Report 1Q 2026

BBVA Posts Nearly €3 Billion Profit in the First Quarter (up 11%) and Announces a New Tranche of Share Buybacks

The share

The global economy has shown greater strength than expected during the last months of 2025 given the high levels of uncertainty, trade and geopolitical tensions, and the migration restrictions of the United States administration. The negative effects of protectionist policies and high geopolitical instability would have been mitigated by lower effective tariffs than initially announced, fiscal stimulus and the strong growth in investment in artificial intelligence, particularly in the United States. The expansionary nature of the monetary policy of the Federal Reserve (hereinafter, the Fed), the moderate inflation, and contained energy prices would have also supported global activity.

The conflict in Iran has once again raised uncertainty and geopolitical risk, and has significantly driven up oil and gas prices. Under the assumption that the conflict is resolved in a reasonable short period and tensions in the energy and financial markets progressively moderate, BBVA Research forecasts global growth to stand at 3.2% in 2026, the same figure as in 2025. This expectation of a certain resilience in global activity rests, in part, on the upward revision of the expected growth for the United States by six tenths to 2.5% (in 2025, growth was 2.1%) due to the strong increase in investment in artificial intelligence. In the case of the Eurozone, the forecast of a gradual deceleration in activity is maintained: compared to GDP growth of 1.5% in 2025, in 2026 it could be 1.1%, in a context where the impact of tariffs, political instability in some countries in the bloc, and the rise in energy prices could be partially offset by increased spending on defense and infrastructure. The growth expected for China also remains unchanged: GDP growth in 2026 could stand at 4.5%, compared to 5% in 2025.

It is foreseeable that the rise in tariffs, the strength of demand, and the recent tensions in fuel prices will keep inflation in the United States at around 3% for much of 2026, limiting the Fed's scope for interest rate cuts. Following the cuts in 2025, which brought the benchmark rate to 3.75%, BBVA Research forecasts two additional rate cuts to 3.25%, conditioned, in any case, on the duration of the conflict in Iran and its impact on prices. In the Eurozone, the ECB is expected to keep the deposit facility interest rate unchanged (at 2%) if inflationary pressures subside once the crisis in the Middle East is contained (the headline rate could remain above 2% throughout 2026). In China, monetary conditions are likely to continue to ease given the current context of very low inflation in which it finds itself.

The balance of risks for the global economy remains weighted to the downside, with growing uncertainty following the outbreak of the conflict between the United States, Israel, and Iran. In addition to protectionist measures in trade and immigration, and the structural challenges facing Europe and China, negative factors include increased geopolitical tensions (potential interventions of the United States in Latin America, the Middle East or Greenland) and uncertainty regarding the Fed's independence and its potential impact on financial markets. A sharp increase in the prices of oil, gas, and energy-intensive goods, derived from an escalation of tensions in the Middle East, emerges as a significant source of risk. On a positive note, however, it is worth mentioning the boost in investment in artificial intelligence and its medium-term effect on the productivity of economies that promote its adoption.

