Turkey

Highlights

- The dedollarization of the balance sheet continues

- Improvement of the NPL ratio and the cost of risk in the quarter

- Net attributable profit of the second quarter negatively affected by the strong depreciation of the Turkish lira

Business activity (1)

(VARIATION AT CONSTANT EXCHANGE RATE COMPARED TO 31-12-22)

(1) Excluding repos.

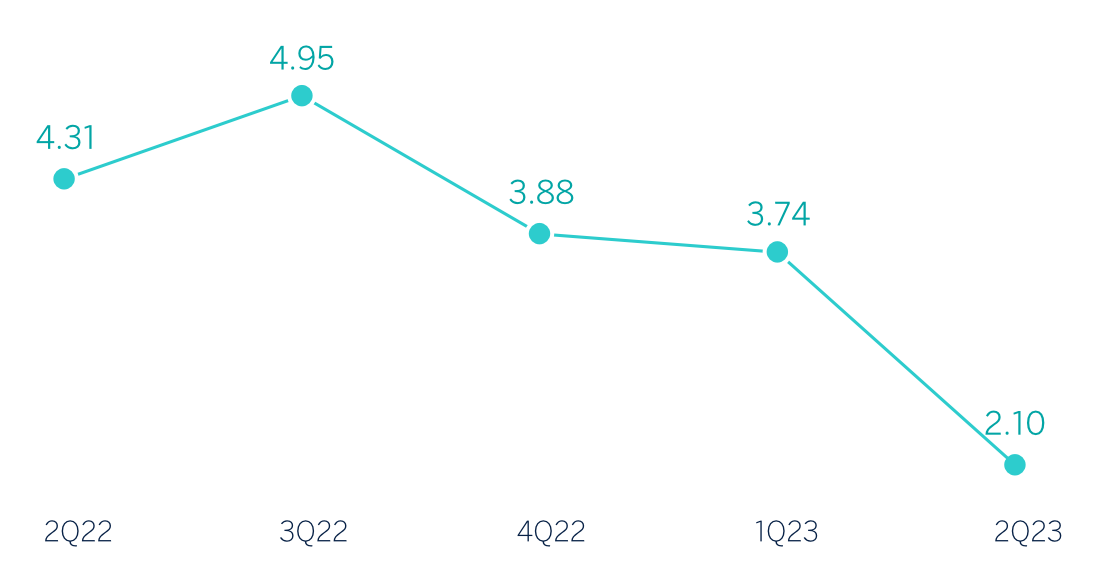

Net interest income / AVERAGE TOTAL ASSETS

(Percentage at current exchange rate)

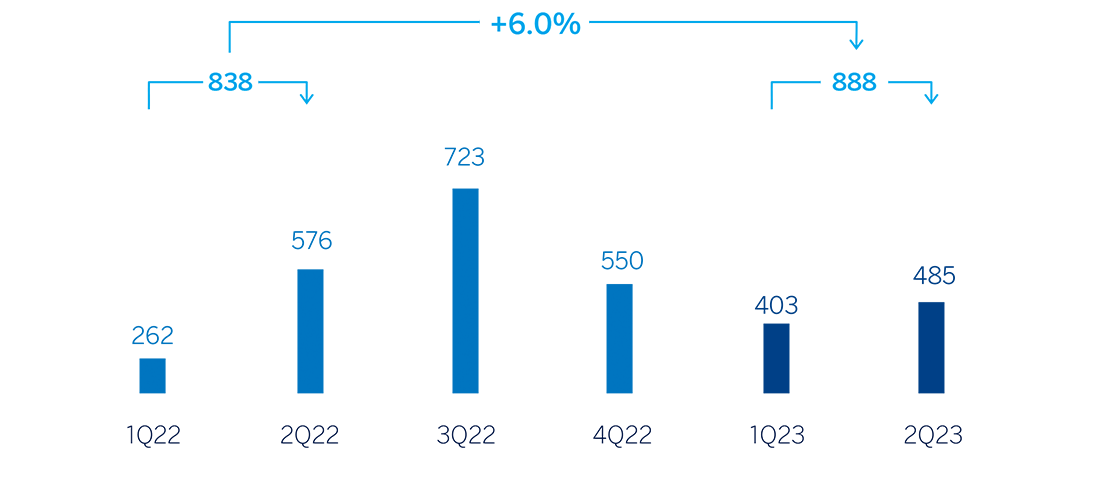

Operating income

(Millions of euros at current exchange rate)

