Report 3Q 2025

BBVA Posts Record Profit of Nearly €8 Billion Through September, Driven by Solid Lending Growth and Core Revenues

The share

The global economy has remained relatively resilient during the first half of 2025 despite high levels of uncertainty, trade tensions and the US administration's immigration restrictions. The negative effects of protectionist policies appear to be mitigated by fiscal stimulus, lower than expected effective tariffs and the strong growth in investment in artificial intelligence. Low financial volatility, supported by the Federal Reserve's (hereinafter, Fed) expansionary monetary policy, is also supporting global activity.

Even so, BBVA Research estimates that global growth will moderate in 2025 to 3.0%, in line with the previous forecast, and will reach around 3.1% in 2026. For the United States, the forecast of an economic slowdown remains unchanged, with a GDP growth of 1.7% in 2025 (unchanged from the previous forecast) and 1.8% in 2026. In the Eurozone, the upward revision of activity data in the first half of the year raises the GDP growth forecast for this year to 1.3% (four tenths more than in the previous scenario). By 2026, growth is expected to be reduced to 1.0%, in a context where the impact of tariffs and political instability in some countries in the bloc will be partially offset by increased spending on defense and infrastructure. In China, the economic slowdown continues: GDP could grow by 4.8% in 2025 (the same rate as previous quarter's forecast) and 4.5% in 2026.

Although the tariff increase is expected to keep inflation in the United States at around 3% by the end of 2026, the Fed could respond to the loss of momentum in the labor market with further interest rate cuts, following the reduction to 4.25% in September. In particular, BBVA Research forecasts at least two additional rate cuts in 2025, to 3.75%, and further reductions during 2026 to reach levels of 3%. In the Eurozone, BBVA Research expects the ECB to keep the deposit facility interest rate unchanged (at 2%) if inflationary pressures remain contained (the average inflation rate could close 2025 at 2.0% and 2026 at 1.8%) and downside risks to growth do not intensify. In China, monetary conditions are likely to continue to ease given the current context of very low inflation.

The balance of risks for the global economy remains weighted to the downside. In addition to protectionist measures in trade and immigration, and the structural challenges facing Europe and China, there is also uncertainty about the Fed's independence and its potential impact on financial markets.

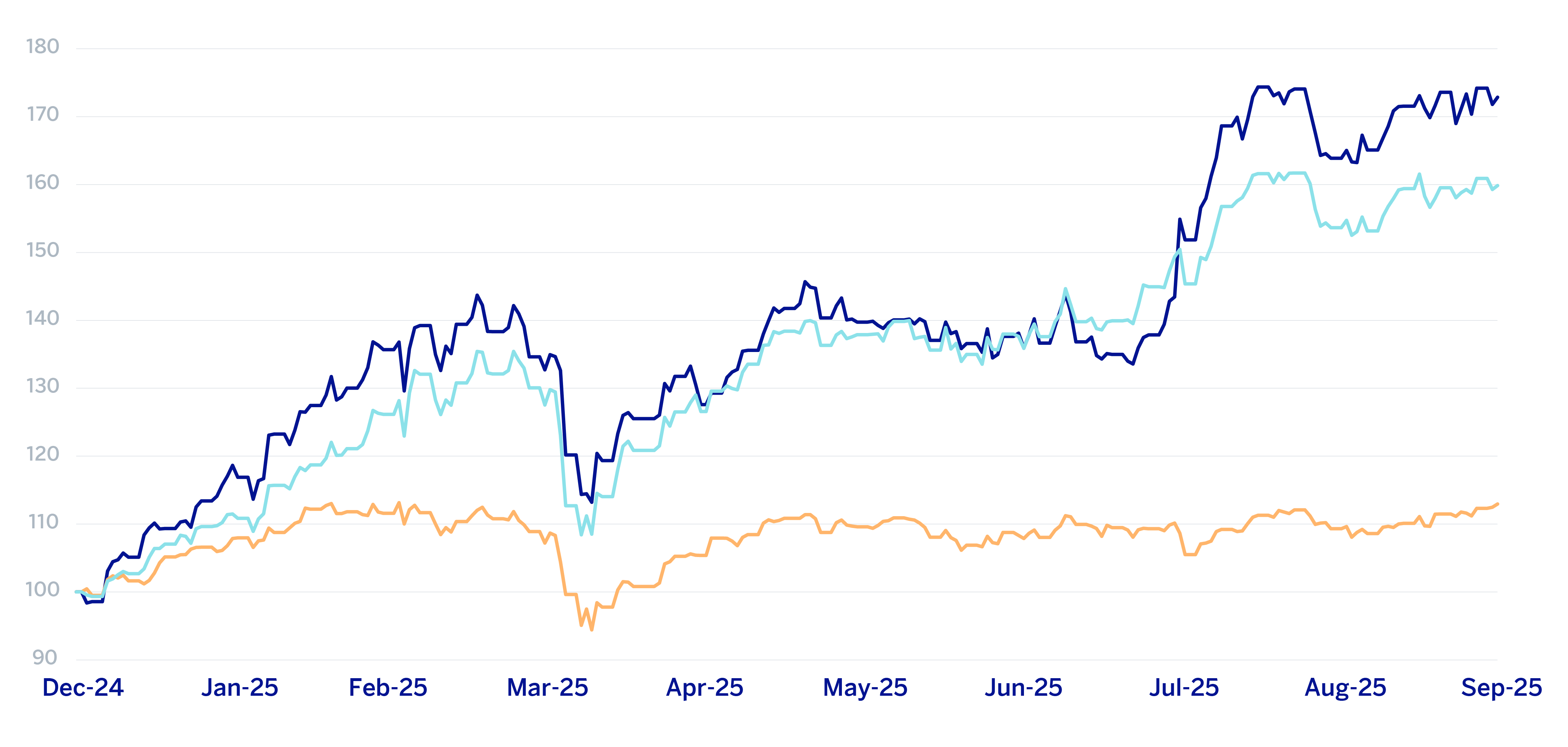

The main indexes have shown a positive performance during the third quarter of 2025. In Europe, the Stoxx Europe 600 index rose by 3.1% compared to the end of June 2025, and in Spain the Ibex 35 increased by 10.6% in the same period, showing a better relative performance. In the United States, the S&P 500 index increased by 7.8%.