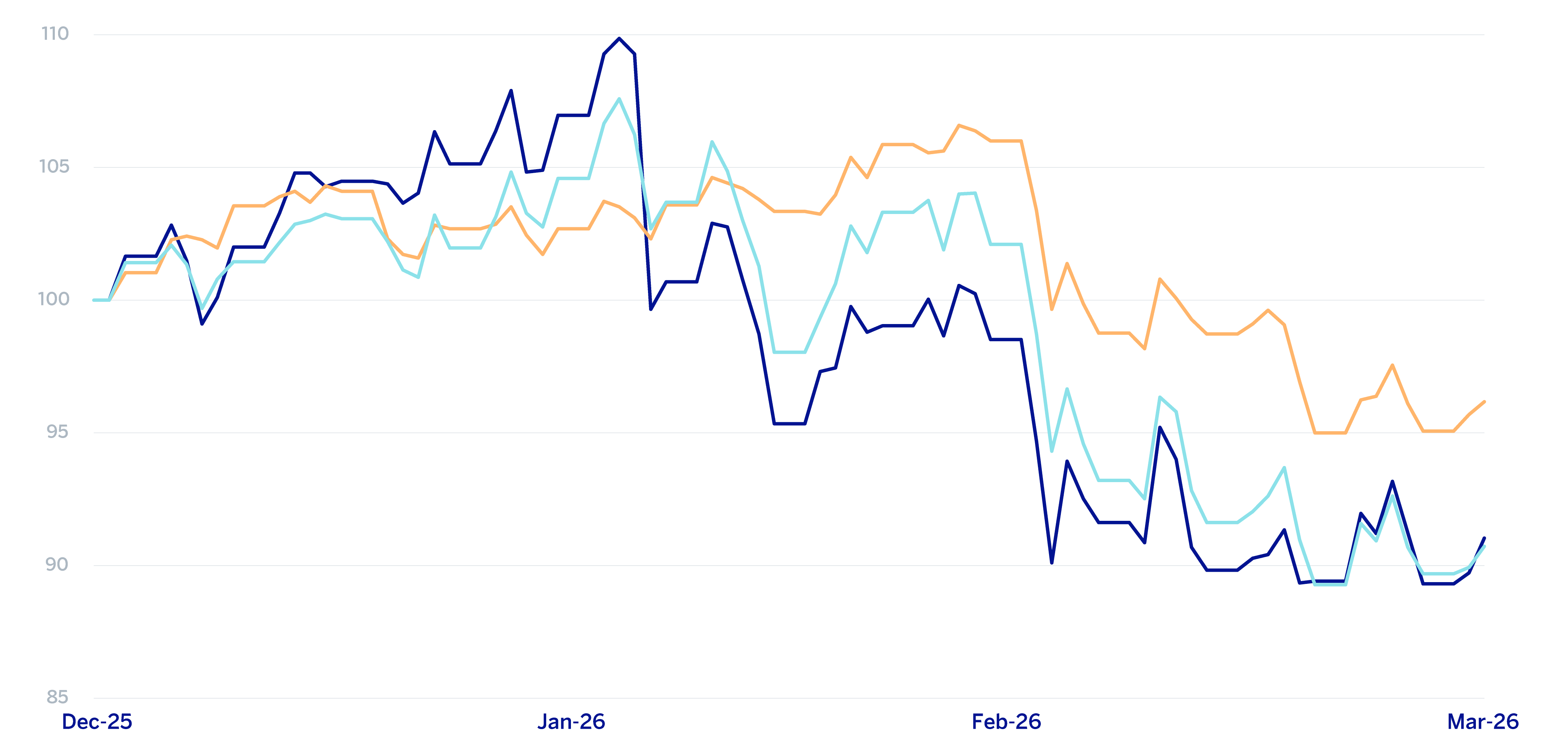

The main indexes have shown a negative performance during the first quarter of 2026. In Europe, the Stoxx Europe 600 index decreased by -1.5% compared to the end of December 2025, and in Spain the Ibex 35 also decreased by -1.5% in the same period. In the United States, the S&P 500 index decreased by -4.6%.

With regard to the banking sector indexes, the performance in the first quarter of 2026 was worse than the general indexes in Europe. The Stoxx Europe 600 Banks index, which includes the banks in the United Kingdom, and the Euro Stoxx Banks, an index of Eurozone banks, decreased by -7.1% and -9.3% respectively, while in the United States, the S&P Regional Banks sector index increased by 0.4% in the period.

The BBVA share price fell by -9.0% during the quarter, underperforming its sector index, closing the month of March 2026 at €18.25.

BBVA share evolution

Compared with European indexes (base indice 100=31-12-25)

BBVA

Eurostoxx-50

Eurostoxx Banks

| THE BBVA SHARE AND SHARE PERFORMANCE RATIOS | ||

|---|---|---|

| 31/03/2026 | 31/12/2025 | |

| Number of shareholders | 660,942 | 657,193 |

| Number of shares issued (millions) | 5,634 | 5,709 |

| Closing price (euros) | 18.25 | 20.05 |

| Book value per share (euros) (1) | 10.10 | 10.19 |

| Tangible book value per share (euros) (1) | 9.57 | 9.69 |

| Market capitalization (millions of euros) | 102,821 | 114,465 |

| (1) For more information, see Alternative Performance Measures at the end of the quarterly report. | ||

Regarding shareholder remuneration, the Annual General Shareholders´ Meeting of BBVA held on March 20, 2026, approved, under item 1.3 of the Agenda, a cash distribution against the 2025 results as a final dividend for the 2025 financial year, for an amount equal to €0.60 gross per outstanding BBVA share entitled to participate in this distribution, which was paid on April 10, 2026. Thus, the total amount of cash distributions for the 2025 financial year, taking into account that in November 2025 a gross amount of €0.32 per share was distributed, stood at €0.92 gross per share.

Total shareholder policy contemplates that cash distributions may be combined with share buybacks, all subject to the authorization and approvals applicable at any given time1.

On March 31, 2026 the number of BBVA shares outstanding was 5,634 million. The number of shareholders reached 660,942 and, by type of investor, 68.48% of the capital belonged to institutional investors and the remaining 31.52% was in the hands of retail shareholders.

BBVA shares are included on the main stock market indexes. At the closing of March 2026, the weighting of BBVA shares in the Ibex 35, Euro Stoxx 50 and the Stoxx Europe 600 index, were 12.1%, 2.6% and 0.9%, respectively. They are also included on several sector indexes, including Stoxx Europe 600 Banks, which includes the United Kingdom, with a weighting of 6.3% and the Euro Stoxx Banks index for the eurozone with a weighting of 10.4%. Moreover BBVA maintains a significant presence on a number of international sustainability indexes, such as, Dow Jones Sustainability Index (DJSI), FTSE4Good or MSCI ESG Indexes.

1 For further information, please refer to the "Share buyback programs" section in the "Capital and shareholders" chapter of the quarterly report.

