Rest of Business

Highlights for the period January - September 2025

- Dynamism of lending activity in all geographical areas in the first nine months of 2025

- Outstanding evolution of fees

- Positive behavior of risk indicators

- Highest attributable profit within the quarterly series since 2024

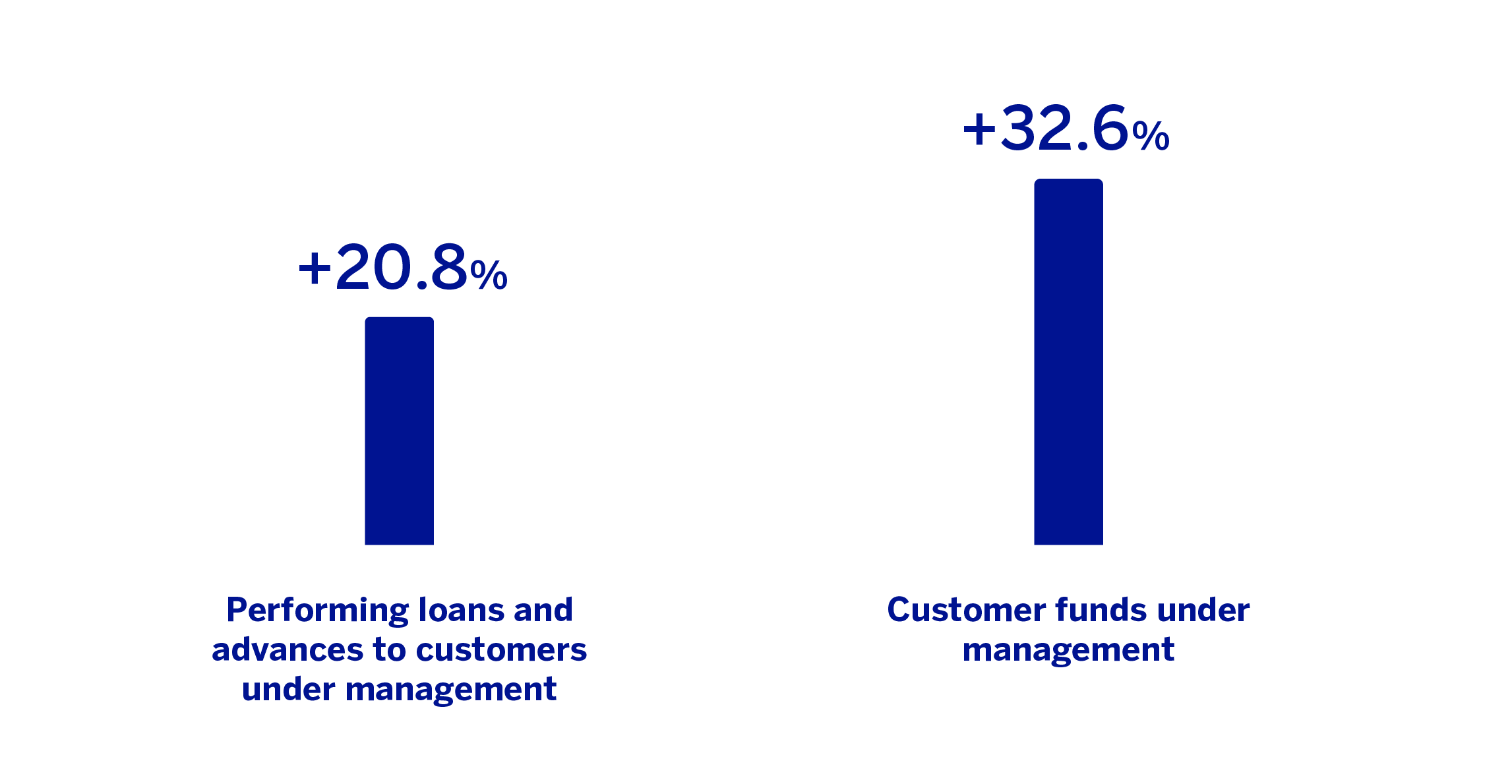

BUSINESS ACTIVITY (1) (VARIATION AT CONSTANT EXCHANGE RATES COMPARED TO 31-12-24)

(1) Excluding repos.

