Capital and shareholders

Capital base

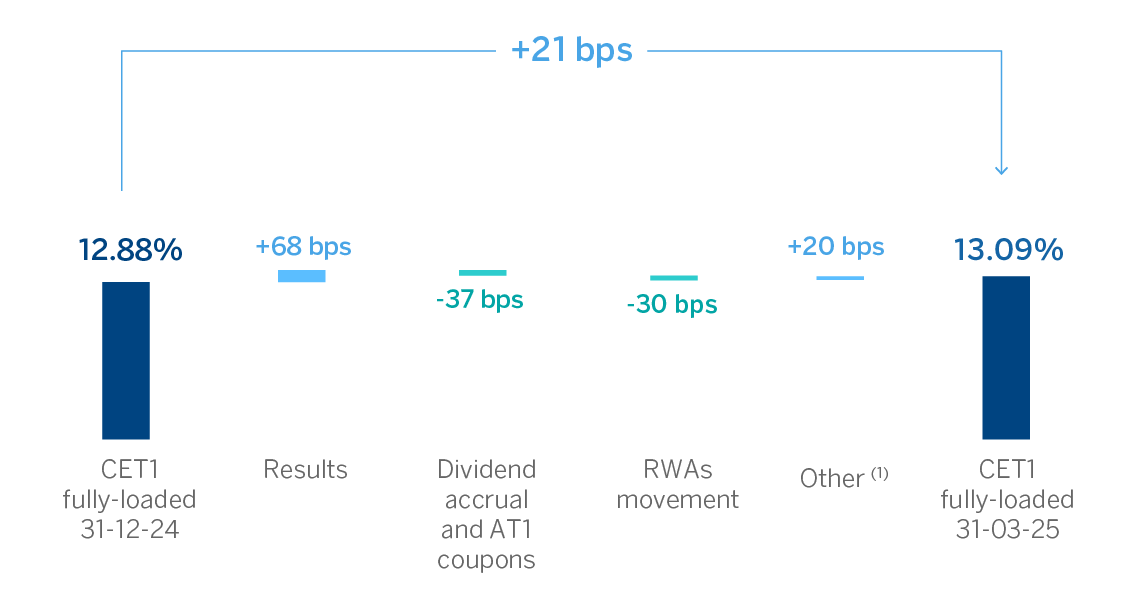

The BBVA Group's CET1 ratio9 stood at 13.09% as of March 31, 2025, which allows it to maintain a large management buffer over the Group's CET1 requirement as of that date (9.13%10), and is also above the Group's target management range of 11.5% - 12.0% of CET1.

Regarding the evolution during the first quarter, the Group’s CET1 has increased by 21 basis points with respect to the December level (12.88%). The entry into force of the new regulation CRR3 had no significant impact to this ratio.

The strong earnings generation during the quarter (+68 basis points) net of shareholder remuneration and payment of capital instruments (CoCos), generated a positive contribution of +31 basis points to CET1 ratio, which offset the growth of risk-weighted assets (RWA) derived from the organic growth of activity in constant terms, net of risk transfer initiatives in the period (consumption of -30 basis points), in line with the Group's strategy of continuing to promote profitable growth.

Among the remaining impacts that increase the ratio by 20 basis points, the positive compensation effect of Other Comprehensive Income over the net monetary value loss registered in results in hyperinflationary economies stands out, and, to a lesser extent, the valuation of fixed income and equity portfolios.

QUARTERLY EVOLUTION OF THE CET1 RATIO

(1) Includes, among others, FX and mark to market of HTC&S portfolios, minority interests, and a positive impact in OCI equivalent to the Net Monetary Position value loss in hyperinflationary economies registered in results.

The AT1 ratio stood at 1.44% showing a reduction of -9 basis points compared to December 31, 2024. In the quarter BBVA, S.A. issued USD 1 billion worth of CoCos, the effect of which was offset by the early redemption of another issuance for the same amount. The impact of the depreciation of the US dollar on CoCos issued in this currency explains part of the reduction of the ratio in the quarter.

The Tier 2 ratio has experienced a significant variation in the quarter (+52 basis points), mainly impacted by the issuance in Spain, of subordinated debt amounting to €1 billion. In addition, in Mexico, a USD 1 billion of subordinated debt was issued.