Group's information

- 2025-2029 Strategic Plan

- Results

- Balance sheet and business activity

- Solvency

- Sustainability

2025-2029 Strategic Plan

In the first quarter of 2026, the BBVA Group has continued to make significant progress in the execution of its 2025-2029 Strategic Plan, which aims to establish a new axis of differentiation by radically incorporating the customer perspective, as well as driving and strengthening the Group's commitment to growth and value creation. Thus, in mid-2025, the Group presented its financial objectives for the period 2025-2028, which are part of the strategic plan presented at the beginning of that same year.

BBVA continues to focus on innovation as a key driver for achieving these goals and continuing to lead the transformation of the sector. Thanks to artificial intelligence and next-generation technologies, the Group amplifies its positive impact on customers, helping them make the best decisions.

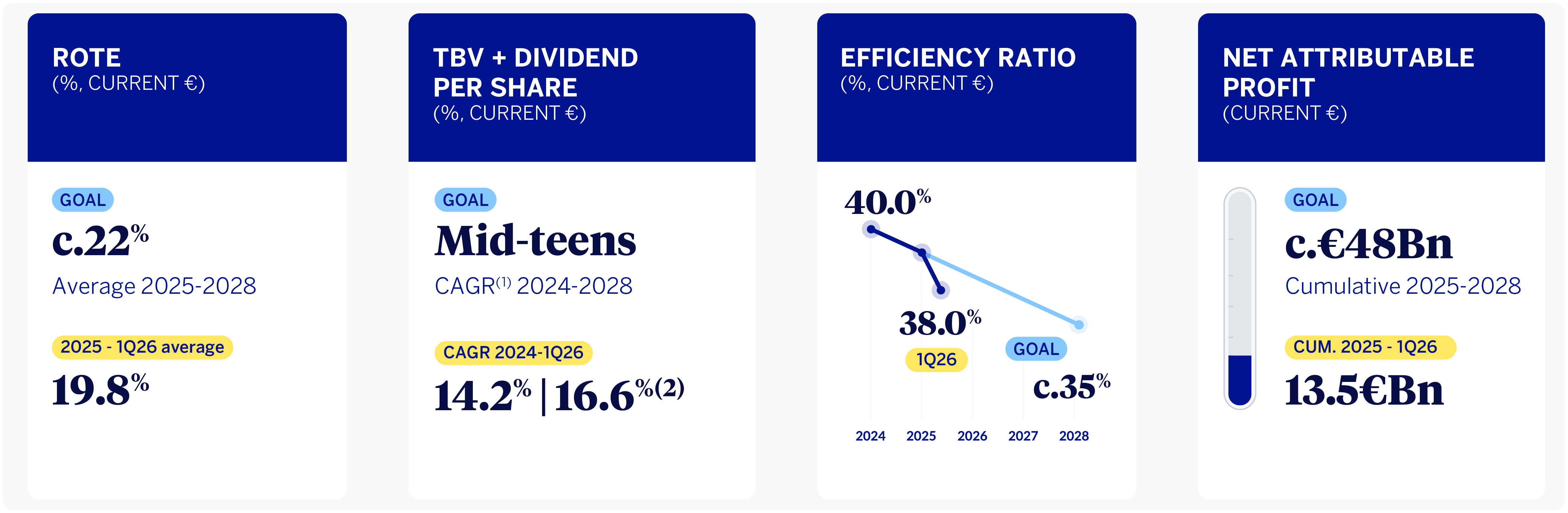

GROUP FINANCIAL KPIS GOALS EVOLUTION

(1) Compound Annual Growth Rate.

(2) Excluding the effect of Share Buybacks.