With regard to the banking sector indexes, the performance in the third quarter of 2025 was better than the general indexes in Europe. The Stoxx Europe 600 Banks index, which includes the banks in the United Kingdom, and the Euro Stoxx Banks, an index of Eurozone banks, increased by 13.5% and 16.2% respectively, while in the United States, the S&P Regional Banks sector index increased by 6.5% in the period.

BBVA’s share price increased by 25.2% during the quarter, outperforming its sector index, closing the month of September 2025 at €16.34.

BBVA share evolution

Compared with European indexes (base indice 100=31-12-24)

BBVA

Eurostoxx-50

Eurostoxx Banks

| THE BBVA SHARE AND SHARE PERFORMANCE RATIOS | ||

|---|---|---|

| 30/09/2025 | 30/06/2025 | |

| Number of shareholders | 669,979 | 681,425 |

| Number of shares issued (millions) | 5,763 | 5,763 |

| Closing price (euros) | 16.34 | 13.06 |

| Book value per share (euros) (1) | 10.02 | 9.87 |

| Tangible book value per share (euros) (1) | 9.55 | 9.43 |

| Market capitalization (millions of euros) | 94,172 | 75,269 |

| (1) For more information, see Alternative Performance Measures at the end of the quarterly report. | ||

Regarding shareholder remuneration, as approved by the Annual General Shareholders´ Meeting of BBVA held on March 21, 2025, approved, under item 1.3 of the Agenda, a cash distribution against the 2024 results as a final dividend for the 2024 fiscal year, for an amount equal to €0.41 (€0.3321 net of withholding tax) per outstanding BBVA share entitled to participate in this distribution, which was paid on April 10, 2025.

By means of an inside information notice (información privilegiada) dated September 29, 2025, BBVA announced that its Board of Directors had approved the payment of a cash interim dividend of €0.32 gross (€0.2592 net of withholding tax) per share on account of the 2025 dividend entitled to participate in this distribution, to be paid on November 7, 2025.

Additionally, on January 30, 2025, BBVA announced a share buyback program for an amount of €993 million, which is expected to be carried out starting on October 31, 2025. Likewise, given the relevant accumulated excess capital above 12%, BBVA's Board of Directors has agreed to launch a significant additional share buyback as soon as it receives the authorization from the European Central Bank1.

On September 30, 2025, the number of BBVA shares outstanding was 5,763,285,465. The number of shareholders reached 669,979 and, by type of investor, 66.19% of the capital belonged to institutional investors and the remaining 33.81% was in the hands of retail shareholders.

BBVA shares are included on the main stock market indexes. At the closing of September 2025, the weighting of BBVA shares in the Ibex 35, Euro Stoxx 50 and the Stoxx Europe 600 index, were 11.7%, 2.3% and 0.8%, respectively. They are also included on several sector indexes, including Stoxx Europe 600 Banks, which includes the United Kingdom, with a weighting of 6.0% and the Euro Stoxx Banks index for the eurozone with a weighting of 9.6%. Moreover BBVA maintains a significant presence on a number of international sustainability indexes, such as, Dow Jones Sustainability Index (DJSI), FTSE4Good or MSCI ESG Indexes.

