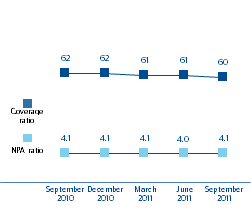

The third quarter of 2011 once more featured stability in the main indicators of credit quality with respect to the close of 2010. The NPA ratio closed at 4.1%, the coverage ratio at 60% and the risk premium for the quarter stood at 1.01%.

As of September 30, 2011, the volume of total risks with customers (including contingent liabilities) totaled €390,723m, which is very similar to the figure from the previous quarter (€391,380m). This flat development is explained in part by the depreciation of the main currencies against the euro (at constant exchange rates, lending fell 0.1% in the quarter) and also by the deleveraging process observed in Spain. This trend might increase in the coming months, though BBVA will be affected to a lesser degree than the system average.

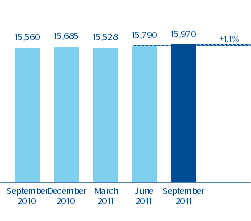

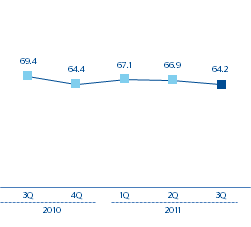

Non-performing loans have remained stable since December 2009 and reached €15,970m. There has been a decrease in new non-performing assets with respect to the previous quarter, as well as in recoveries. The latter, however, is due primarily to the seasonal nature of this period, especially considering the summer vacation period in Spain. Nevertheless, the rate of recoveries over new NPA remains at a solid level (64.2%).

Non-performing assets

(Million euros)

| Credit risk management (1) (Million euros) |

|

|

|

|

|

|---|---|---|---|---|---|

|

|

30-09-11 | 30-06-11 | 31-03-11 | 31-12-10 | 30-09-10 |

| Non-performing assets | 15,970 | 15,790 | 15,528 | 15,685 | 15,560 |

| Total risks | 390,723 | 391,380 | 383,043 | 384,069 | 376,421 |

| Provisions | 9,503 | 9,576 | 9,490 | 9,655 | 9,641 |

| Specific | 6,584 | 6,485 | 6,516 | 6,823 | 6,552 |

| Generic and country-risk | 2,919 | 3,090 | 2,974 | 2,832 | 3,089 |

| NPA ratio (%) | 4,1 | 4,0 | 4,1 | 4,1 | 4,1 |

| NPA coverage ratio (%) | 60 | 61 | 61 | 62 | 62 |

(1) Including contingent liabilities.

| Variations in non-performing assets (Million euros) |

|

|

|

|

|

|---|---|---|---|---|---|

|

|

3Q 11 | 2Q 11 | 1Q 11 | 4Q 10 | 3Q 10 |

| Beginning balance | 15,790 | 15,528 | 15,685 | 15,560 | 16,137 |

| Entries | 2,918 | 3,713 | 2,804 | 3,852 | 3,051 |

| Recoveries | (1,874) | (2,484) | (1,882) | (2,479) | (2,116) |

| Net variation | 1,044 | 1,229 | 922 | 1,373 | 935 |

| Write-offs | (876) | (939) | (1,140) | (1,269) | (1,119) |

| Exchange rate differences and other | 12 | (28) | 61 | 21 | (393) |

| Period-end balance | 15,970 | 15,790 | 15,528 | 15,685 | 15,560 |

| Memorandum item: |

|

|

|

|

|

| Non-performing loans | 15,689 | 15,515 | 15,210 | 15,361 | 15,218 |

| Non-performing contingent liabilities | 281 | 275 | 319 | 324 | 342 |

Recoveries over entries to NPA

(Percentage)

The NPA ratio of the Group stood at 4.1% and remained in a stable range with respect to recent quarters. Broken down by business area, the NPA ratio rose slightly in Spain, Mexico and Eurasia. This variation in Spain is due to the aforementioned decrease in lending, as the NPA as of 30-Sep-2011 remained stable as compared to the figure as of 30-Jun-2011. The United States maintained its downward trend in the NPA ratio, and South America closed another quarter with an improvement of 9 basis points with respect to the figure for June 2011.

Coverage provisions for risks with customers amounted to €9,503m, a very similar figure to that from the second quarter of the year. Of this total, generic provisions reached 2,886m and represented 30.4%.

Finally, the NPA coverage ratio stood at 60%, which is similar to that of the previous quarter. By business area, it stood at 42% in Spain (43% at the end of the previous quarter), it increased to 69% in the United States (67% as of 30-Jun-2011) and improved to 140% in South America (138% as of 30-Jun-2011). In turn, it fell in Eurasia to 118% (144% as of 30-Jun-2011) and to 128% in Mexico (134% as of 30-Jun-2011). Additionally, it is worth noting that 58.9% of the Group’s risks are collateralized.

NPA and coverage ratios

(Percentage)