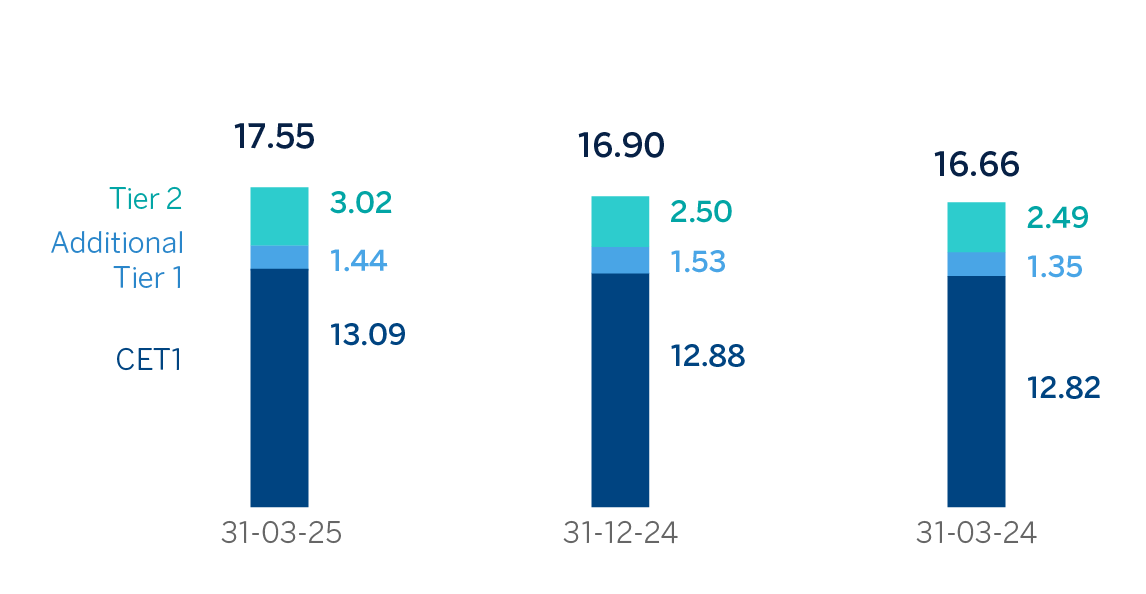

As a consequence of the foregoing, the consolidated total capital ratio stood at 17.55% as of March 31, 2025, above the total capital requirements (13.29%10).

Following the latest decision of the SREP (Supervisory Review and Evaluation Process), which came into force on January 1, 2025, BBVA Group must maintain at consolidated level a total capital ratio of 13.29% and a CET1 capital ratio of 9.13%10, including a Pillar 2 requirement at consolidated level of 1.68% (a minimum of 1.02% must be satisfied with CET1), of which 0.18% is determined on the basis of the ECB's prudential provisioning expectations, and must be satisfied by CET1.

CAPITAL RATIOS

(PERCENTAGE)

| CAPITAL BASE (MILLIONS OF EUROS) | |||

|---|---|---|---|

| 31-03-25 (1) | 31-12-24 | 31-03-24 | |

| Common Equity Tier 1 (CET1) | 51,745 | 50,799 | 48,740 |

| Tier 1 | 57,452 | 56,822 | 53,868 |

| Tier 2 | 11,946 | 9,858 | 9,450 |

| Total capital (Tier 1 + Tier 2) | 69,397 | 66,680 | 63,318 |

| Risk-weighted assets | 395,352 | 394,468 | 380,044 |

| CET1 ratio (%) | 13.09 | 12.88 | 12.82 |

| Tier 1 ratio (%) | 14.53 | 14.40 | 14.17 |

| Tier 2 ratio (%) | 3.02 | 2.50 | 2.49 |

| Total capital ratio (%) | 17.55 | 16.90 | 16.66 |

General note: The 2024 data and ratios are presented according to the requirements under CRR2, while those for March 2025 have been calculated applying the regulatory changes of CRR3.

(1) Preliminary data.

As of March 31, 2025, the fully loaded leverage ratio stood at 6.94%, which represents an increase of 13 basis points compared to December 2024.

| LEVERAGE RATIO | |||

|---|---|---|---|

| 31-03-25 (1) | 31-12-24 | 31-03-24 | |

| Exposure to Leverage Ratio (million euros) | 827,804 | 834,488 | 830,725 |

| Leverage ratio (%) | 6.94 | 6.81 | 6.48 |

General note: The 2024 data and ratios are presented according to the requirements under CRR2, while those for March 2025 have been calculated applying the regulatory changes of CRR3.

(1) Preliminary data.

With respect to the MREL (Minimum Requirement for own funds and Eligible Liabilities) ratios11 achieved as of March 31, 2025, these were 33.20% and 12.51%, respectively for MREL in RWA and MREL in LR, reaching the subordinated ratios of both 27.70% and 10.43%, respectively. A summarizing table is shown below:

| MREL | |||

|---|---|---|---|

| 31-03-25 (1) | 31-12-24 | 31-03-24 | |

| Total own funds and eligible liabilities (million euros) | 65,771 | 63,887 | 61,061 |

| Total RWA of the resolution group (million euros) | 198,078 | 228,796 | 219,593 |

| RWA ratio (%) | 33.20 | 27.92 | 27.81 |

| Total exposure for the Leverage calculation (million euros) | 527,899 | 527,804 | 530,175 |

| Leverage ratio (%) | 12.51 | 12.10 | 11.52 |

General note: The 2024 data and ratios are presented according to the requirements under CRR2, while those for March 2025 have been calculated applying the regulatory changes of CRR3. In addition, they do not include the combined buffer requirement (CBR).

