South America

Highlights for the period January - September 2025

- Balanced growth in lending activity and customer funds

- Argentina's cumulative hyperinflation adjustment in September 2025 significantly lower than in September 2024

- Peru and Colombia continue showing good performance in terms of risk quality

- Year-on-year increase in the area's net attributable profit

BUSINESS ACTIVITY (1)

(VARIATION AT CONSTANT EXCHANGE RATES COMPARED TO 31-12-24)

(1) Excluding repos.

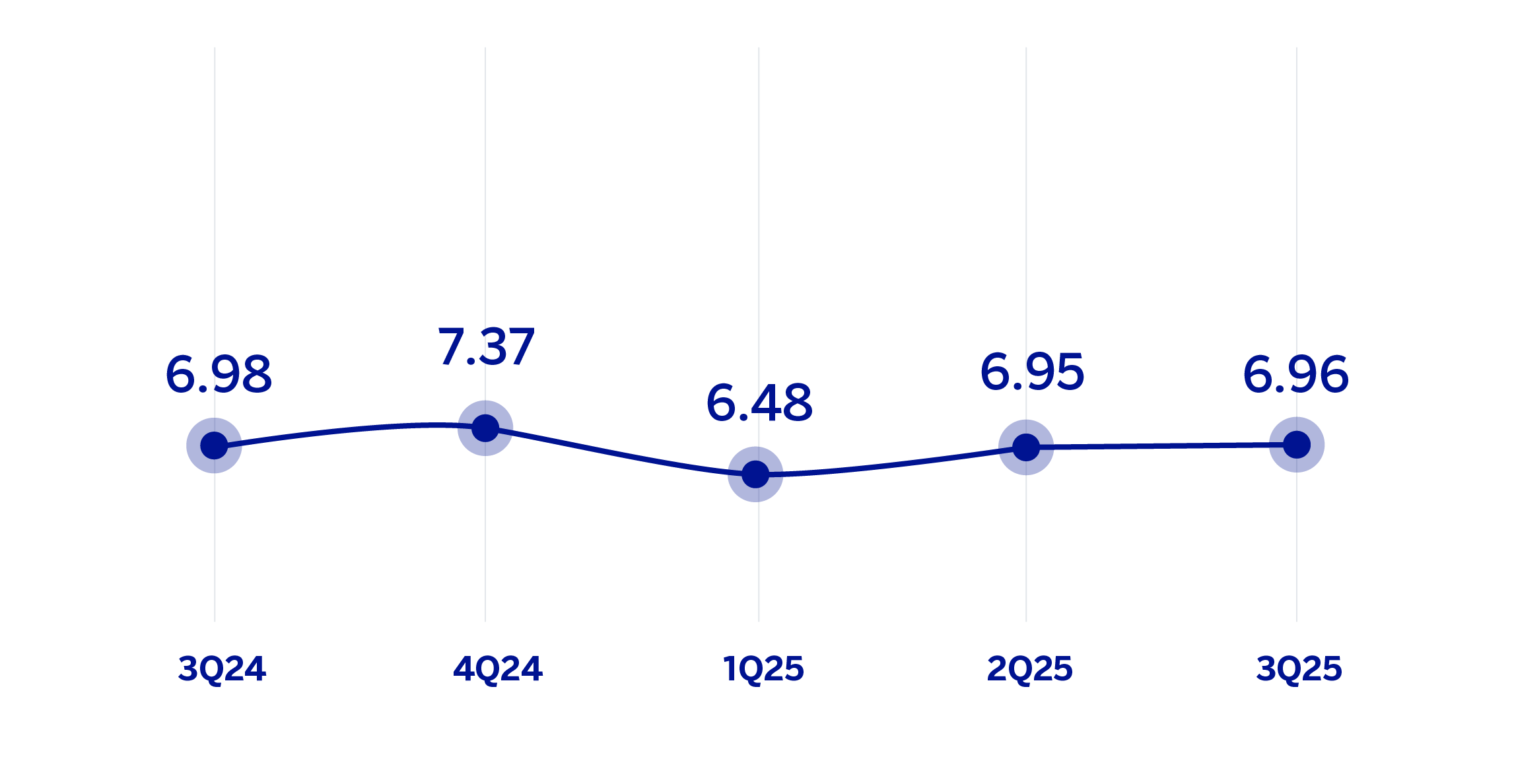

NET INTEREST INCOME / AVERAGE TOTAL ASSETS

(PERCENTAGE AT CONSTANT EXCHANGE RATES)