1 Subject to the corresponding approvals and authorizations.

Group's information

- 2025-2029 Strategic Plan

- Results

- Balance sheet and business activity

- Solvency

- Sustainability

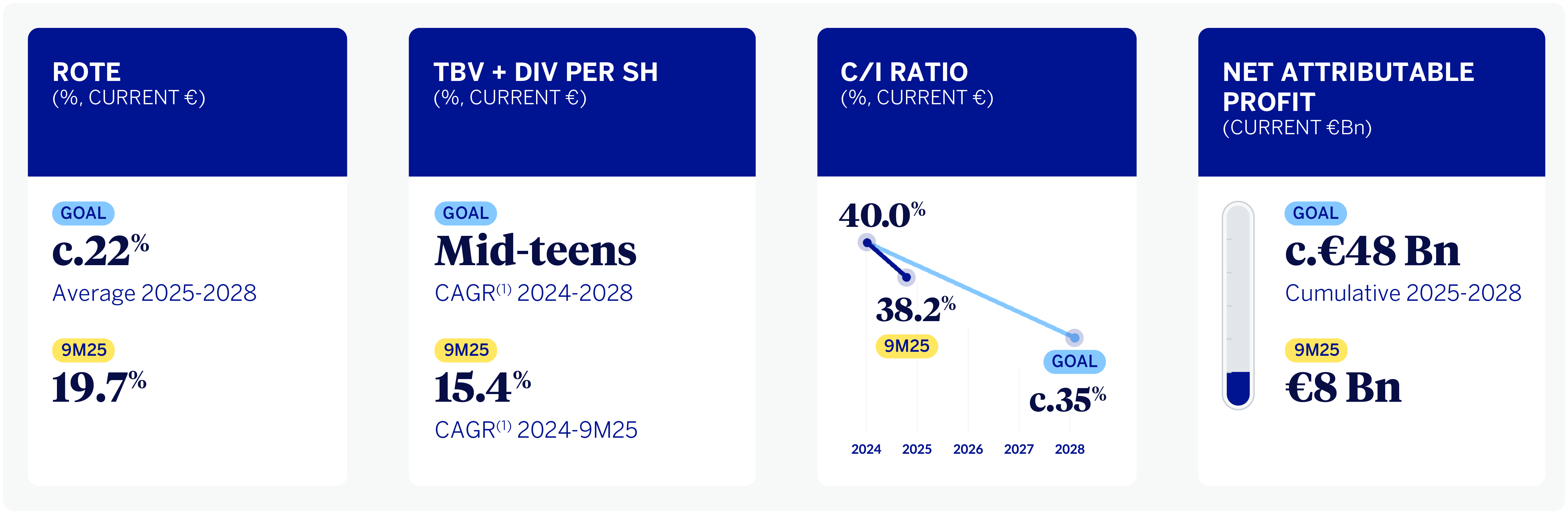

Between January and September 2025, the Group has made significant progress in the execution of its new 2025-2029 Strategic Plan, which aims to establish a new axis of differentiation by radically incorporating the customer perspective, as well as driving and strengthening the Group's commitment to growth and value creation. Thus, on July 31, the Group presented its financial objectives for the period 2025-2028, which are part of the strategic plan presented at the beginning of the year.

GROUP FINANCIAL KPIS GOALS EVOLUTION

(1) Compound Annual Growth Rate.

BBVA continues to focus on innovation as a key driver for achieving these goals and continuing to lead the transformation of the sector. Thanks to artificial intelligence and next-generation technologies, the Group amplifies its positive impact on customers, helping them make the best decisions.

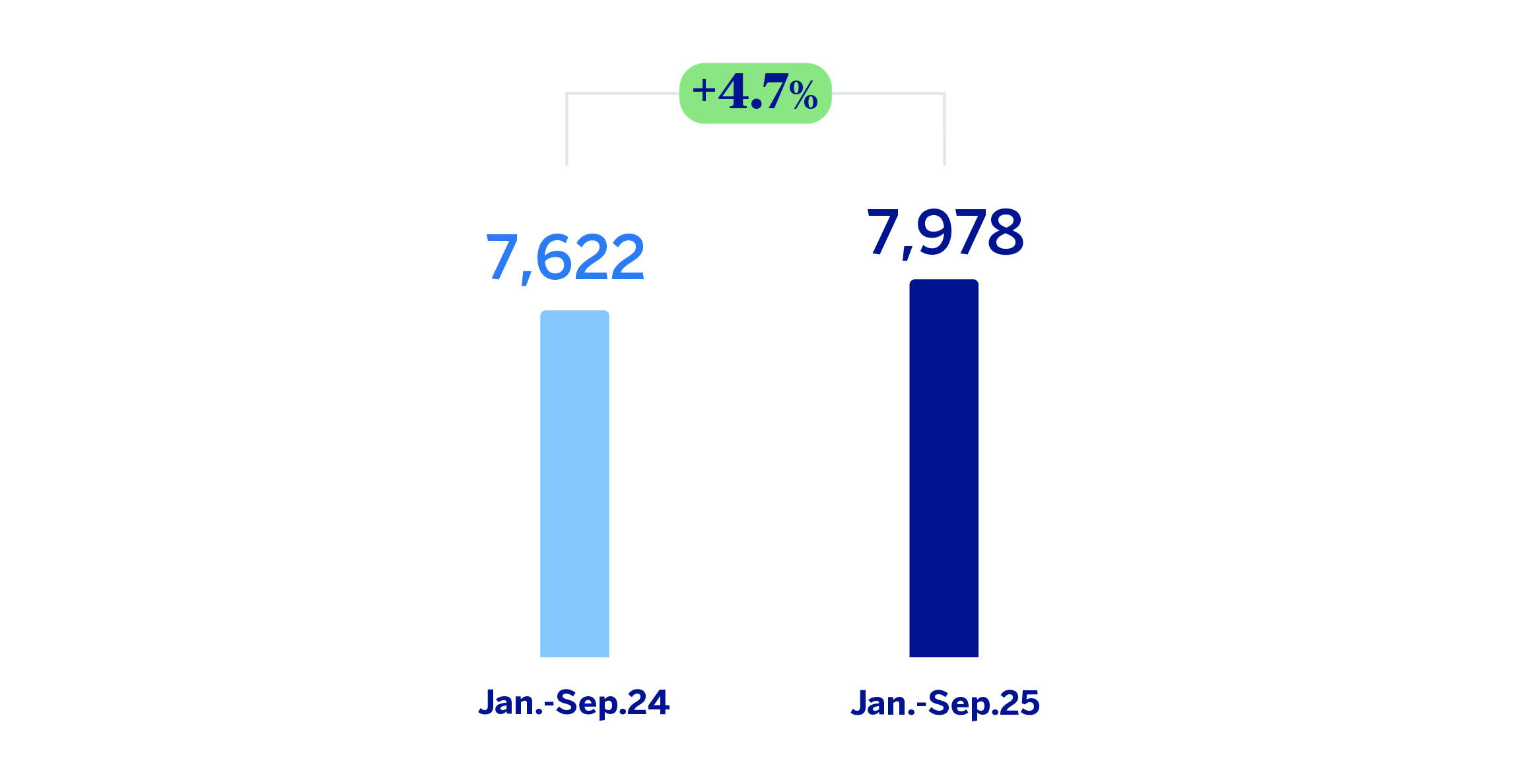

In this context, the BBVA Group achieved a cumulative result of €7,978, by the end of September 2025, representing a year-on-year increase of 4.7%, supported by the strong performance of recurring revenues from the banking business, that is, net interest income and net fees and commissions. If the exchange rates variation is excluded, this growth increases to 19.8%.

Thanks to the solid evolution in gross income, which increased by 16.2% in constant terms, with a growth rate that is significantly higher than that of operating expenses (+11.0% at constant exchange rates, impacted by an environment of still high inflation), the efficiency ratio fell to 38.2% as of September 30, 2025, which represents an improvement of 178 basis points compared to the ratio as of September 30, 2024.