(1) Preliminary data.

On March 27, 2024 the Group made public that it had received a communication from the Bank of Spain regarding its new MREL requirement 22.79%12. In addition, BBVA must reach, also as from March 27, 2024, a volume of own funds and eligible liabilities in terms of total exposure considered for purposes of calculating the leverage ratio of 8.48% (the “MREL in LR”)13. These requirements do not include the current combined buffer requirement, which, according to current regulations and supervisory criteria, is 3.65%14. Given the structure of the resolution group's own funds and eligible liabilities, as of March 31, 2025, the Group meets the aforementioned requirements.

Likewise, with the aim of reinforcing compliance with these requirements, BBVA made several debt issuances during the first quarter of 2025. For more information on these issuances, see "Structural risks" section within the "Risk management" chapter.

Shareholder remuneration

Regarding shareholder remuneration, as approved by the General Shareholders' Meeting on March 21, 2025, under item 1.3 of the agenda, on April 10, 2025, a cash payment of €0.41 gross per outstanding BBVA share was made against 2024 earnings, with the right to receive this amount as a final dividend for 2024. Thus, the total amount of cash distributions for 2024, taking into account that €0.29 gross per share were distributed in October 2024, amounted to €0.70 gross per share.

Additionally, on January 30, 2025 a BBVA share repurchase program for an amount of €993m million was announced, which is pending execution as of the date of this document.

As of March 31, 2025, BBVA’s share capital amounted to €2,824,009,877.85 divided into 5,763,285,465 shares.

| SHAREHOLDER STRUCTURE (31-03-25) | |||||

|---|---|---|---|---|---|

Number of shares | |||||

| Number | % | Number | % | ||

| Up to 500 | 301,609 | 43.7 | 55,002,009 | 1.0 | |

| 501 to 5,000 | 305,358 | 44.2 | 541,214,969 | 9.4 | |

| 5,001 to 10,000 | 44,984 | 6.5 | 315,297,202 | 5.5 | |

| 10,001 to 50,000 | 34,898 | 5.1 | 667,195,479 | 11.6 | |

| 50,001 to 100,000 | 2,461 | 0.4 | 167,876,439 | 2.9 | |

| 100,001 to 500,000 | 1,080 | 0.2 | 193,457,118 | 3.4 | |

| More than 500,001 | 245 | 0.04 | 3,823,242,249 | 66.3 | |

| Total | 690,635 | 100 | 5,763,285,465 | 100 | |

Note: in the case of shares held by investors operating through a custodian entity located outside Spain, only the custodian is counted as a shareholder, as it is the entity registered in the corresponding book-entry register. Therefore, the reported number of shareholders does not include these underlying holders.

Ratings

During the first three months of 2025, several agencies have recognized the favorable evolution of BBVA's fundamentals, especially in relation to the high levels of profitability achieved and the resilient asset quality maintained. In February, Fitch changed the outlook on its rating (A-) to positive from stable, and Moody's changed the outlook on its long-term senior preferred debt to rating watch positive from positive in March, maintaining its rating at A3. Also in February, DBRS communicated the result of its annual review of BBVA affirming its rating at A (high) with a stable outlook and S&P affirmed in March its rating at A with a stable outlook. The following table shows the credit ratings and outlooks assigned by the agencies:

| RATINGS | |||

|---|---|---|---|

| Rating agency | Long term (1) | Short term | Outlook |

| DBRS | A (high) | R-1 (middle) | Stable |

| Fitch | A- | F-2 | Positive |

| Moody's | A3 | P-2 | Rating watch positive |

| Standard & Poor's | A | A-1 | Stable |

(1) Ratings assigned to long term senior preferred debt. Additionally, Moody’s, Fitch and DBRS assign A2, A- and A (high) rating, respectively, to BBVA’s long term deposits.

9 For the periods shown, there were no differences between fully loaded and phased-in ratios given that the impact associated with the transitional adjustments is nil.

10 Considering the last official update of the countercyclical capital buffer and systemic risk buffer, calculated on the basis of exposure as of December 31, 2024.

11 Calculated at subconsolidated level according to the resolution strategy MPE (“Multiple Point of Entry”) of the BBVA Group, established by the SRB ("Single Resolution Board"). The resolution group is made up of Banco Bilbao Vizcaya Argentaria, S.A. and subsidiaries that belong to the same European resolution group. That implies the ratios are calculated under the subconsolidated perimeter of the resolution group. Preliminary MREL ratios as of the date of publication.

12 The subordination requirement in RWA is 13.50%.

13 The subordination requirement in Leverage ratio is 5.78%.

14 Considering the last official updates of the countercyclical capital buffer and systemic risk buffer, calculated on the basis of exposure as of December 31, 2024.