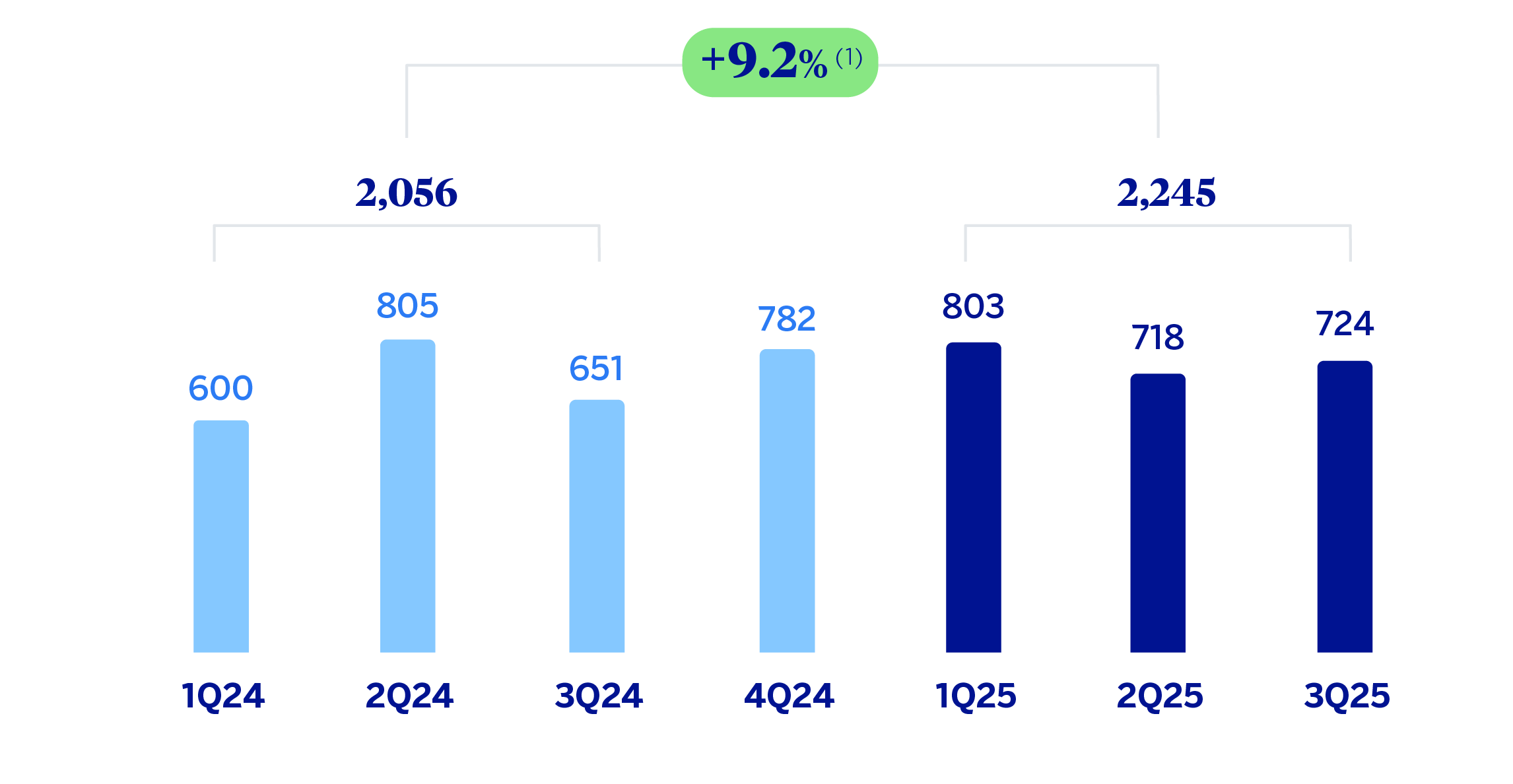

OPERATING INCOME

(MILLIONS OF EUROS AT CURRENT EXCHANGE RATES)

(1) At constant exchange rates: +38.0%.