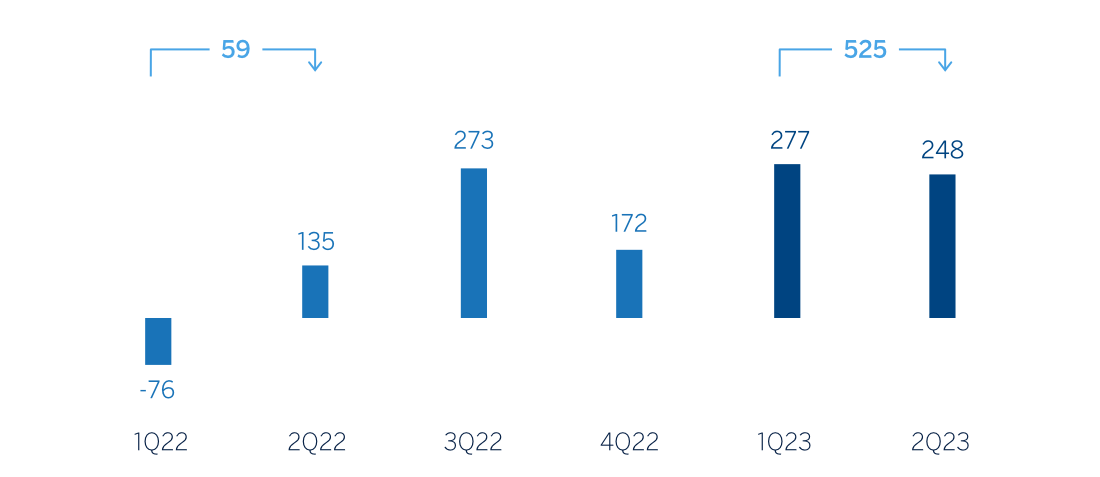

Net attributable profit (LOSS)

(Millions of euros at current exchange rate)

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 1H23 | ∆% | ∆% (1) | 1H22 (2) |

|---|---|---|---|---|

| Net interest income | 980 | (15.0) | 29.2 | 1,153 |

| Net fees and commissions | 285 | (5.6) | 43.6 | 302 |

| Net trading income | 394 | (0.2) | 52.7 | 395 |

| Other operating income and expenses | (180) | (65.0) | (81.4) | (515) |

| Gross income | 1,480 | 10.8 | n.s. | 1,335 |

| Operating expenses | (591) | 18.9 | 75.1 | (497) |

| Personnel expenses | (324) | 15.8 | 74.1 | (280) |

| Other administrative expenses | (206) | 34.4 | 100.7 | (153) |

| Depreciation | (61) | (4.5) | 25.0 | (64) |

| Operating income | 888 | 6.0 | n.s. | 838 |

| Impairment on financial assets not measured at fair value through profit or loss | (55) | (68.2) | (51.4) | (171) |

| Provisions or reversal of provisions and other results | (47) | 37.5 | 81.5 | (34) |

| Profit (loss) before tax | 787 | 24.3 | n.s. | 633 |

| Income tax | (170) | (73.1) | (60.2) | (635) |

| Profit (loss) for the period | 617 | n.s. | n.s. | (2) |

| Non-controlling interests | (92) | n.s. | n.s. | 61 |

| Net attributable profit (loss) | 525 | n.s. | n.s. | 59 |

| Balance sheets | 30-06-23 | ∆% | ∆% (1) | 31-12-22 (2) |

|---|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 7,759 | 28.0 | 81.6 | 6,061 |

| Financial assets designated at fair value | 4,119 | (20.8) | 12.3 | 5,203 |

| Of which: Loans and advances | 1 | (76.0) | (66.0) | 3 |

| Financial assets at amortized cost | 52,531 | 1.8 | 44.3 | 51,621 |

| Of which: Loans and advances to customers | 35,673 | (4.7) | 35.1 | 37,443 |

| Tangible assets | 1,165 | (4.0) | 29.0 | 1,213 |

| Other assets | 1,750 | (9.7) | 26.2 | 1,938 |

| Total assets/liabilities and equity | 67,324 | 1.9 | 44.4 | 66,036 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 2,197 | 2.7 | 45.7 | 2,138 |

| Deposits from central banks and credit institutions | 2,346 | (18.3) | 15.9 | 2,872 |