The provisions for impairment on financial assets increased by 12.0% compared to the balances at the end of September 2024 and at constant exchange rates, a rate that is below the growth in lending, which reached 16.0%.

NET ATTRIBUTABLE PROFIT (LOSS) (MILLIONS OF EUROS)

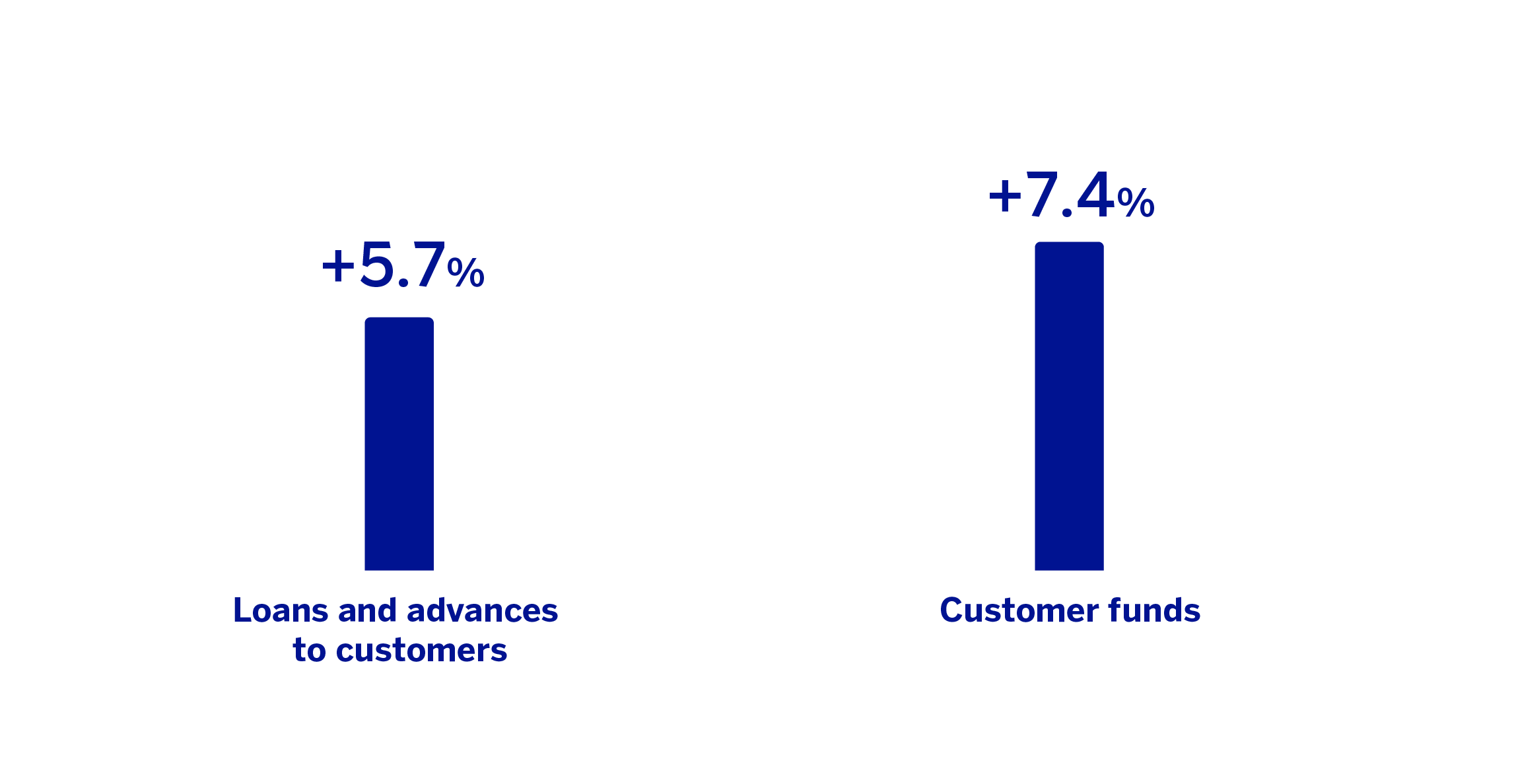

During the first nine months of 2025, loans and advances to customers increased by 5.7%, driven by the dynamism of the wholesale segment. Of particular note within this segment was the higher volume of loans to business, which grew by 5.9% at the Group level. Loans to individuals increased by 4.2%, with consumer and mortgage loans showing greater dynamism.

Customer funds grew by 7.4% in the first nine months of the year, driven not only by mutual funds and managed portfolios, but also by deposits from customers.

LOANS AND ADVANCES TO CUSTOMERS AND TOTAL CUSTOMER FUNDS (VARIATION COMPARED TO 31-12-2024)

The BBVA Group's CET12 ratio stood at 13.42% as of September 30, 2025, which allows it to maintain a large management buffer over the Group's CET1 requirement as of that date (9.13%3), and is also above the Group's target management range of 11.5% - 12.0% of CET1.

CET1 RATIO

(1) Considering the last official update of the countercyclical capital buffer, calculated on the basis of exposure as of June 30, 2025.

2 For the periods shown, there were no differences between fully loaded and phased-in ratios given that the impact associated with the transitional adjustments is nil.

3 Considering the last official updates of the countercyclical capital buffer and systemic risk buffer, calculated on the basis of exposure as of June 30, 2025.