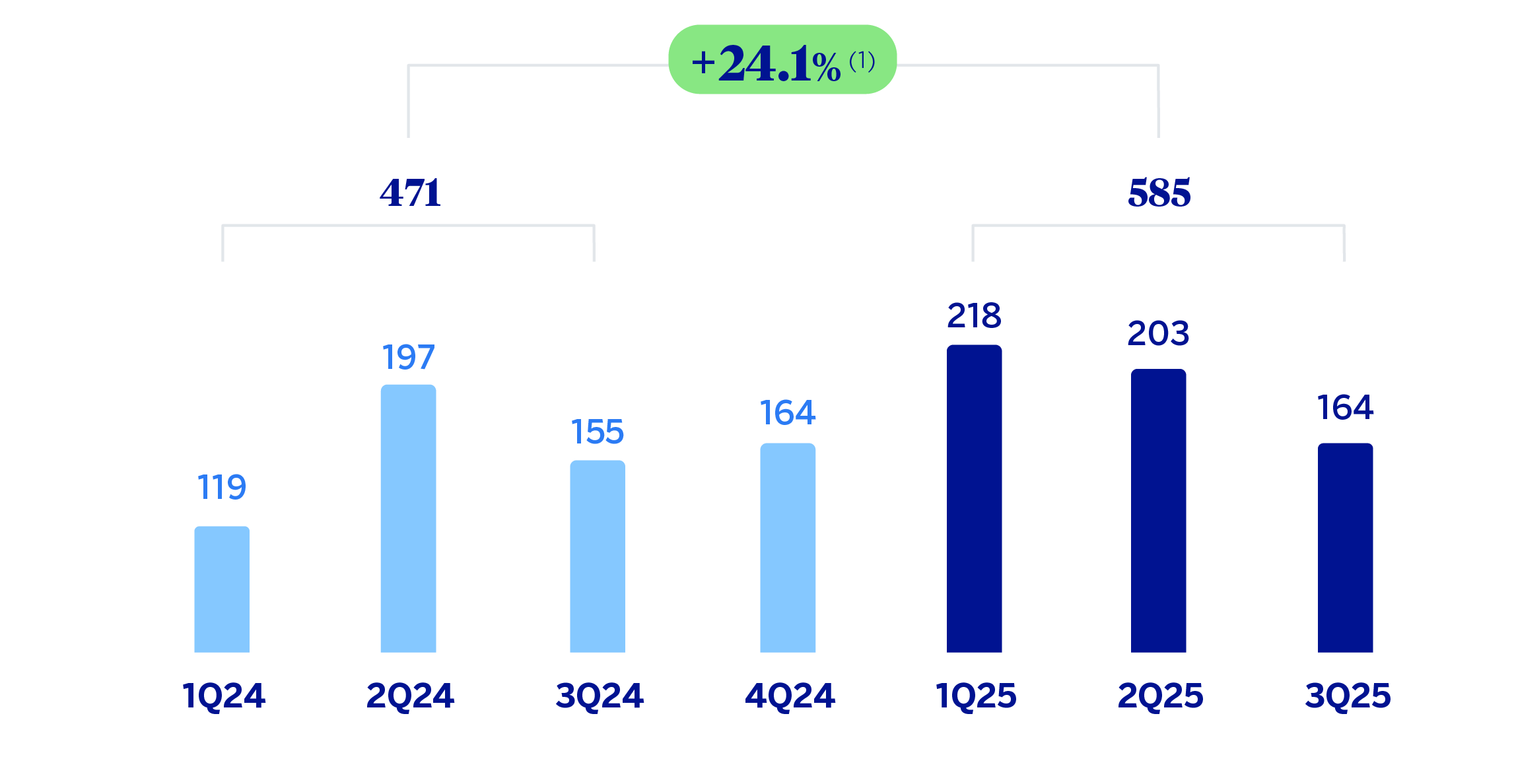

NET ATTRIBUTABLE PROFIT (LOSS)

(MILLIONS OF EUROS AT CURRENT EXCHANGE RATES)

(1) At constant exchange rates: +84.2%.