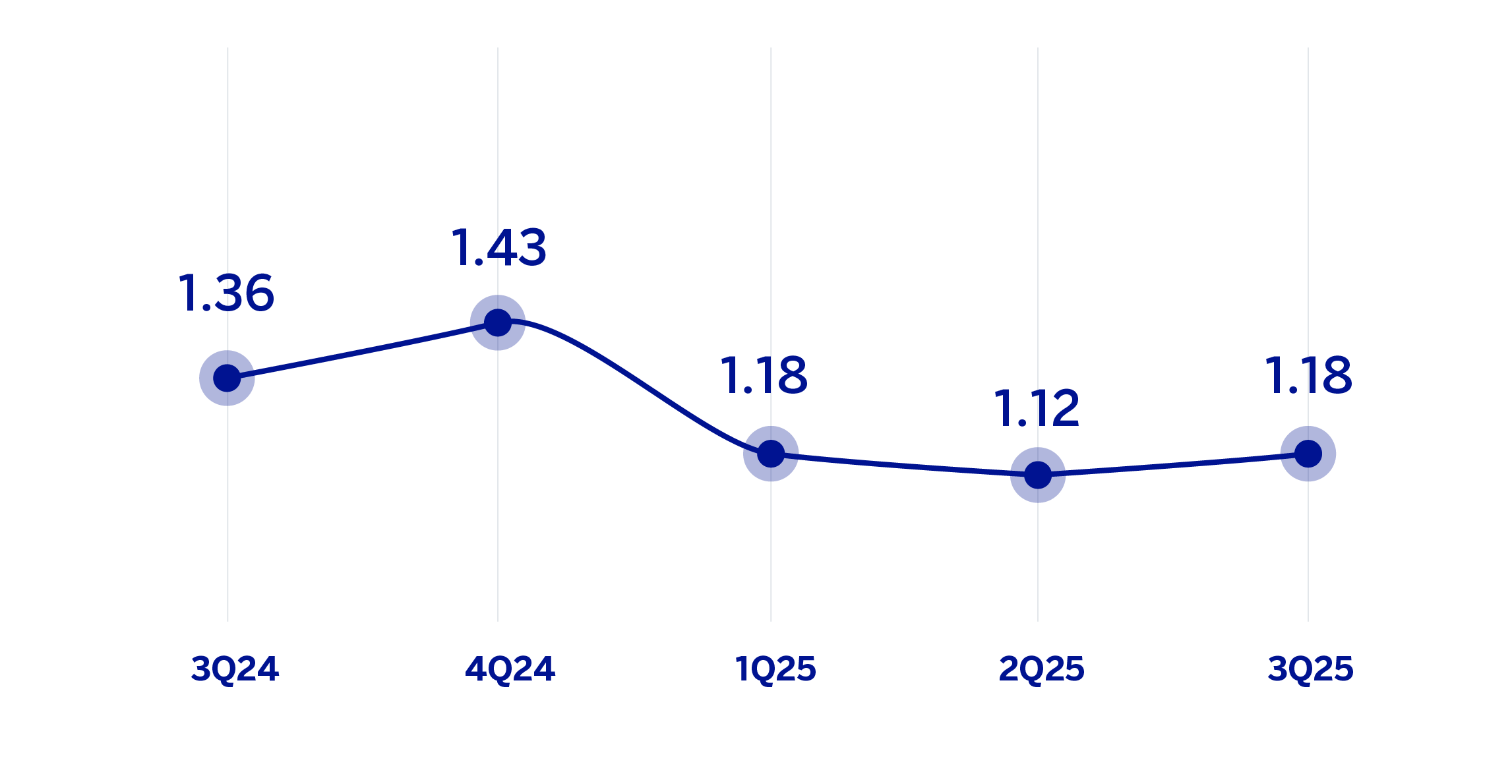

NET INTEREST INCOME / AVERAGE TOTAL ASSETS

(PERCENTAGE AT CONSTANT EXCHANGE RATES)