| Deposits from customers | 50,793 | 9.6 | 55.5 | 46,339 |

| Debt certificates | 2,860 | (11.6) | 25.4 | 3,236 |

| Other liabilities | 1,851 | (61.0) | (45.6) | 4,741 |

| Regulatory capital allocated | 7,277 | 8.4 | 53.5 | 6,711 |

| Relevant business indicators | 30-06-23 | ∆% | ∆% (1) | 31-12-22 |

|---|---|---|---|---|

| Performing loans and advances to customers under management (3) | 35,604 | (4.3) | 35.8 | 37,191 |

| Non-performing loans | 2,056 | (20.8) | 12.3 | 2,597 |

| Customer deposits under management (3) | 49,520 | 8.6 | 54.1 | 45,592 |

| Off-balance sheet funds (4) | 6,800 | (2.0) | 39.1 | 6,936 |

| Risk-weighted assets | 50,672 | (10.0) | 27.5 | 56,275 |

| Efficiency ratio (%) | 39.9 | 33.5 | ||

| NPL ratio (%) | 4.2 | 5.1 | ||

| NPL coverage ratio (%) | 97 | 90 | ||

| Cost of risk (%) | 0.23 | 0.94 |

(1) At constant exchange rate.

(2) Restated balances according to IFRS17 - Insurance contracts.

(3) Excluding repos.

(4) Includes mutual funds and pension funds.

Macro and industry trends

There are incipient signs of changes in economic policy in general, and monetary policy in particular, since the general elections held in May 2023, which point to a gradual correction of the current macroeconomic distortions, especially the high external financing needs. In this regard, benchmark interest rates have been raised from 8.5% to 17.5% in July and are expected to continue rising in the coming months with the intention of controlling inflation, which reached 38.2% in June in year-on-year terms, in a context in which the speed of depreciation of the Turkish lira has increased. Economic growth could reach 4.5% in 2023, below the 5.6% expansion recorded in 2022, although well above BBVA Research's previous forecast (3.0%), largely due to the strong dynamism of economic activity in the first half of the year. Despite the high uncertainty, highly due to doubts about the duration and scale of the current economic policy adjustment process, the most likely scenario is that the pace of GDP growth will moderate going forward, reducing pressures on inflation, which would nevertheless remain at high levels, fueled by fiscal stimulus, exchange rate depreciation and the high inertia of the price revision process, among other factors.

Regarding the Turkish banking system, with data as of May 2023, where the effect of inflation remains clear, the total volume of credit in the system increased by 53.7% year-on-year, in line with the growth of previous months. The credit stock continues to be driven by the acceleration in consumer and credit card lending (+110.9% year-on-year) while corporate lending grew to a lesser extent (+41.8% year-on-year). Total deposits grew less in May than in previous months (+58.4% year-on-year). Growth in Turkish lira deposits remains stable (+126.1%) while dollar deposits grew much more slowly (+8.6%). The dollarization stood at 40% at the end of May 2023 (vs. 59% a year earlier, driven by regulatory measures commissioned last year to encourage the growth of Turkish lira deposits. As for the system's NPL ratio, it has continued to fall in recent months, and in May it was 1.75% (86 basis points lower than the same month of 2022).

Unless expressly stated otherwise, all comments below on rates of changes for both activity and results, will be presented at constant exchange rates. These rates, together with changes at current exchange rates, can be observed in the attached tables of the financial statements and relevant business indicators. For the conversion of these figures, the end of period exchange rate as of June 30, 2023 is used, reflecting the considerable depreciation by the Turkish lira in the last year, in particular during the second quarter of 2023, with a negative impact in the accumulated results at the end of June 2023. Likewise, the Balance sheet, the Risk-Weighted Asset (RWA) and the equity are affected.

Activity

The most relevant aspects related to the area’s activity in the first half of 2023 were:

- Lending activity (performing loans under management) increased by 35.8% between January and June 2023, mainly driven by the growth in Turkish lira loans (+27.6%). This growth was mainly supported by the performance of credit cards and, to a lesser extent, of loans to companies. Foreign currency loans (in U.S. dollars) increased by 5.4%, boosted by the increase in activity with customers focused on foreign trade (with natural hedging of exchange rate risk).

- Customer deposits (75% of the area's total liabilities as of June 30, 2023) remained the main source of funding for the balance sheet and increased by 54.1%. Noteworthy is the positive performance of Turkish lira time deposits (+73.3%), which represent a 79.4% of total customer deposits in local currency. Balances deposited in foreign currency (in U.S. dollars) continued their downward path and decreased by 10.5%, with transfers from foreign currency time deposits to Turkish lira time deposits observed under a foreign exchange protection scheme. Thus, as of June 30, 2023, Turkish lira deposits accounted for 59% of total customer deposits in the area. For its part, off-balance sheet funds grew by 39.1%.