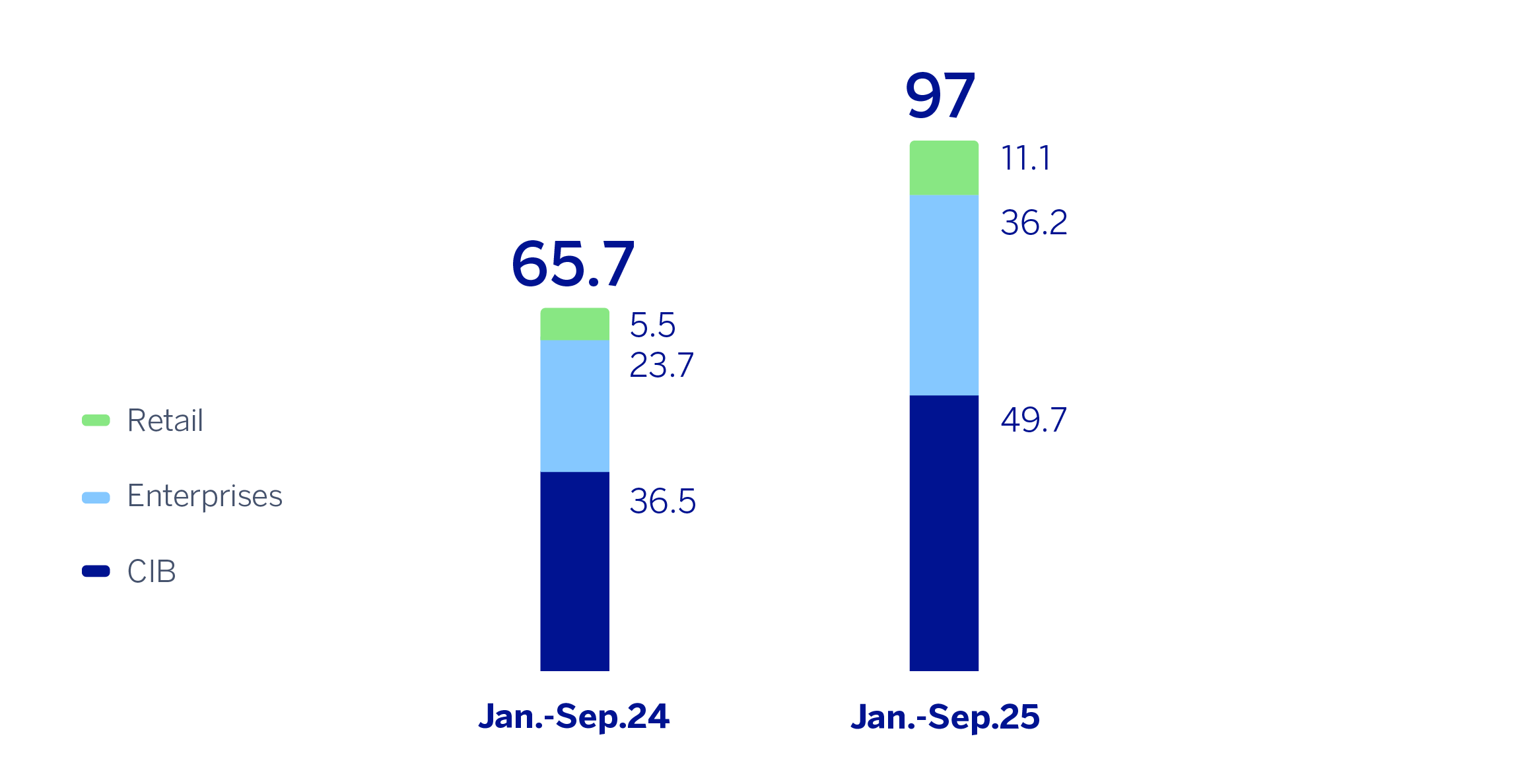

BBVA aims to promote sustainability as a driver of differential growth, leveraging the need to finance investments to meet the increasing demand for efficient and clean energy. As part of its new and ambitious target of channeling €700 billion in sustainable business for the 2025–2029 period4, the BBVA Group has channeled approximately €97 billion in the first nine months of 20255, representing a 48%6 increase. Of this amount, 76% corresponds to the environmental impact area, while the remaining 24% relates to opportunities in the social sphere.

CHANNELING OF SUSTAINABLE BUSINESS

BREAKDOWN BY CUSTOMER SEGMENTS (€BN)

BBVA’s sustainable business channeling includes aspects related to climate change and natural capital (which encompasses activities connected to water, agriculture, and the circular economy), as well as the promotion and financing of social initiatives (including social, educational, and health infrastructure; support for entrepreneurs and young businesses; and financial inclusion for the most disadvantaged groups). This channeling refers to financial flows linked to activities, clients, or products deemed sustainable by BBVA. Moreover, it is a cumulative concept, as it reflects amounts originated from a specific date. Some of these flows are not recorded on the balance sheet (such as client bond placements or guarantees), or they may have already matured.

During the first nine months of 2025, BBVA has channeled nearly €11.1 billion into its retail business, representing a year-on-year growth of 102%5. In line with its bet for sustainability, the Group has developed digital tools to help its retail customers adopt more responsible energy consumption habits. These solutions offer indicative estimates of the potential savings that can be achieved by implementing energy efficiency measures in areas such as the home and transport.

It is worth highlighting the strong performance in financing for the acquisition of hybrid or electric vehicles, which reached approximately €1.3 billion.

The corporate business unit channeled approximately €36.2 billion during the same period, representing a year-on-year growth of 52%5. During these months, BBVA has continued to offer its customers in this segment specialized advice on solutions aimed at generating potential savings, with cross-cutting initiatives such as energy efficiency, transport fleet renewal, and water resource management. A particularly noteworthy aspect has been financing linked to natural capital, which reached nearly €3.9 billion, where Mexico's contribution remains essential, generating around half of this channeling, mainly in the agricultural sector.

Between January and September 2025, CIB (Corporate & Investment Banking) channeled approximately €49.7 billion, representing a 36%5 increase. BBVA has continued to promote the financing of clean technologies and renewable energy projects within the wholesale segment, as well as solutions such as sustainability-linked confirming. Among these initiatives, the financing of renewable energy projects stands out, reaching €2.1 billion until September.