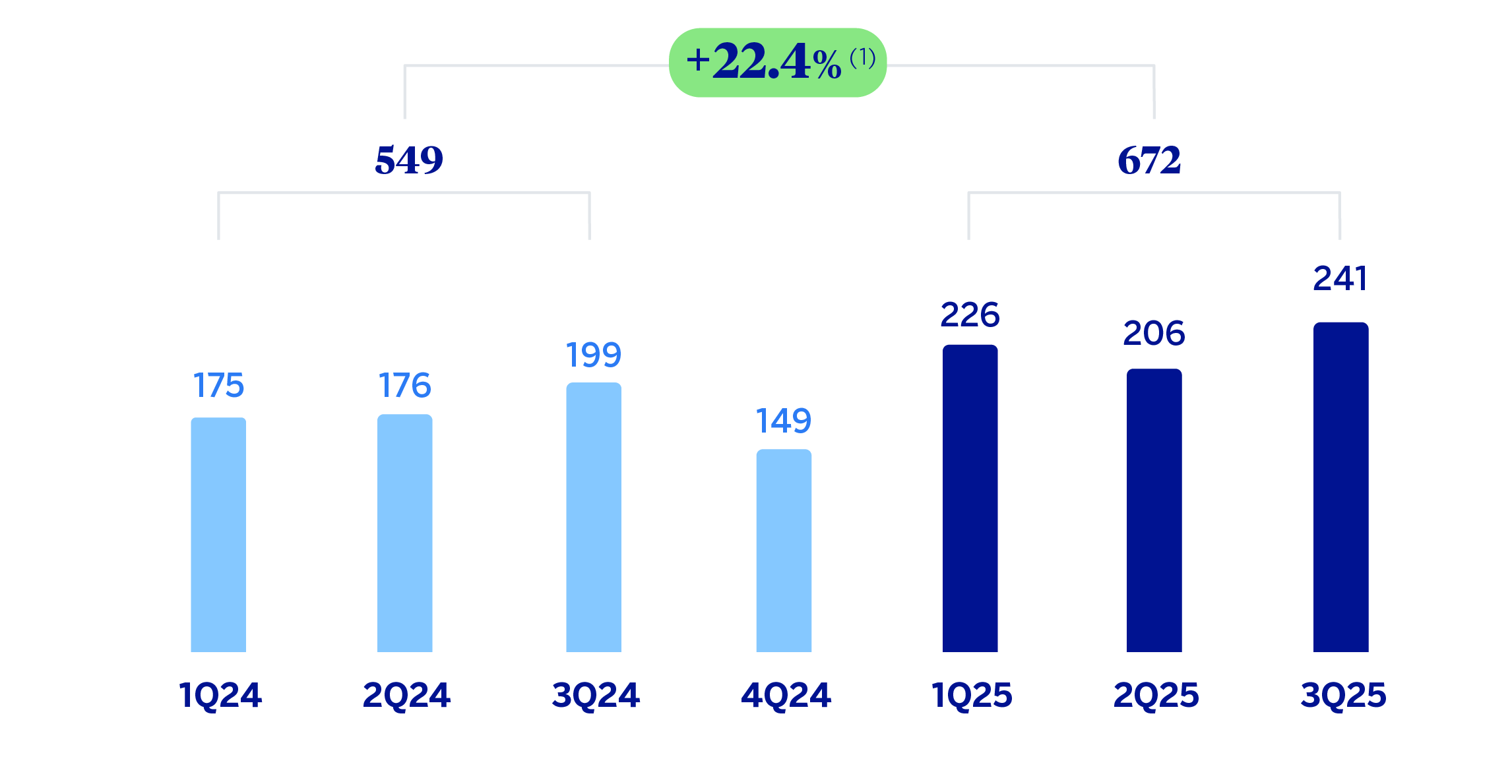

OPERATING INCOME

(MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES)

(1) At current exchange rates: +20.2%.

