The main trends observed in the global economy over the previous quarters were confirmed in the latter part of 2013. First, the recovery of the U.S. economy and the start of the gradual withdrawal of the extraordinary monetary stimuli by the Federal Reserve. Second, the European Central Bank’s (ECB) cut in its base rate to an all-time low, in order to support the economic recovery of the Eurozone. The improvement of the macroeconomic fundamentals in emerging markets and the fact that their exchange rates have on the whole been flexible, have led to an orderly adaptation to the Fed’s monetary policy transition.

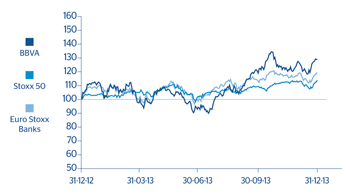

Financial markets began the quarter facing the threat of a possible default by the U.S. Treasury, the exit by the Fed from its expansive monetary policy and the consequent value readjustment in emerging assets in international portfolios. Most of these uncertainties began to ease toward the end of 2013, as reflected in the gains of the main stock-market indices. The general European index, the Stoxx 50, posted a quarterly gain of 5.2% at the end of December. The Ibex 35 and the Eurozone bank index (Euro Stoxx Banks) rose by 8.0% and 12.4% respectively.

Equity analysts consider that BBVA’s earnings in the third quarter of 2013 stand out from other Spanish banks due to the strength of its balance sheet and BBVA’s excellent capital position, as well as its more conservative risk management policy compared with the rest of the Spanish banking system. As a result, most analysts continue to classify BBVA as the best investment option for taking advantage of the opportunities derived from Spain’s imminent economic recovery. The Group’s earnings in Mexico and South America have also been very positive, and in some cases have exceeded market expectations.

As a result of the above factors, the BBVA share gained significantly in 2013. At the end of December, the share price had risen over the quarter by 8.3% and by 28.6% over the previous 12 months, closing as of 31-Dec-2013 at €8.95 per share. This price represents a market capitalization of €51,773m, a price/book value ratio of 1.1, a P/E ratio of 23.2 (calculated on the BBVA Group’s net attributable profit for 2013) and a dividend yield of 4.1% (based on the new shareholder retribution policy announced last October 25th, 2013).

Following the rise of the share price in the third quarter, the average daily volume traded from October to December fell 39.3% to 39 million shares, a 24.1% decline in terms of average daily volume, to €340m.

As regards shareholder remuneration, a new dividend policy has been announced that will pay shareholders in cash, in line with earnings and the Group’s growth profile. This shift toward a 100% cash remuneration will be accompanied by a complement to the cash dividend through the “dividend-option” system during the transition period. The market has taken a positive view of this new policy’s focus on cash payment, and considers that there are good grounds for implementing it in the current circumstances.

The BBVA share and share performance ratios

|

|

31-12-13 | 30-09-13 |

|---|---|---|

| Number of shareholders | 974,395 | 980,481 |

| Number of shares issued | 5,785,954,443 | 5,724,326,491 |

| Daily average number of shares traded | 39,188,130 | 64,576,932 |

| Daily average trading (million euros) | 340 | 447 |

| Maximum price (euros) | 9.40 | 8.46 |

| Minimum price (euros) | 8.17 | 6.18 |

| Closing price (euros) | 8.95 | 8.26 |

| Book value per share (euros) | 8.18 | 8.27 |

| Market capitalization (million euros) | 51,773 | 47,283 |

| Price/book value (times) | 1.1 | 1.0 |

| PER (Price/earnings; times) | 23.2 | 13.7 |

| Yield (Dividend/price; %) (1) | 4.1 | 4.5 |

Share price index

(31-12-12=100)