Net interest income

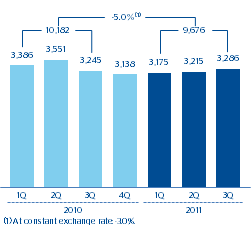

The Group’s quarterly net interest income continues to show great resilience. Between July and September 2011, it totaled €3,286m, 1.3% up on the same period last year and 2.2% above the figure for the previous quarter. This is the result

of increased business in emerging markets, as well as the appropriate management of spreads in developed countries as volumes of business fall. The figure year to date is €9,676m.

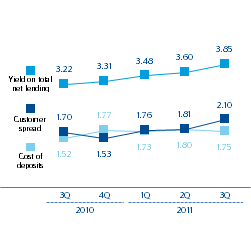

In business with customers in the domestic sector of the euro area, yield on loans was up again in the third quarter of 2011 by 19 basis points to 3.50%, while the cost of funds slowed its rise significantly, and increased by only 8 basis points to 1.72%. As a result, the customer spread was up 11 basis points on the figure for the second quarter of 2011 to 1.78%. This improvement practically offsets the effects of lower lending and more expensive wholesale funding.

| Net interest income (Million euros)  |

Customer spread. Euros domestic sector (Percentage)  |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Breakdown of yields and costs (Million euros) |

||||||||||||||

|

|

3Q 11 |

|

2Q 11 |

|

1Q 11 |

|

4Q 10 |

|

3Q 10 | |||||

|

|

% of ATA |

% yield/ Cost |

|

% of ATA |

% yield/ Cost |

|

% of ATA |

% yield/ Cost |

|

% of ATA |

% yield/ Cost |

|

% of ATA |

% yield/ Cost |

| Cash and balances with central banks | 3.8 | 1.19 |

|

3.6 | 1.25 |

|

3.7 | 1.30 |

|

4.0 | 1.17 |

|

4.2 | 0.99 |

| Financial assets and derivatives | 25.4 | 2.87 |

|

24.3 | 2.98 |

|

24.4 | 3.03 |

|

25.2 | 2.75 |

|

26.0 | 2.61 |

| Loans and advances to credit institutions | 4.4 | 2.88 |

|

5.3 | 2.35 |

|

4.5 | 2.23 |

|

4.7 | 1.97 |

|

4.2 | 2.14 |

| Loans and advances to customers | 59.7 | 5.62 |

|

60.3 | 5.42 |

|

61.2 | 5.24 |

|

59.9 | 4.89 |

|

59.5 | 4.86 |

| Euros | 38.4 | 3.50 |

|

39.2 | 3.31 |

|

40.0 | 3.25 |

|

39.5 | 3.12 |

|

39.0 | 3.12 |

| Domestic | 33.1 | 3.85 |

|

34.0 | 3.60 |

|

35.4 | 3.48 |

|

35.6 | 3.31 |

|

35.4 | 3.22 |

| Other | 5.2 | 1.31 |

|

5.2 | 1.41 |

|

4.6 | 1.43 |

|

3.9 | 1.48 |

|

3.6 | 2.10 |

| Foreign currencies | 21.3 | 9.44 |

|

21.1 | 9.33 |

|

21.3 | 8.98 |

|

20.4 | 8.31 |

|

20.5 | 8.19 |

| Other assets | 6.7 | 0.45 |

|

6.4 | 0.37 |

|

6.1 | 0.44 |

|

6.2 | 0.46 |

|

6.1 | 0.43 |

| Total assets | 100.0 | 4.29 |

|

100.0 | 4.19 |

|

100.0 | 4.12 |

|

100.0 | 3.79 |

|

100.0 | 3.73 |

| Deposits from central banks and credit institutions |

14.3 | 2.73 |

|

13.7 | 2.52 |

|

11.3 | 2.68 |

|

12.9 | 2.15 |

|

15.1 | 1.82 |

| Deposits from customers | 48.3 | 2.17 |

|

48.6 | 2.06 |

|

50.6 | 1.77 |

|

48.1 | 1.63 |

|

45.6 | 1.51 |

| Euros | 27.3 | 1.72 |

|

26.6 | 1.64 |

|

28.1 | 1.35 |

|

24.6 | 1.40 |

|

22.5 | 1.23 |

| Domestic | 16.6 | 1.75 |

|

17.7 | 1.80 |

|

17.7 | 1.73 |

|

17.3 | 1.77 |

|

16.6 | 1.52 |

| Other | 10.7 | 1.67 |

|

8.9 | 1.31 |

|

10.5 | 0.72 |

|

7.3 | 0.51 |

|

5.8 | 0.41 |

| Foreign currencies | 21.0 | 2.75 |

|

22.1 | 2.57 |

|

22.4 | 2.28 |

|

23.4 | 1.87 |

|

23.2 | 1.78 |

| Debt certificates and subordinated liabilities | 18.9 | 2.47 |

|

20.3 | 2.27 |

|

20.1 | 2.15 |

|

20.4 | 2.15 |

|

20.6 | 1.95 |

| Other liabilities | 11.7 | 0.99 |

|

10.7 | 1.02 |

|

11.1 | 1.29 |

|

12.3 | 0.64 |

|

12.8 | 0.64 |

| Equity | 6.8 | - |

|

6.7 | - |

|

6.9 | - |

|

6.3 | - |

|

5.9 | - |

| Total liabilities and equity | 100.0 | 2.02 |

|

100.0 | 1.92 |

|

100.0 | 1.77 |

|

100.0 | 1.58 |

|

100.0 | 1.45 |

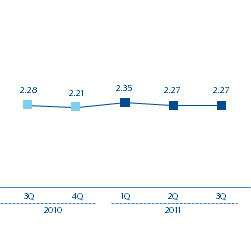

| Net interest income/Average total assets (ATA) | 2.27 |

|

|

2.27 |

|

|

2.35 |

|

|

2.21 |

|

|

2.28 | |

again in the third quarter of 2011 by 19 basis points to 3.50%, while the cost of funds slowed its rise significantly, and increased by only 8 basis points to 1.72%. As a result, the customer spread was up 11 basis points on the figure for the second quarter of 2011 to 1.78%. This improvement practically offsets the effects of lower lending and more expensive wholesale funding.

In Mexico, interbank rates are still low and practically at the same levels as at the close of the second quarter of 2011. The yield on loans has risen by 14 basis points on the figure at the close of the previous quarter, to 13.10%, thanks to the good new production figures, above all in consumer finance and credit cards. Deposit costs increased by barely 5 basis points in the quarter to 1.96%. Thus the customer spread stood at 11.14% at the close of the quarter (11.05% in the first quarter of 2011) and the net interest income year to date in the area is up 6.0% year-on-year at constant exchange rates.

Competitive pressure remains high in South America. However, buoyant business activity means that the net interest income year to date in the area was up 28.4% year-on-year at constant exchange rates.

Net interest income/ATA

BBVA Group (Percentage)

Finally, in the United States net interest income between July and September 2011 remained at similar levels to those of the previous two quarters at constant exchange rates, despite the continued increase in the proportion of lower risk loans, and thus lower yield. The above is the result of continuing good price management by BBVA Compass.