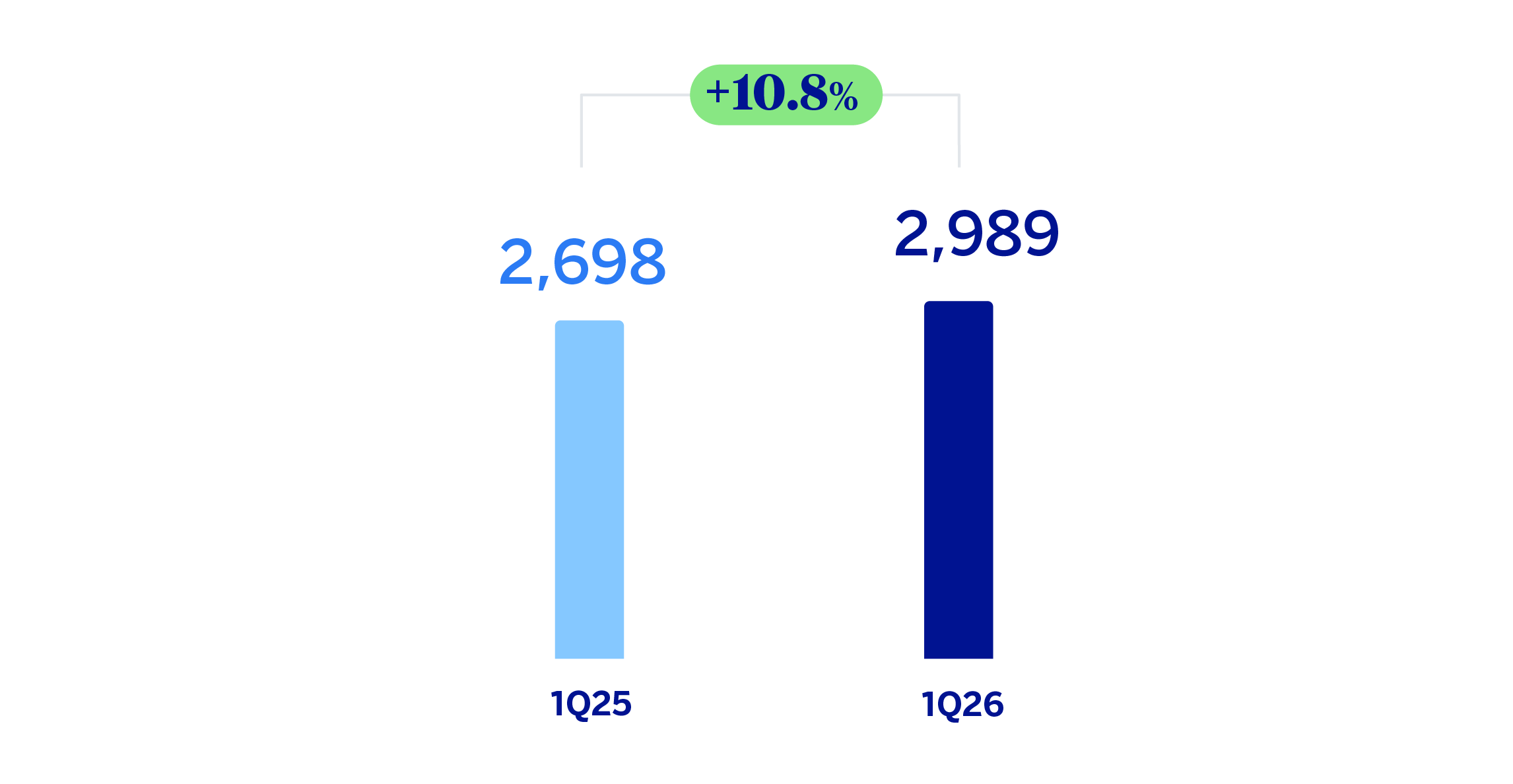

In this context, the BBVA Group achieved a cumulative result of €2,989 million by the end of the first quarter in 2026, representing an increase of 10.8% over the previous year, supported by the strong performance of recurring revenues from the banking business If the exchange rates variation is excluded, this growth increases to 14.1% favored by the solid evolution in gross income, which increased by 18.3% in constant terms, with a growth rate that is higher than that of operating expenses (+17.5% at constant exchange rates, impacted by an environment of still high inflation). As a result of this evolution, the efficiency ratio stood at 38.0% as of March 31, 2026, which represents an improvement of 24 basis points compared to the ratio as of March 31, 2025.

NET ATTRIBUTABLE PROFIT (LOSS) (MILLIONS OF EUROS)

During the first quarter of 2026, loans and advances to customers increased by 4.0%, driven by the dynamism of the wholesale segment. Of particular note within this segment was the higher volume of loans to business, which grew by 5.2% at the Group level. Loans to individuals increased by 2.2%, with consumer loans showing greater dynamism, followed by mortgages.

Customer funds registered an increase of 0.9% so far this year, with slight growth in customer base deposits of 0.5% at the Group level, and 1.5% in off-balance sheet funds.

LOANS AND ADVANCES TO CUSTOMERS AND TOTAL CUSTOMER FUNDS (VARIATION COMPARED TO 31-12-2025)

(1) The growth of non-performing loans and advances to customers under management (excluding repos) stands at 4.6%.