| FINANCIAL STATEMENTS AND RELEVANT BUSINESS INDICATORS (MILLIONS OF EUROS AND PERCENTAGE)3 | ||||

|---|---|---|---|---|

| Income statement | Jan.-Sep.25 | 𝚫 % | 𝚫 % (1) | Jan.-Sep.24 |

| Net interest income | 3,537 | (15.3) | (1.9) | 4,178 |

| Net fees and commissions | 655 | 7.5 | 18.9 | 610 |

| Net trading income | 433 | (20.9) | (11.6) | 548 |

| Other operating income and expenses | (625) | (57.5) | (55.6) | (1,471) |

| Gross income | 4,001 | 3.5 | 23.5 | 3,865 |

| Operating expenses | (1,756) | (2.9) | 9.0 | (1,809) |

| Personnel expenses | (787) | (4.7) | 8.1 | (826) |

| Other administrative expenses | (815) | (1.1) | 11.6 | (824) |

| Depreciation | (154) | (3.0) | 0.5 | (159) |

| Operating income | 2,245 | 9.2 | 38.0 | 2,056 |

| Impairment on financial assets not measured at fair value through profit or loss | (857) | (18.3) | (12.0) | (1,049) |

| Provisions or reversal of provisions and other results | (34) | (46.9) | (41.3) | (63) |

| Profit (loss) before tax | 1,354 | 43.6 | 127.3 | 943 |

| Income tax | (417) | 120.5 | n.s. | (189) |

| Profit (loss) for the period | 937 | 24.3 | 77.8 | 754 |

| Non-controlling interests | (353) | 24.7 | 68.0 | (283) |

| Net attributable profit (loss) | 585 | 24.1 | 84.2 | 471 |

| Balance sheets | 30-09-25 | 𝚫 % | 𝚫 % (1) | 31-12-24 |

| Cash, cash balances at central banks and other demand deposits | 7,393 | (17.0) | (6.8) | 8,906 |

| Financial assets designated at fair value | 10,528 | (3.3) | 6.4 | 10,884 |

| Of which: Loans and advances | 209 | 2.2 | 2.2 | 205 |

| Financial assets at amortized cost | 51,598 | 3.2 | 11.1 | 49,983 |

| Of which: Loans and advances to customers | 47,804 | 2.0 | 9.8 | 46,846 |

| Tangible assets | 1,107 | (13.3) | (9.7) | 1,277 |

| Other assets | 2,516 | (14.7) | (7.7) | 2,948 |

| Total assets/liabilities and equity | 73,142 | (1.2) | 7.2 | 73,997 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 2,649 | 28.6 | 29.5 | 2,060 |

| Deposits from central banks and credit institutions | 3,844 | (10.4) | (4.9) | 4,292 |

| Deposits from customers | 50,438 | (0.6) | 7.7 | 50,738 |

| Debt certificates | 3,691 | (1.6) | 6.3 | 3,752 |

| Other liabilities | 5,706 | (5.9) | 6.9 | 6,066 |

| Regulatory capital allocated | 6,814 | (3.9) | 4.6 | 7,090 |

| Relevant business indicators | 30-09-25 | 𝚫 % | 𝚫 % (1) | 31-12-24 |

| Performing loans and advances to customers under management (2) | 47,730 | 2.3 | 10.1 | 46,663 |

| Non-performing loans | 2,183 | (8.6) | (4.8) | 2,387 |

| Customer deposits under management (3) | 50,438 | (0.6) | 7.7 | 50,738 |

| Off-balance sheet funds (4) | 8,406 | 5.9 | 21.5 | 7,936 |

| Risk-weighted assets | 53,465 | (5.4) | 2.6 | 56,489 |

| RORWA (5) | 2.27 | 1.94 | ||

| Efficiency ratio (%) | 43.9 | 47.5 | ||

| NPL ratio (%) | 4.1 | 4.5 | ||

| NPL coverage ratio (%) | 93 | 88 | ||

| Cost of risk (%) | 2.43 | 2.87 | ||

| (1) At constant exchange rate. (2) Excluding repos. (3) Excluding repos and including specific marketable debt securities. (4) Includes mutual funds and customer portfolios in Colombia and Peru. (5) For more information on the calculation methodology, as well as the calculation of the metric at the consolidated Group level, see Alternative Performance Measures at this report. |

||||

| SOUTH AMERICA. DATA PER COUNTRY (MILLIONS OF EUROS) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Country | Operating income | Net attributable profit (loss) | |||||||

| Jan.-Sep.25 | 𝚫 % | 𝚫 % (1) | Jan.-Sep.24 | Jan.-Sep.25 | 𝚫 % | 𝚫 % (1) | Jan.-Sep.24 | ||