Relevant initiatives in the field of sustainability

BBVA considers the agri-food sector to be a strategic pillar due to its contribution to a more sustainable economy and its ability to address global challenges such as food security. The bank's strategy is geared toward supporting companies in their transition to more efficient and sustainable models, with a focus on modernization, digitalization, and opening up to new markets.

This engagement was recently showcased at Fruit Attraction, one of the world's largest events for the fruit and vegetable industry, where BBVA reaffirmed its role as the sector’s financial partner. In this context, the Group presented its value proposition, built around sustainability and internationalization. This positioning is supported by the fact that nearly 30% of the exhibiting companies are already customers.

4 The 2029 Objective includes the channeling of financial flows, on a cumulative basis, related to activities, clients, or products considered sustainable or that promote sustainability, in accordance with internal standards inspired by existing regulations, market standards such as the Green Bond Principles, Social Bond Principles, and Sustainability-Linked Bond Principles of the International Capital Market Association, as well as the Green Loan Principles, Social Loan Principles, and Sustainability-Linked Loan Principles of the Loan Market Association, and market best practices. The above is understood without prejudice to the fact that such channeling, both at its initial moment and at a later time, may not be recorded on the balance sheet. To determine the amounts of channeled sustainable business, internal criteria are used based on both internal and external information, whether public, provided by clients, or by a third party (primarily data providers and independent experts).This Sustainable Business Channeling Objective does not include the activities of BBVA Asset Management or the BBVA Microfinance Foundation.

5 The products and eligibility and accounting criteria are described in the Guide for Sustainable Business Channeling available on the BBVA Group's shareholders and investors website.

6 Growth compared to the same period of the previous year, excluding the activity of BBVA Asset Management and the BBVA Microfinance Foundation.

Between January and September 2025, the Group has made significant progress in the execution of its new 2025-2029 Strategic Plan, which aims to establish a new axis of differentiation by radically incorporating the customer perspective, as well as driving and strengthening the Group's commitment to growth and value creation. Thus, on July 31, the Group presented its financial objectives for the period 2025-2028, which are part of the strategic plan presented at the beginning of the year.

GROUP FINANCIAL KPIS GOALS EVOLUTION

(1) Compound Annual Growth Rate.

BBVA continues to focus on innovation as a key driver for achieving these goals and continuing to lead the transformation of the sector. Thanks to artificial intelligence and next-generation technologies, the Group amplifies its positive impact on customers, helping them make the best decisions.

In this context, the BBVA Group achieved a cumulative result of €7,978, by the end of September 2025, representing a year-on-year increase of 4.7%, supported by the strong performance of recurring revenues from the banking business, that is, net interest income and net fees and commissions. If the exchange rates variation is excluded, this growth increases to 19.8%.

Thanks to the solid evolution in gross income, which increased by 16.2% in constant terms, with a growth rate that is significantly higher than that of operating expenses (+11.0% at constant exchange rates, impacted by an environment of still high inflation), the efficiency ratio fell to 38.2% as of September 30, 2025, which represents an improvement of 178 basis points compared to the ratio as of September 30, 2024.

The provisions for impairment on financial assets increased by 12.0% compared to the balances at the end of September 2024 and at constant exchange rates, a rate that is below the growth in lending, which reached 16.0%.

NET ATTRIBUTABLE PROFIT (LOSS) (MILLIONS OF EUROS)

During the first nine months of 2025, loans and advances to customers increased by 5.7%, driven by the dynamism of the wholesale segment. Of particular note within this segment was the higher volume of loans to business, which grew by 5.9% at the Group level. Loans to individuals increased by 4.2%, with consumer and mortgage loans showing greater dynamism.

Customer funds grew by 7.4% in the first nine months of the year, driven not only by mutual funds and managed portfolios, but also by deposits from customers.

LOANS AND ADVANCES TO CUSTOMERS AND TOTAL CUSTOMER FUNDS (VARIATION COMPARED TO 31-12-2024)

The BBVA Group's CET12 ratio stood at 13.42% as of September 30, 2025, which allows it to maintain a large management buffer over the Group's CET1 requirement as of that date (9.13%3), and is also above the Group's target management range of 11.5% - 12.0% of CET1.

CET1 RATIO

(1) Considering the last official update of the countercyclical capital buffer, calculated on the basis of exposure as of June 30, 2025.

2 For the periods shown, there were no differences between fully loaded and phased-in ratios given that the impact associated with the transitional adjustments is nil.

3 Considering the last official updates of the countercyclical capital buffer and systemic risk buffer, calculated on the basis of exposure as of June 30, 2025.

BBVA aims to promote sustainability as a driver of differential growth, leveraging the need to finance investments to meet the increasing demand for efficient and clean energy. As part of its new and ambitious target of channeling €700 billion in sustainable business for the 2025–2029 period4, the BBVA Group has channeled approximately €97 billion in the first nine months of 20255, representing a 48%6 increase. Of this amount, 76% corresponds to the environmental impact area, while the remaining 24% relates to opportunities in the social sphere.

CHANNELING OF SUSTAINABLE BUSINESS

BREAKDOWN BY CUSTOMER SEGMENTS (€BN)

BBVA’s sustainable business channeling includes aspects related to climate change and natural capital (which encompasses activities connected to water, agriculture, and the circular economy), as well as the promotion and financing of social initiatives (including social, educational, and health infrastructure; support for entrepreneurs and young businesses; and financial inclusion for the most disadvantaged groups). This channeling refers to financial flows linked to activities, clients, or products deemed sustainable by BBVA. Moreover, it is a cumulative concept, as it reflects amounts originated from a specific date. Some of these flows are not recorded on the balance sheet (such as client bond placements or guarantees), or they may have already matured.

During the first nine months of 2025, BBVA has channeled nearly €11.1 billion into its retail business, representing a year-on-year growth of 102%5. In line with its bet for sustainability, the Group has developed digital tools to help its retail customers adopt more responsible energy consumption habits. These solutions offer indicative estimates of the potential savings that can be achieved by implementing energy efficiency measures in areas such as the home and transport.