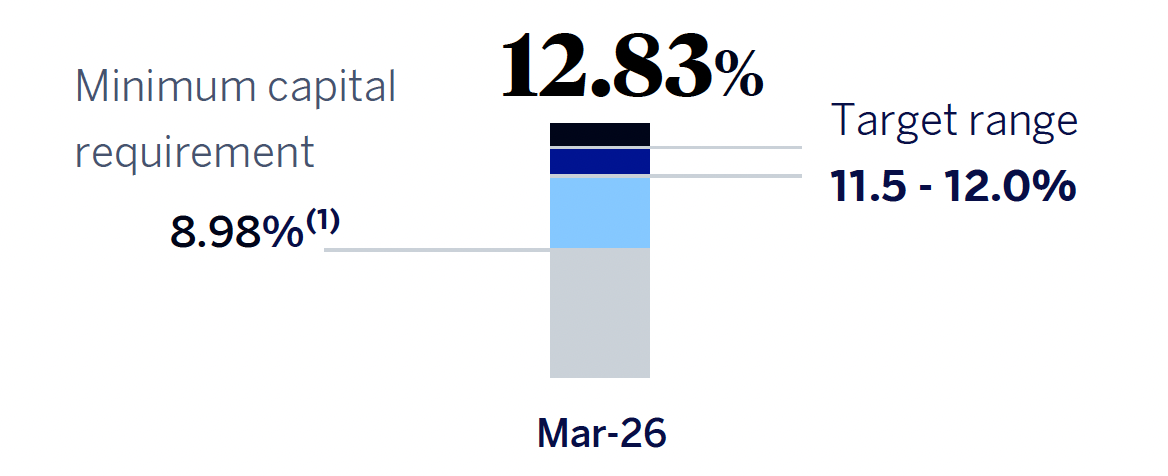

The BBVA Group's CET12 ratio stood at 12.83% as of March 31, 2026, which allows it to maintain a large management buffer over the Group's CET1 requirement as of that date (8.98%3), and is also above the Group's target management range of 11.5% - 12.0% of CET1.

CET1 RATIO

(1) Considering the latest official updates to the countercyclical capital buffer and the systemic risk buffer, applied on the basis of exposure as of December 31, 2025.

2 As of March 31, 2026, there were no differences between fully loaded and phased-in ratios given that the impact associated with the transitional adjustments is nil.

3 Considering the latest official updates to the countercyclical capital buffer and the systemic risk buffer, applied on the basis of exposure as of December 31, 2025.

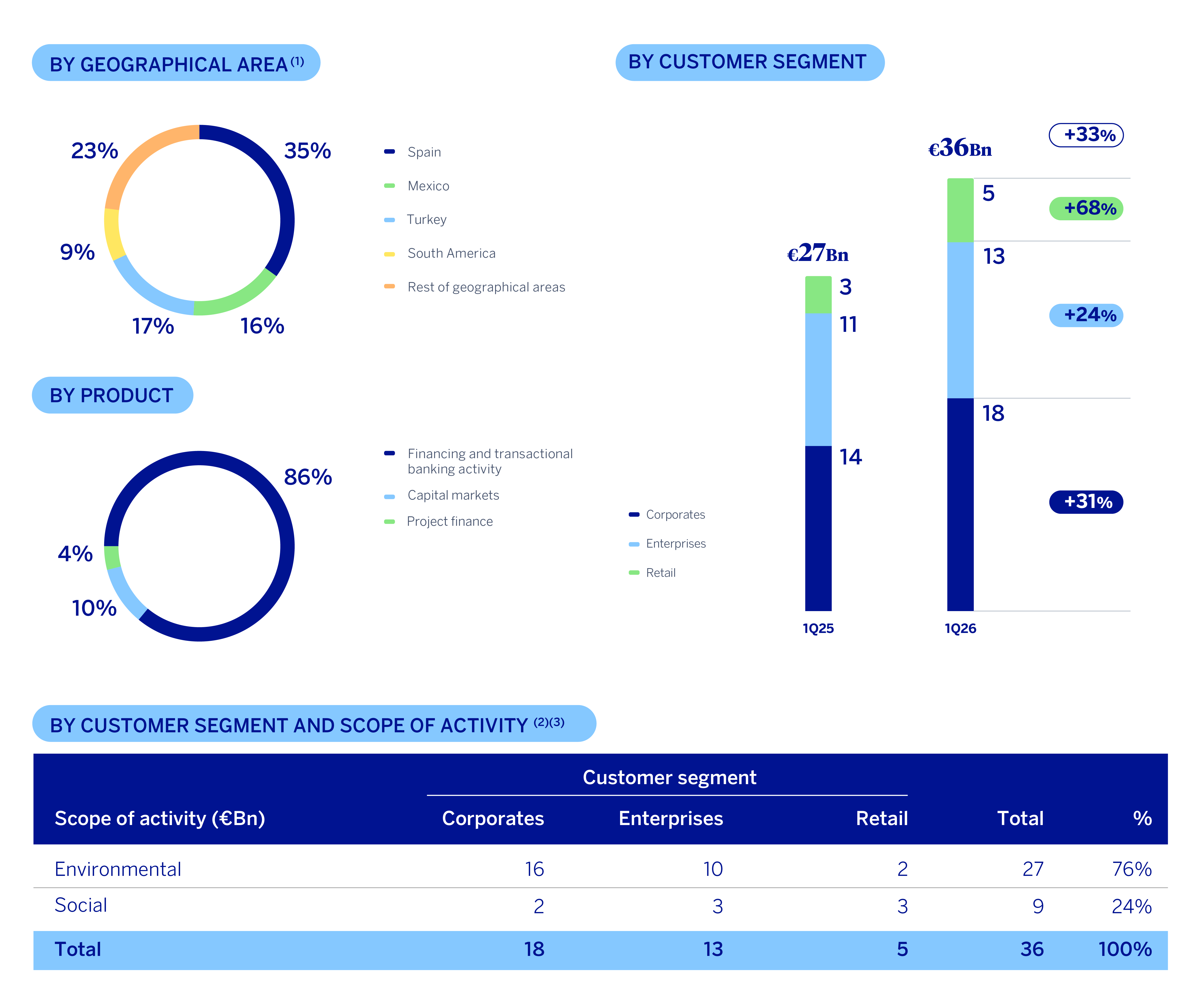

BBVA is driving sustainability as a differential growth engine. Within the framework of its ambitious target of channeling €700 billion into sustainable business for the 2025–2029 period4, the BBVA Group has channeled approximately €36 billion in the first three months of 2026, bringing the cumulative total to €170 billion since the announcement of this new target.

