration curve for BBVA Spain companies based on the internal scoring assigned and the sector groups, which show a different cyclicality.

9 Rating tool calibration for BBVA Spain companies

(Default rates based on score and sector groups, with different cyclicality)

The economic cycle in PD

The current economic crisis has revealed the importance of a proper anticipation in risk management. In this context, excess cyclicality of risk measurements has been identified as one of the causes of the instability of the metrics of financial institutions. BBVA has always been committed to estimating average cycle parameters that mitigate the effects of economic-financial turbulence in credit risk measurement.

The probability of default varies according to the cycle: it is greater during recessions and lower during expansions. In general, financial institutions do not have internal information on defaults covering a sufficiently long period of time to serve as an observation of the behavior of portfolios over a complete cycle. That is why adjustments have to be made to the internal data. The adjustment process to translate the default rates observed empirically into average default rates is known as cycle adjustment. The cycle adjustment uses sufficiently long economic series related to the default of portfolios, and their behavior is compared with that of the default events in the Entity’s portfolios. Any differences between past and future economic cycles may also be taken into account, thus resulting in a certain prospective approach.

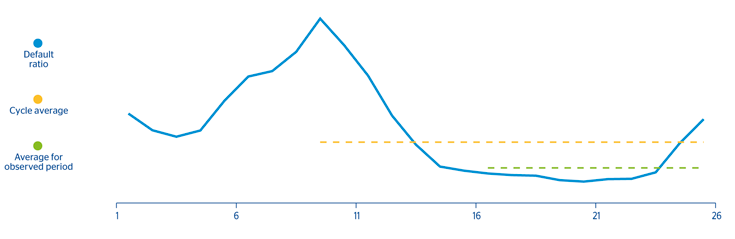

10 Cycle adjustment mechanism

Chart 10 illustrates how the cycle adjustment mechanism works. It shows the hypothetical evolution of a series of default events over a sufficiently long period of time to be considered to include at least one economic cycle. The cycle adjustment model used by BBVA extrapolates the performance of this series of default events to internal data, based on the relationship between the series over one entire cycle and the observation period.