It is worth highlighting the strong performance in financing for the acquisition of hybrid or electric vehicles, which reached approximately €1.3 billion.

The corporate business unit channeled approximately €36.2 billion during the same period, representing a year-on-year growth of 52%5. During these months, BBVA has continued to offer its customers in this segment specialized advice on solutions aimed at generating potential savings, with cross-cutting initiatives such as energy efficiency, transport fleet renewal, and water resource management. A particularly noteworthy aspect has been financing linked to natural capital, which reached nearly €3.9 billion, where Mexico's contribution remains essential, generating around half of this channeling, mainly in the agricultural sector.

Between January and September 2025, CIB (Corporate & Investment Banking) channeled approximately €49.7 billion, representing a 36%5 increase. BBVA has continued to promote the financing of clean technologies and renewable energy projects within the wholesale segment, as well as solutions such as sustainability-linked confirming. Among these initiatives, the financing of renewable energy projects stands out, reaching €2.1 billion until September.

Relevant initiatives in the field of sustainability

BBVA considers the agri-food sector to be a strategic pillar due to its contribution to a more sustainable economy and its ability to address global challenges such as food security. The bank's strategy is geared toward supporting companies in their transition to more efficient and sustainable models, with a focus on modernization, digitalization, and opening up to new markets.

This engagement was recently showcased at Fruit Attraction, one of the world's largest events for the fruit and vegetable industry, where BBVA reaffirmed its role as the sector’s financial partner. In this context, the Group presented its value proposition, built around sustainability and internationalization. This positioning is supported by the fact that nearly 30% of the exhibiting companies are already customers.

4 The 2029 Objective includes the channeling of financial flows, on a cumulative basis, related to activities, clients, or products considered sustainable or that promote sustainability, in accordance with internal standards inspired by existing regulations, market standards such as the Green Bond Principles, Social Bond Principles, and Sustainability-Linked Bond Principles of the International Capital Market Association, as well as the Green Loan Principles, Social Loan Principles, and Sustainability-Linked Loan Principles of the Loan Market Association, and market best practices. The above is understood without prejudice to the fact that such channeling, both at its initial moment and at a later time, may not be recorded on the balance sheet. To determine the amounts of channeled sustainable business, internal criteria are used based on both internal and external information, whether public, provided by clients, or by a third party (primarily data providers and independent experts).This Sustainable Business Channeling Objective does not include the activities of BBVA Asset Management or the BBVA Microfinance Foundation.

5 The products and eligibility and accounting criteria are described in the Guide for Sustainable Business Channeling available on the BBVA Group's shareholders and investors website.

6 Growth compared to the same period of the previous year, excluding the activity of BBVA Asset Management and the BBVA Microfinance Foundation.

Business Areas

Click on each area to learn more

Spain

Spain

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 4,905 | 7,473 |

| +2.3% (2) | +5.8% (2) |

| Operating income | Net atributable profit |

| 5,053 | 3,139 |

| +9.7% (2) | +10.5% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-24. Balances as of 30-09-25. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +5.5% | +5.2% |

RISKS |

| NPL coverage ratio |

| 59% | 65% |

| NPL ratio |

| 3.7% | 3.1% |

| Cost of risk |

| 0.38% | 0.34% |

(2) Year-on-year changes.

Mexico

Mexico

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 8,393 | 11,124 |

| +8.3% (2) | +8.0% (2) |

| Operating income | Net atributable profit |

| 7,735 | 3,875 |

| +7.2% (2) | +4.5% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-24. Balances as of 30-09-25. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +3.8% | +9.8% |

RISKS |

| NPL coverage ratio |

| 121% | 123% |

| NPL ratio |

| 2.7% | 2.8% |

| Cost of risk |

| 3.39% | 3.27% |

(2) Year-on-year changes.

Turkey

Turkey

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 2,137 | 3,776 |

| +185.8% (2) | +87.4% (2) |

| Operating income | Net atributable profit |

| 2,125 | 648 |

| +139.5% (2) | n.s.(2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-24. Balances as of 30-09-25. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +38.0% | +46.7% |

RISKS |

| NPL coverage ratio |

| 96% | 78% |

| NPL ratio |

| 3.1% | 3.7% |

| Cost of risk |

| 1.27% | 1.76% |

(2) Year-on-year changes.

South America

South America

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 3,537 | 4,001 |

| -1.9% (2) | +23.5% (2) |

| Operating income | Net atributable profit |

| 2,245 | 585 |

| +38.0% (2) | +84.2% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-24. Balances as of 30-09-25. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +10.1% | +9.5% |

RISKS |

| NPL coverage ratio |

| 88% | 93% |

| NPL ratio |

| 4.5% | 4.1% |

| Cost of risk |

| 2.87% | 2.43% |

(2) Year-on-year changes.

Rest of business

Rest of business

HIGHLIGHTS FOR THE PERIOD

|

RESULTS

| |

| Net interest income | Gross income |

| 596 | 1,296 |

| +15.7% (2) | +24.5% (2) |

| Operating income | Net atributable profit |

| 672 | 481 |

| +22.4% (2) | +20.0% (2) |

ACTIVITY (1)

|

|

| Variation compared 31-12-24. Balances as of 30-09-25. |

|

| Performing loans and advances to customers under management | Customer funds under management |

| +20.8% | +32.6% |

RISKS |

| NPL coverage ratio |

| 102% | 136% |

| NPL ratio |

| 0.3% | 0.2% |

| Cost of risk |

| 0.17% | 0.10% |

(2) Year-on-year changes.

* Gross income.

(1) At constant exchange rate.

(2) At constant exchange rates.