SUSTAINABLE BUSINESS CHANNELING 2025–MARCH 2026

SUSTAINABLE BUSINESS CHANNELING 1Q26

(1) Generally, the criterion used for distributing pipelines by geography is the location of the corresponding operation's registration. However, there are certain exceptions when several geographies are involved in the operation.

(2) In cases where data granularity does not allow for a direct attribution between the scope of activity, internal estimation models based on the best available information are applied. For reporting purposes, the “Environment” category integrates activities related to climate change and natural capital.

(3) The amounts indicated have been rounded; therefore, the amounts or variations shown may not be the exact arithmetic sum of the figures that precede them.

4 The Goal 2029 includes the channeling of financial flows, cumulatively, in relation with activities, clients or products considered to be sustainable, or promoting sustainability and/or the transition, in accordance with internal standards inspired by existing regulations, market standards such as the Green Bond Principles, the Social Bond Principles, the Climate Transition Finance Handbook and Climate Transition Bond Guidelines and the Sustainability Linked Bond Principles of the International Capital Markets Association, as well as the Green Loan Principles, Social Loan Principles, Guide to Transition Loans and the Sustainability Linked Loan Principles of the Loan Market Association, and best market practices. The foregoing is understood without prejudice to the fact that said channeling, both at an initial stage or at a later time, may not be registered on the balance sheet.

2025-2029 Strategic Plan

In the first quarter of 2026, the BBVA Group has continued to make significant progress in the execution of its 2025-2029 Strategic Plan, which aims to establish a new axis of differentiation by radically incorporating the customer perspective, as well as driving and strengthening the Group's commitment to growth and value creation. Thus, in mid-2025, the Group presented its financial objectives for the period 2025-2028, which are part of the strategic plan presented at the beginning of that same year.

BBVA continues to focus on innovation as a key driver for achieving these goals and continuing to lead the transformation of the sector. Thanks to artificial intelligence and next-generation technologies, the Group amplifies its positive impact on customers, helping them make the best decisions.

GROUP FINANCIAL KPIS GOALS EVOLUTION

(1) Compound Annual Growth Rate.

(2) Excluding the effect of Share Buybacks.

In this context, the BBVA Group achieved a cumulative result of €2,989 million by the end of the first quarter in 2026, representing an increase of 10.8% over the previous year, supported by the strong performance of recurring revenues from the banking business If the exchange rates variation is excluded, this growth increases to 14.1% favored by the solid evolution in gross income, which increased by 18.3% in constant terms, with a growth rate that is higher than that of operating expenses (+17.5% at constant exchange rates, impacted by an environment of still high inflation). As a result of this evolution, the efficiency ratio stood at 38.0% as of March 31, 2026, which represents an improvement of 24 basis points compared to the ratio as of March 31, 2025.

NET ATTRIBUTABLE PROFIT (LOSS) (MILLIONS OF EUROS)

During the first quarter of 2026, loans and advances to customers increased by 4.0%, driven by the dynamism of the wholesale segment. Of particular note within this segment was the higher volume of loans to business, which grew by 5.2% at the Group level. Loans to individuals increased by 2.2%, with consumer loans showing greater dynamism, followed by mortgages.

Customer funds registered an increase of 0.9% so far this year, with slight growth in customer base deposits of 0.5% at the Group level, and 1.5% in off-balance sheet funds.

LOANS AND ADVANCES TO CUSTOMERS AND TOTAL CUSTOMER FUNDS (VARIATION COMPARED TO 31-12-2025)

(1) The growth of non-performing loans and advances to customers under management (excluding repos) stands at 4.6%.

The BBVA Group's CET12 ratio stood at 12.83% as of March 31, 2026, which allows it to maintain a large management buffer over the Group's CET1 requirement as of that date (8.98%3), and is also above the Group's target management range of 11.5% - 12.0% of CET1.

CET1 RATIO

(1) Considering the latest official updates to the countercyclical capital buffer and the systemic risk buffer, applied on the basis of exposure as of December 31, 2025.

2 As of March 31, 2026, there were no differences between fully loaded and phased-in ratios given that the impact associated with the transitional adjustments is nil.

3 Considering the latest official updates to the countercyclical capital buffer and the systemic risk buffer, applied on the basis of exposure as of December 31, 2025.

BBVA is driving sustainability as a differential growth engine. Within the framework of its ambitious target of channeling €700 billion into sustainable business for the 2025–2029 period4, the BBVA Group has channeled approximately €36 billion in the first three months of 2026, bringing the cumulative total to €170 billion since the announcement of this new target.