| Argentina | 503 | 7.0 | n.s. | 470 | 104 | (25.0) | n.s. | 138 | |

| Colombia | 466 | (6.0) | 0.3 | 496 | 122 | 33.6 | 42.6 | 91 | |

| Peru | 918 | 0.7 | 0.2 | 912 | 227 | 31.0 | 30.4 | 173 | |

| Other countries (2) | 358 | 101.5 | 113.8 | 177 | 133 | 92.4 | 106.2 | 69 | |

| Total | 2,245 | 9.2 | 38.0 | 2,056 | 585 | 24.1 | 84.2 | 471 | |

| (1) At constant exchange rates. (2) Chile (Forum), Uruguay and Venezuela. Additionally, it includes eliminations and other charges. |

|||||||||

| SOUTH AMERICA. RELEVANT BUSINESS INDICATORS PER COUNTRY (MILLIONS OF EUROS) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Argentina | Colombia | Peru | ||||||

| 30-09-25 | 31-12-24 | 30-09-25 | 31-12-24 | 30-09-25 | 31-12-24 | |||

| Performing loans and advances to customers under management (1)(2) | 7,660 | 4,783 | 16,555 | 15,609 | 18,710 | 18,314 | ||

| Non-performing loans (1) | 308 | 70 | 798 | 966 | 906 | 1,081 | ||

| Customer deposits under management (1)(3) | 9,930 | 6,281 | 17,295 | 17,178 | 19,290 | 19,432 | ||

| Off-balance sheet funds (1)(4) | 2,545 | 1,935 | 2,836 | 2,539 | 3,023 | 2,440 | ||

| Risk-weighted assets | 11,068 | 11,037 | 18,054 | 18,868 | 18,676 | 20,384 | ||

| RORWA (5) | 1.87 | 3.65 | 0.91 | 0.46 | 3.21 | 2.40 | ||

| Efficiency ratio (%) | 54.6 | 59.5 | 45.2 | 46.9 | 37.6 | 36.5 | ||

| NPL ratio (%) | 3.8 | 1.4 | 4.5 | 5.7 | 4.0 | 4.9 | ||

| NPL coverage ratio (%) | 88 | 145 | 89 | 82 | 99 | 90 | ||

| Cost of risk (%) | 4.91 | 4.48 | 2.24 | 2.83 | 1.77 | 2.83 | ||

| (1) Figures at constant exchange rates. (2) Excluding repos. (3) Excluding repos and including specific marketable debt securities. (4) Includes mutual funds and customer portfolios (in Colombia and Peru, preliminary data as of September 30, 2025). (5) For more information on the calculation methodology, as well as the calculation of the metric at the consolidated Group level, see Alternative Performance Measures at this report. |

||||||||

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and results, will be given at constant exchange rates. These rates, together with the changes at current exchange rates, can be found in the attached tables of the financial statements and relevant business indicators.

Activity and results

The most relevant aspects related to the area's activity during the first nine months of 2025 were:

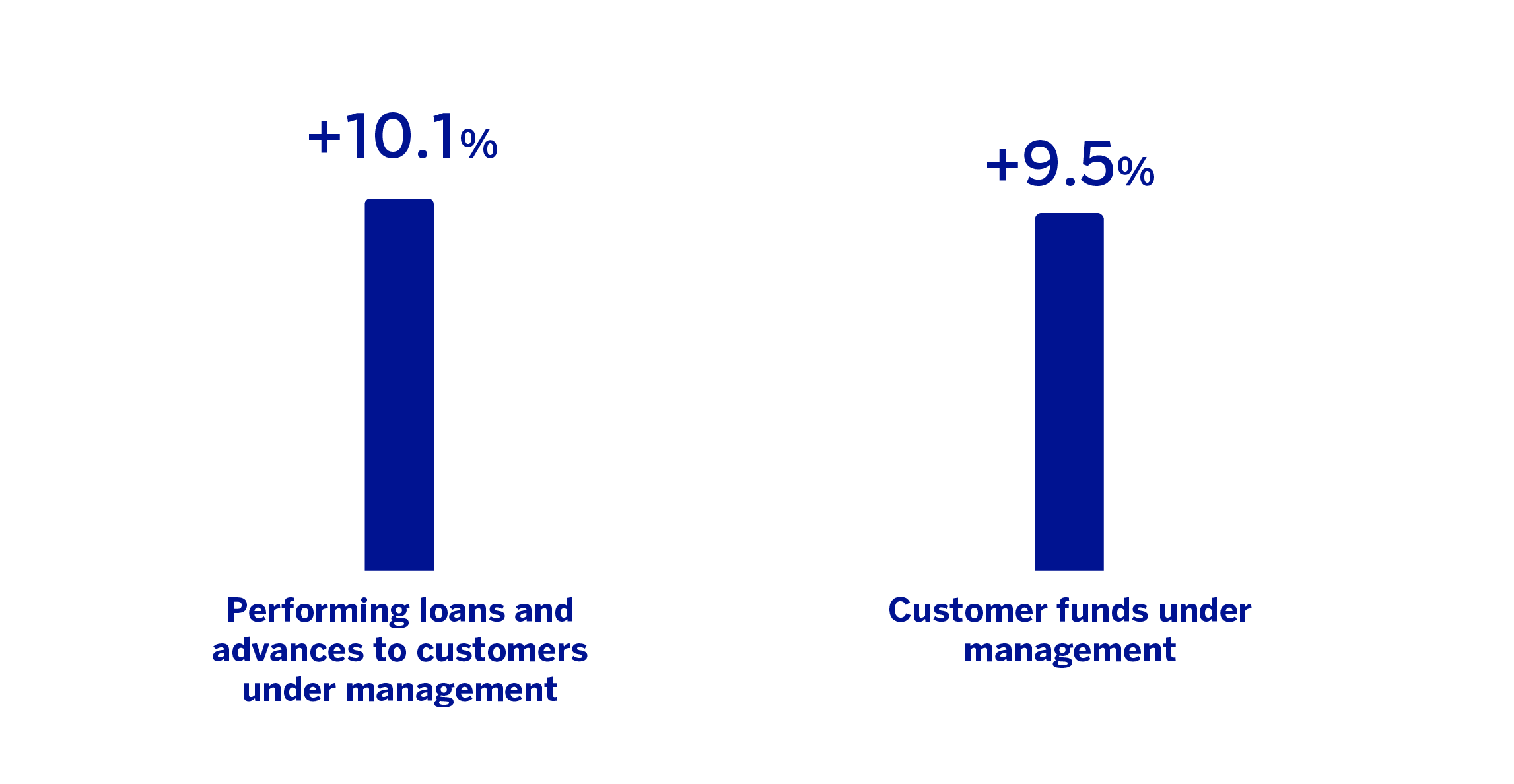

Lending activity (performing loans under management) recorded an increase of +10.1%, with a more dynamic growth in the wholesale portfolio that grew at a rate of 10.5%, above the growth of the retail portfolio (+9.7%).

Customer funds under management grew by 9.5% compared to the closing balances at the end of 2024, where the evolution of off-balance sheet funds (+21.5%) and time deposits (+10.6%) stand out.

The most relevant aspects related to the area's activity during the third quarter of the year 2025 have been:

Lending activity registered a positive variation of 3.1%, mainly supported by the dynamism of commercial loans (+2.4%), credit consumption and credit cards (+4.1%, overall).

With regard to the quality of the credit granted, the area's NPL ratio stood at 4.1%, which represents a decrease of 11 basis points compared to the previous quarter, favored by the performance in Peru and Colombia. For its part, the coverage ratio for the area was 93%, which represents an increase of 355 basis points compared to the end of June, also driven by Peru and Colombia.

Customer funds under management increased at a rate of 5.0%, with growth of 4.3% in customer deposits and 9.3% in off-balance sheet funds.

South America generated a net attributable profit of €585m at the end of the first nine months of 2025, which represents a year-on-year growth of 24.1% at current exchange rates, mainly derived from a less negative hyperinflation adjustment in Argentina, along with a better performance of net fees and commissions, and with a more reduced level of loan-loss provisions.

The impact of the adjustment for hyperinflation implies, among other effects, recording in the income statement the loss on the net monetary position of the Argentina subsidiaries under "Other operating income and expenses" and amounted to €277m in the period January - September 2025, much lower than the €1,178m recorded in the period January - September 2024.

More detailed information on the most representative countries of the business area is provided below.

Argentina

Macro and industry trends

The outlook for economic growth deteriorated in the third quarter of 2025 due to the combination of high political uncertainty, high interest rates, and exchange rate pressures. BBVA Research has revised its GDP growth forecast for 2025 downwards to 4.5% (one percentage point lower than in the previous scenario) and expects a gradual moderation in growth to rates of 3% by 2026. Despite the volatility and the recent depreciation of the peso, inflation has maintained the correction path initiated in 2024: in September it stood at 32.1% and it is expected to reach 30% by the end of 2025 and may fall below 20% during the second half of 2026.