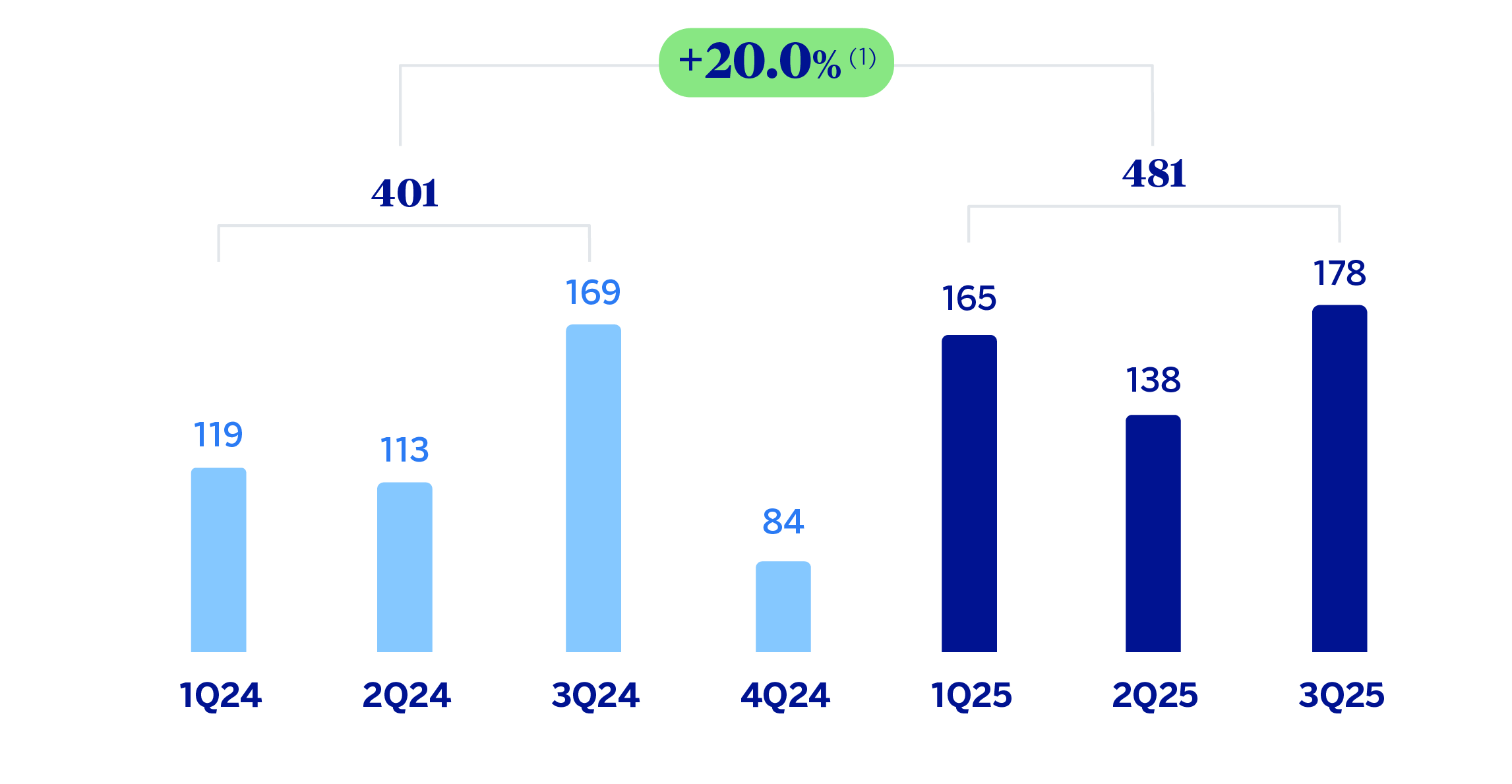

NET ATTRIBUTABLE PROFIT (LOSS) (

(MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES)