The most relevant aspects related to the area’s activity in the second quarter of 2023 were:

- Lending activity (performing loans under management) increased by 24.1%, mainly driven by the growth in Turkish lira loans (+15.6%), since loans in foreign currency deleveraged.

- In terms of asset quality, the NPL ratio decreased 12 basis points from that at the end of March 2023 to 4.2% and 89 basis points below the figure for the end of 2022 due to the good performance in the wholesale portfolio, in repayments, which offset the entries into default in the retail portfolio. The NPL coverage ratio recorded a reduction of 136 basis points in the quarter to 97% as of June 30, 2023 due to the release of a provision to a one-time customer.

- Customer deposits increased by 35.0% mainly thanks to the performance of Turkish lira time deposits (+23.6%) and off- balance sheet funds grew by 23.2%. For its part, balances deposited in foreign currency (in U.S. dollars) continued their downward path and decreased by 2.6%.

Results

Turkey generated a net attributable profit of €525m during the first half of 2023, which compares very positively with the result reached in the first half of 2022, both periods reflecting the impact of the application of hyperinflation accounting. The accumulated result at the end of June 2023 reflects the positive impact of the revaluation for tax purposes of the real estate and other depreciable assets of Garanti BBVA AS which has generated a credit in corporate income tax expense, due to the higher tax base of the assets, amounting to approximately €205m.

In the tax area, after its publication in the Official Gazette on July 15, 2023, Law No. 7456 on Additional Motor Vehicle Tax and Amendments to Certain Laws as well as Decree Law No. 375, for Compensation of Economic Losses Caused by the Earthquakes on February 6, 2023, has entered into force in Turkey. Among other aspects, this Law provides for the modification of the general corporate income tax rate in Turkey from 20% to 25%. However, the general tax rate for banks and financial institutions is increased to 30% (it was already 25%). This change is applicable to profits generated in tax periods beginning on or after January 1, 2023. The Group does not expect significant impacts from this reform.

As mentioned above, the year-on-year comparison of the accumulated income statement at the end of June 2023 at current exchange rate is affected by the strong depreciation of the Turkish lira in the last year. To exclude this effect, the highlights of the first half results at constant exchange rate are summarized below:

- Net interest income recorded a year-on-year growth of 29.2%, reflecting growth in Turkish lira loan, as well as lower funding costs and higher income from the securities portfolio in Turkish lira. This is partially offset by the decline in the Turkish lira spread.

- Net fees and commissions increased by 43.6%, favored by the performance in payment systems fees, money transfers, brokerage activity and guarantees and asset management.

- NTI showed an excellent performance (+52.7%) thanks to the increase in the results of the Global Markets unit, favored by foreign exchange operations and portfolio sales.

- The other operating income and expenses line showed a balance of €-180m, which compares favorably with the previous year. This line includes among others, the loss in the value of the net monetary position due to the country's inflation rate, which stood below the loss recorded in the first half of 2022, partially offset by the income derived from inflation-linked bonds (CPI linkers), which were lower in relation to those obtained in the first half of 2022. It is also worth highlighting the improved performance of Garanti BBVA's subsidiaries, also included in this line.

- Operating expenses increased by 75.1%, with growth both in personnel, as a result of salary improvements to compensate for the loss of purchasing power of the workforce, and in general expenses, where higher expenses in technology stand out, as well as the institutional donation made by the BBVA Group to help those affected by the earthquake that struck an area in the south of the country last February.

- Impairment on financial assets decreased by 51.4%, mainly due to strong improvements in credit quality and repayments in the wholesale segments which led to a significant improvement in the accumulated cost of risk as of June 30, 2023 to 0.23% from the 0.88% at the end of June of the previous year.

- The provisions and other results line closed June 2023 with a higher loss than in the same half of the previous year, mainly due to the update of the provisions for commitments with personnel.

In the second quarter of 2023, the net attributable profit decreased by 10.5% compared to the previous quarter at current exchange rate due to the strong depreciation of the Turkish lira since the end of March (-26% versus the euro). On the other hand, the quarterly inflation rate of the second quarter of the year (6.4%) has been lower than the registered in the previous quarter (12.5%). Thus, the negative adjustment for hyperinflation was significantly smaller.