The banking system continues to grow at a high pace, although the inflation control entails that the credit and deposit volume growth is more moderate than in previous quarters. With data at the end of August 2025, total lending was increased by 136% compared to August 2024, favored by consumer, corporate and, above all, mortgage portfolios, which grew by 130%, 127% and 445% year-on-year, respectively. For their part, deposits continue to decelerate, and at the end of August recorded a year-on-year growth of 54%. Finally, the NPL ratio has rebounded due to the growth in household credit defaults, standing at 3.72% at the end of August 2025.

Activity and results

In the first nine months of 2025, performing loans under management grew by 60.1% (+10.1% in the third quarter), driven mainly by the growth in corporate loans and all the loans to individuals, highlighting the dynamism of mortgage loans (+134.7%) and growth in terms of volume of consumer loans (+72.0%) and credit cards (+37.3%). At the end of September 2025, the NPL ratio stood at 3.8%, an increase of 107 basis points compared to the end of June 2025, mainly due to retail portfolio NPL entries affecting the NPL coverage ratio, which stood at 88%, below the level recorded at the end of June 2025.

On balance sheet funds recorded a 58.1% growth in the first nine months of 2025 (+19.8% in the third quarter), with growth in time deposits (+99.8%) higher than demand deposits (+36.1%). For its part, mutual funds (off-balance sheet funds) also had a good performance on the same time horizon (+31.5%, +16.3% in the third quarter).

Regarding the evolution of the income statement16, the cumulative net attributable profit at the end of September 2025 stood at €104m, showing a significantly lower hyperinflationary impact than at the end of September 2024. Net interest income continues to be affected by price effect and the higher cost of funds due to the growth in customer balances, which was not offset by the higher lending volume. Net fees and commissions grew by 20.3% year-on-year, driven by payment methods activity. On the other hand, a significantly lower negative adjustment for hyperinflation was recorded (mainly reflected in the "Other operating income and expenses" line) and higher operating expenses, both in personnel (fixed compensation to staff) and in other operating expenses. With regard to loan-loss provisions, there was an increase in requirements in the retail portfolio, partly affected by a higher portfolio volume. As a result of the above, the cost of risk stood at 4.91%, which represents an increase of 44 basis points in the quarter. Thus, the result of the third quarter reached €13m, which represents a decrease from the previous quarter, mainly due to higher loan-loss provisions compared to the second quarter of 2025, due to greater requirements in the retail and fixed income portfolios, where in the second quarter there were releases due to an improvement in the internal rating of the national government bond portfolio. This was partially offset by the favorable performance of net fees and commissions and a less negative hyperinflation adjustment.

Colombia

Macro and industry trends

Economic activity remained relatively robust during the first half of 2025, supported by the dynamism of private consumption and fiscal spending. BBVA Research expects the recovery to continue in the coming quarters, estimating GDP growth for 2025 at 2.5%, two tenths above the previous scenario and raising it to 2.7% for 2026. The increase in the household spending has also contributed to limit the reduction in the inflation: in September, the overall rate reached 5.2%, and it is expected to close the year and start 2026 at around 5%. This price environment, together with fiscal pressures and domestic uncertainty, has led the central bank to keep its benchmark interest rate unchanged at 9.25%: a level that could extend into the second half of 2026, at which point monetary policy could become more expansionary with rate cuts to around 8.5% at the end of the year.

Total credit growth in the banking system stood at 6.1% year-on-year in August 2025. As in previous months, the system's lending continued to be driven by corporate credit and mortgage loans, with growth of 6.2% and 11.0% respectively. As for consumer credit remained virtually flat in August shows a slightly increased dynamism than in previous months, with growth in year-on-year terms of 3.2%. On the other hand, total deposits grew by 10.1% year-on-year at the end of August 2025, with a more balanced evolution by portfolios than in previous quarters. Thus, demand and time deposits grew by 9.9% and 10.3% year-on-year respectively. The system's NPL ratio has improved in the last few months, placing at 4.22% in August 2025, 88 basis points below the figure for the same month of the previous year.