(1) At current exchange rates: +17.6%.

| FINANCIAL STATEMENTS AND RELEVANT BUSINESS INDICATORS (MILLIONS OF EUROS AND PERCENTAGE) | ||||

|---|---|---|---|---|

| Income statement | Jan.-Sep.25 | 𝚫 % | 𝚫 % (1) | Jan.-Sep.24 (2) |

| Net interest income | 596 | 14.1 | 15.7 | 522 |

| Net fees and commissions | 428 | 52.0 | 53.9 | 281 |

| Net trading income | 269 | 6.4 | 8.8 | 252 |

| Other operating income and expenses | 4 | 191.0 | 241.1 | 1 |

| Gross income | 1,296 | 22.6 | 24.5 | 1,058 |

| Operating expenses | (624) | 25.3 | 26.9 | (498) |

| Personnel expenses | (322) | 23.0 | 24.9 | (262) |

| Other administrative expenses | (273) | 27.8 | 29.2 | (214) |

| Depreciation | (28) | 27.5 | 28.9 | (22) |

| Operating income | 672 | 20.2 | 22.4 | 560 |

| Impairment on financial assets not measured at fair value through profit or loss | (47) | 28.1 | 27.7 | (36) |

| Provisions or reversal of provisions and other results | (11) | n.s. | n.s. | (3) |

| Profit (loss) before tax | 615 | 18.1 | 20.5 | 520 |

| Income tax | (134) | 19.7 | 22.0 | (112) |

| Profit (loss) for the period | 481 | 17.6 | 20.0 | 409 |

| Non-controlling interests | — | — | — | — |

| Net attributable profit (loss) | 481 | 17.6 | 20.0 | 409 |

| Balance sheets | 30-09-25 | 𝚫 % | 𝚫 % (1) | 31-12-24 |

| Cash, cash balances at central banks and other demand deposits | 9,152 | 9.6 | 23.2 | 8,348 |

| Financial assets designated at fair value | 2,043 | 25.6 | 33.4 | 1,627 |

| Of which: Loans and advances | 1,351 | 47.7 | 59.9 | 914 |

| Financial assets at amortized cost | 64,723 | 15.6 | 20.4 | 56,013 |

| Of which: Loans and advances to customers | 58,308 | 15.7 | 20.7 | 50,392 |

| Inter-area positions | — | — | — | — |

| Tangible assets | 230 | 11.7 | 21.2 | 206 |

| Other assets | 490 | 43.7 | 50.5 | 341 |

| Total assets/liabilities and equity | 76,639 | 15.2 | 21.2 | 66,534 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 788 | 22.7 | 37.7 | 642 |

| Deposits from central banks and credit institutions | 5,133 | 156.3 | 170.0 | 2,002 |

| Deposits from customers | 35,178 | 28.2 | 33.2 | 27,432 |

| Debt certificates | 1,684 | (2.2) | 2.6 | 1,721 |

| Inter-area positions (3) | 27,326 | (2.7) | 3.5 | 28,091 |

| Other liabilities (3) | 1,714 | 6.2 | 13.8 | 1,613 |

| Regulatory capital allocated | 4,817 | (4.3) | 0.4 | 5,033 |

| Relevant business indicators | 30-09-25 | 𝚫 % | 𝚫 % (1) | 31-12-24 |

| Performing loans and advances to customers under management (4) | 58,359 | 15.8 | 20.8 | 50,393 |