According to the accumulated results of the business areas by the end of September 2025, in each of them it is worth mentioning:

Spain generated a net attributable profit of €3,139m, that is, 10.5% above the result achieved in the same period of 2024, driven by the evolution of the recurring revenue from the banking business.

BBVA Mexico achieved a cumulative net attributable profit of €3,875m, which represents a year-on-year growth of 4.5%, excluding the impact of the Mexican peso, explained mainly by the favorable evolution of the net interest income.

Turkey reached a net attributable profit of €648m, with a year-on-year growth of 49.6%, as a result of the good performance of recurring revenues in banking business and a less negative hyperinflation impact.

South America generated a net attributable profit of €585m in the first nine months of 2025, which represents a year-on-year growth of 24.1%, mainly derived from a less negative hyperinflation adjustment in Argentina and an improvement in net attributable profit in Colombia and Peru.

Rest of Business achieved an accumulated net attributable profit of €481m, this is, excluding the currency evolution, 20.0% higher than in the same period of the previous year, favored by the evolution of the recurring revenues and the net trading income (hereinafter, NTI).

The Corporate Center recorded a net attributable loss of €-750m, in line with the €-726m recorded in the same period of the previous year.

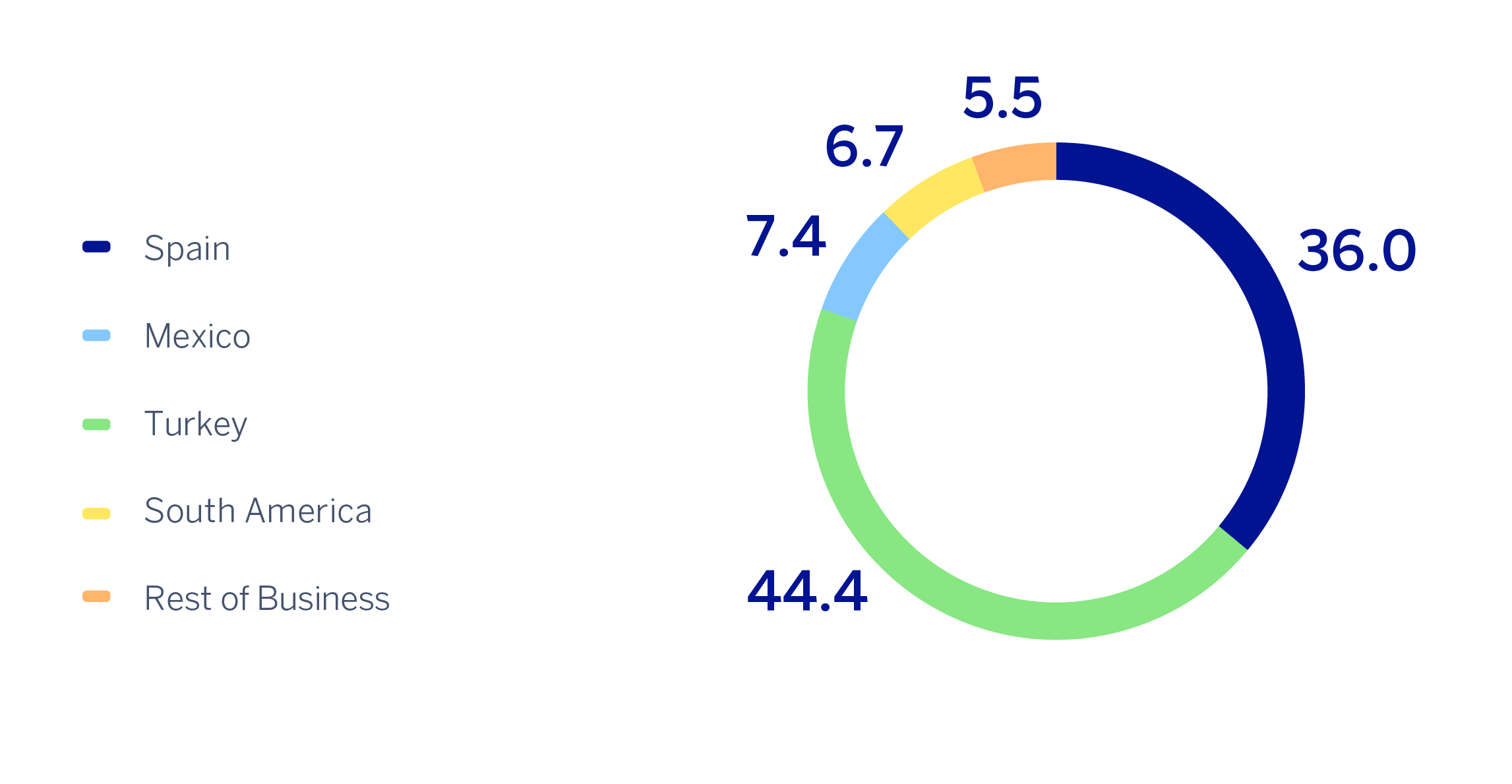

Lastly, and for a broader understanding of the Group's activity and results, supplementary information is provided below for the wholesale business, Corporate & Investment Banking (CIB), carried out by BBVA in the countries where it operates. CIB generated a net attributable profit of €2,341m7. Excluding the impact of currency fluctuations, this result represents a 31.8% increase over the same period of the previous year and reflects again the strength of the Group's wholesale businesses, with the aim of offering a value proposition focused on the needs of its customers.

NET ATTRIBUTABLE PROFIT BREAKDOWN (1)

(PERCENTAGE. JAN.-SEP.25)

(1) Excludes the Corporate Center.

7 The additional pro forma CIB information does not include the application of hyperinflation accounting or the Group's wholesale business in Venezuela.

Read legal disclaimer of this report.

News

Contact

Shareholder attention line

Shareholder attention line

912 24 98 21

Subscription service

Subscription service Shareholder Office

Shareholder Office Contact email

Contact email