SUSTAINABLE BUSINESS CHANNELING 2025–MARCH 2026

SUSTAINABLE BUSINESS CHANNELING 1Q26

(1) Generally, the criterion used for distributing pipelines by geography is the location of the corresponding operation's registration. However, there are certain exceptions when several geographies are involved in the operation.

(2) In cases where data granularity does not allow for a direct attribution between the scope of activity, internal estimation models based on the best available information are applied. For reporting purposes, the “Environment” category integrates activities related to climate change and natural capital.

(3) The amounts indicated have been rounded; therefore, the amounts or variations shown may not be the exact arithmetic sum of the figures that precede them.

4 The Goal 2029 includes the channeling of financial flows, cumulatively, in relation with activities, clients or products considered to be sustainable, or promoting sustainability and/or the transition, in accordance with internal standards inspired by existing regulations, market standards such as the Green Bond Principles, the Social Bond Principles, the Climate Transition Finance Handbook and Climate Transition Bond Guidelines and the Sustainability Linked Bond Principles of the International Capital Markets Association, as well as the Green Loan Principles, Social Loan Principles, Guide to Transition Loans and the Sustainability Linked Loan Principles of the Loan Market Association, and best market practices. The foregoing is understood without prejudice to the fact that said channeling, both at an initial stage or at a later time, may not be registered on the balance sheet.

Business Areas

Click on each area to learn more

Spain

Spain

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 1,656 | 2,653 |

| +3.6% (2) | +5.4% (2) |

| Operating income | Net atributable profit |

| 1,759 | 1,095 |

| +3.3%(2) | +8.1% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-25. Balances as of 31-03-26. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +1.2% | -1.3% |

RISKS |

| NPL coverage ratio |

| 67% | 69% |

| NPL ratio |

| 3.0% | 2.9% |

| Cost of risk |

| 0.34% | 0.34% |

(2) Year-on-year changes.

Mexico

Mexico

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 3,136 | 4,274 |

| +8.3% (2) | +10.3% (2) |

| Operating income | Net atributable profit |

| 2,956 | 1,453 |

| +10.5% (2) | +4.5% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-25. Balances as of 31-03-26. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +2.6% | +2.4% |

RISKS |

| NPL coverage ratio |

| 124% | 129% |

| NPL ratio |

| 2.7% | 2.6% |

| Cost of risk |

| 3.31% | 3.45% |

(2) Year-on-year changes.

Turkey

Turkey

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 1,121 | 1,712 |

| +93.4% (2) | +79.5% (2) |

| Operating income | Net atributable profit |

| 1,033 | 263 |

| +117.1% (2) | n.s.(2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-25. Balances as of 31-03-26. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +6.9% | +4.9% |

RISKS |

| NPL coverage ratio |

| 76% | 74% |

| NPL ratio |

| 3.9% | 4.1% |

| Cost of risk |

| 1.94% | 2.53% |

(2) Year-on-year changes.

South America

South America

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 1,474 | 1,626 |

| +33.4% (2) | +26.6% (2) |

| Operating income | Net atributable profit |

| 950 | 249 |

| +34.5% (2) | +33.8% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-25. Balances as of 31-03-26. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +2.6% | +5.5% |

RISKS |

| NPL coverage ratio |

| 92% | 90% |

| NPL ratio |

| 4.0% | 4.2% |

| Cost of risk |

| 2.50% | 2.76% |

(2) Year-on-year changes.

Rest of business

Rest of business

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 232 | 595 |

| +27.0% (2) | +41.8% (2) |

| Operating income | Net atributable profit |

| 355 | 236 |

| +50.7% (2) | +36.0% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-25. Balances as of 31-03-26. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +12.6% | -7.4% |

RISKS |

| NPL coverage ratio |

| 172% | 197% |

| NPL ratio |

| 0.2% | 0.1% |

| Cost of risk |

| 0.15% | 0.30% |

(2) Year-on-year changes.

* Gross income.

(1) At constant exchange rate.

(2) At constant exchange rates.

According to the accumulated results of the business areas by the end of March 2026, in each of them it is worth mentioning:

Spain generated a net attributable profit of €1,095 million, that is, 8.1% above the result achieved in the same period of 2025, driven by the evolution of recurring revenues and net trading income (hereinafter NTI).

BBVA Mexico achieved a net attributable profit of €1,453 million, which represents a year-on-year growth of 4.5%, excluding the impact of the evolution of the Mexican peso, explained mainly by the favorable evolution of net interest income and driven by the rest of components of gross income.

Turkey reached a net attributable profit of €263 million during the first quarter of 2026, with a year-on-year growth of 66.1%, as a result mainly of the good performance of recurring income from the banking business (net interest income and fees).

South America generated a net attributable profit of €249 million in the first quarter of 2026, which represents a year-on-year growth of 16.3%, favored mainly by the improvement in net attributable profit in Colombia.