| Non-performing loans | 151 | (29.4) | (29.4) | 213 |

| Customer deposits under management (4) | 35,178 | 28.2 | 33.2 | 27,432 |

| Off-balance sheet funds (5) | 687 | 6.5 | 6.5 | 645 |

| Risk-weighted assets | 41,516 | (6.5) | (1.8) | 44,407 |

| RORWA (1)(5) | 1.70 | 1.27 | ||

| Efficiency ratio (%) | 48.1 | 50.4 | ||

| NPL ratio (%) | 0.2 | 0.3 | ||

| NPL coverage ratio (%) | 136 | 102 | ||

| Cost of risk (%) | 0.10 | 0.17 | ||

| (1) At constant exchange rate. (2) Revised balances. For more information, please refer to the “Business Areas” section. (3) Revised balances in 2024. (4) Excluding repos. (5) Includes pension funds. (6) For more information on the calculation methodology, as well as the calculation of the metric at the consolidated Group level, see Alternative Performance Measures at this report. |

||||

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and results, will be given at constant exchange rates. These rates, together with the changes at current exchange rates, can be found in the attached tables of the financial statements and relevant business indicators. Comments that refer to Europe exclude Spain.

Activity

The most relevant aspects of the evolution of BBVA Group's Rest of Business activity during the first nine months of 2025 were:

Lending activity (performing loans under management) grew by 20.8%. The United States and Europe are driving this growth, with significant transactions in project finance and corporate loans.

Customer funds under management recorded an increase of 32.6%, driven by customer deposits in Europe, supported by the performance of United Kingdom (CIB) and the digital bank in Germany, and, to a lesser extent, Asia.

The most relevant aspects of the evolution of BBVA Group's Rest of Business activity during the third quarter of 2025 were:

Lending (performing loans under management) recorded a growth of 4.2%, continuing the upward trend seen in recent quarters. Significant growth was observed in Investment Banking & Finance (IB&F), especially in the United States.

On the other hand, compared to the end of June, the NPL ratio decreased by 3 basis points to 0.2%, while the coverage ratio fell to 136%.

Customer funds under management recorded an increase of 34.3%, mainly due to the deposit balances, both demand and time deposits, by customers of branches in Europe, followed by customer deposits in the United States and Asia.

Results

Rest of Business achieved an accumulated net attributable profit of €481m during the first nine months of 2025, 20.0% higher than in the same period of the previous year, favored by the evolution of the recurring revenues and the NTI, which widely offset the increase in operating expenses.

In the year-on-year evolution of the main lines of the area's income statement at the end of September 2025, the following was particularly noteworthy:

Net interest income grew by 15.7% as a result of increased activity volumes and appropriate price management. By geographical areas, growth in the New York branch stood out.

Net fees and commissions had an excellent performance and increased by 53.9%, thanks to issuance activity in the primary debt market and relevant operations in project finance and corporate loans. Commissions originating in Europe and the United States stood out.

The NTI grew by 8.8% with the favorable performance of the United States standing out thanks to commercial activity in foreign exchange, credit and interest rates.

Increase in operating expenses of 26.9% mainly explained by higher expenses in Europe and, to a lesser extent, in the United States due to new hires and investment in strategic projects.

The impairment on financial assets line at the end of September 2025 recorded a balance of €-47m, figure which is higher than in the same period of the previous year, mainly originated in higher provisions in the United States. Meanwhile, the cumulative cost of risk at the end of September fell by 4 basis points compared to June to 0.10%, due in part to lower provisions for individual customers.

In the third quarter of 2025 and excluding the effect of the exchange rates fluctuations, the Group's Rest of Businesses as a whole generated a net attributable profit of €178m, 29.6% above that of the previous quarter. In the quarterly evolution, the good performance of recurring revenues and NTI were partially offset by the increase in the operating expenses associated with strategic plans.

Read legal disclaimer of this report.