Activity and results

Lending activity grew at a rate of 6.1% compared to the end of 2024, and 2.0% in the third quarter. In terms of asset quality indicators, they improved with respect to the end of 2024: the NPL ratio stood at 4.5%, a decrease of 49 basis points with respect to the previous quarter, as a result of the containment of inflows and the good recovery dynamics of the quarter, as well as the write-offs mainly in retail portfolios. On the other hand, the coverage ratio rose 381 basis points in the quarter, placing at 89% due to the decrease in non-performing loans.

Customer funds grew by 2.1% compared to the end of 2024, mainly thanks to the growth of time deposits (+5.4%) and, to a lesser extent, to the increase of off-balance sheet funds (+11.7%). In the third quarter, off-balance sheet funds grew by 9.5% and offset the lower customer balances.

The cumulative net attributable profit at the end of September 2025 stood at 122 million euros, that is, 33.6% higher than at the end of the same period of the previous year (at current exchange rates), favored by a more efficient cost management, and particularly, a lower level of provisions for impairment on financial assets associated with the lower requirements of the retail portfolio as a result of lower entries into NPLs. Third quarter net attributable profit stood at €48m, 20.6% above the previous quarter at current exchange rates, mainly as result of the dynamism of the recurring revenues and NTI, and lower loan-loss provisions needs in the retail portfolio, which have been reflected in a 19 basis points decrease in the quarter in the cumulative cost of risk as of September 30, 2025, which stood at 2.24%.

Peru

Macro and industry trends

Economic activity has maintained a relatively favorable performance during the first half of 2025, thanks to the dynamism of the domestic demand and support from gold and copper prices. According to BBVA Research, GDP growth could stand at 3.1% in 2025, in line with the previous forecast, and remain at around that level in 2026 amid growing domestic political uncertainty. Controlled inflation, which stood at 1.4% in September and is expected to rise gradually to 1.8% in December and 2.5% throughout 2026, and low interest rates, which could remain unchanged at the current 4.25%, support growth expectations going forward.

Total lending in the Peruvian banking system continued the trend of recent quarters and increased 4.8% year-on-year in August 2025, with growth in all portfolios. Thus, the consumer credit portfolio grew by 10.1% year-on-year, the mortgage portfolio increased by 6.4% and the corporate loan portfolio by 2.5% year-on-year. The system's total deposits lost momentum in August 2025, with year-on-year growth of 3.3% due to the contraction in time deposits (-1.4% year-on-year), which was partially offset by 5.8% growth in demand deposits. Finally, the system's NPL ratio continued on a downward trend, reaching a rate of 3.46% in August 2025.

Activity and results

Lending activity grew by 2.2% compared to the end of December 2024, focused on the retail portfolios, mainly mortgages and consumer loans, which offset the deleveraging in the wholesale portfolios. In the third quarter of 2025, lending growth stood at 1.7%, with growth in the retail portfolio (+3.2%) and stability in the wholesale portfolio (+0.5%). Regarding the asset quality indicators, the NPL ratio was lower than at the end of June 2025 (-29 basis points) placing at 4.0%, where ongoing strong recovery performance and management of non-performing loans during the quarter continue. The coverage ratio was 99%, representing an increase of 716 basis points compared to the end of June, driven by the reduction in non-performing loans and the effect of the annual review of risk model parameters.

Customers funds under management increased during the first nine months of 2025 (+2.0%), thanks to the favorable performance of demand deposits (+5.9%) and off-balance sheet funds (+23.9%).

BBVA Peru's cumulative attributable profit stood at the end of September 2025 at €227m, which represents a year-on-year increase of 31.0% at current exchange rates, originated in lower provisions for impairment on financial assets, which were significantly lower than in the same period of 2024 (-36.7% at current exchange rates) due, among other factors, to a lower requirement for retail products as a result of the improved asset quality of the portfolio in the last quarters. The net attributable profit of the quarter stood at € 71m, which is a variation of -2.1% compared to the previous quarter, at current exchange rates, mainly as a result of the loan-loss provisions made in the quarter, originated in the annual review of the risk model parameters. Thus, the cumulative cost of risk at the end of September 2025 stood at 1.77%, +24 basis points above the cumulative cost of risk at the end of June, although it is still below the cumulative cost of risk at the end of 2024. This development was partially offset by the strong performance of recurring revenue from the banking business.

16 At current rates, that is, the impact of exchange rate fluctuations on the profit and loss account is not excluded.

Read legal disclaimer of this report.