Rest of Business achieved a net attributable profit of €236 million, 36.0% higher than in the same period of the previous year excluding the impact of currency evolution, favored by the evolution of the recurring revenues and the NTI.

The Corporate Center recorded in the first quarter of 2026 a net attributable loss of €305 million.

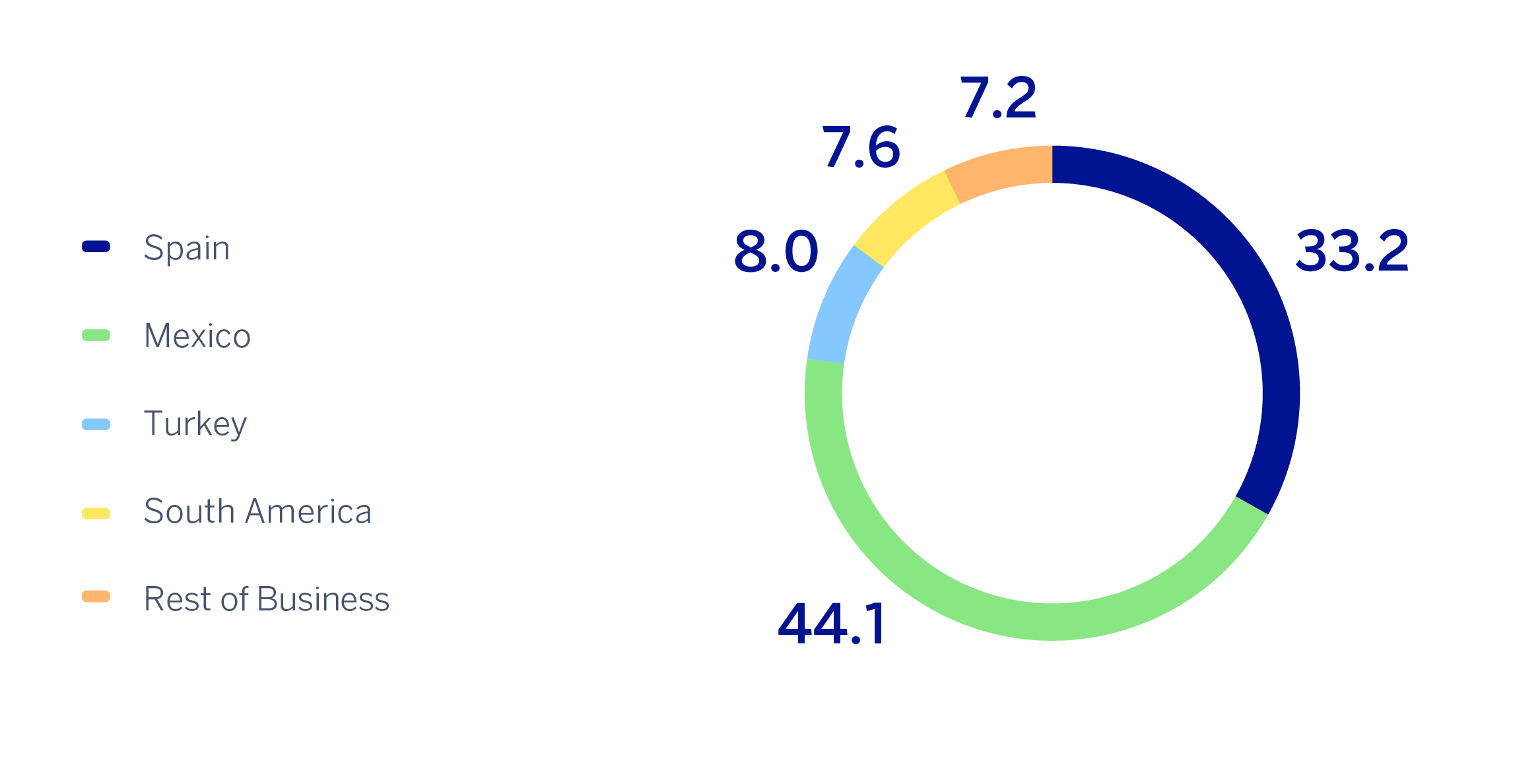

Lastly, and for a better understanding of the Group's activity and results, supplementary information is provided below for the wholesale business, Corporate & Investment Banking (CIB), carried out by BBVA in the countries where it operates. CIB generated a net attributable profit of €1,083 million5. Excluding the impact of currency fluctuations, this result represents a 24.2% increase over the previous year, which reflects again the strength of the Group's wholesale businesses, with the aim of offering a value proposition focused on the needs of its customers.

NET ATTRIBUTABLE PROFIT BREAKDOWN (1)

(PERCENTAGE. 1Q26)

(1) Excludes the Corporate Center.

5 The additional pro forma information from CIB excludes the application of hyperinflation accounting and the Group's wholesale business in Venezuela.

Read legal disclaimer of this report.

News

Contact

Shareholder attention line

Shareholder attention line

912 24 98 21

Subscription service

Subscription service Shareholder Office

Shareholder Office Contact email

Contact email