Other information: Corporate & Investment Banking

Highlights

- Growth in customer funds

- Good performance of recurrent revenues and outstanding NTI evolution

- Improvement in efficiency

- Growth in net attributable profit

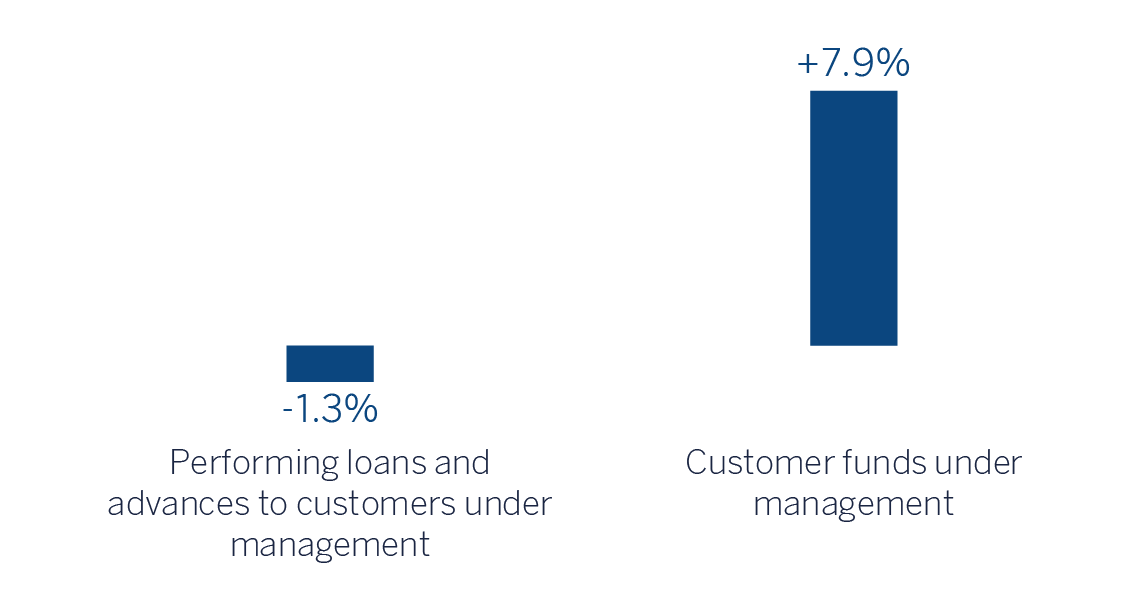

Business activity (1)

(VARIATION AT CONSTANT EXCHANGE RATES COMPARED TO

31-12-22)

(1) Excluding repos.

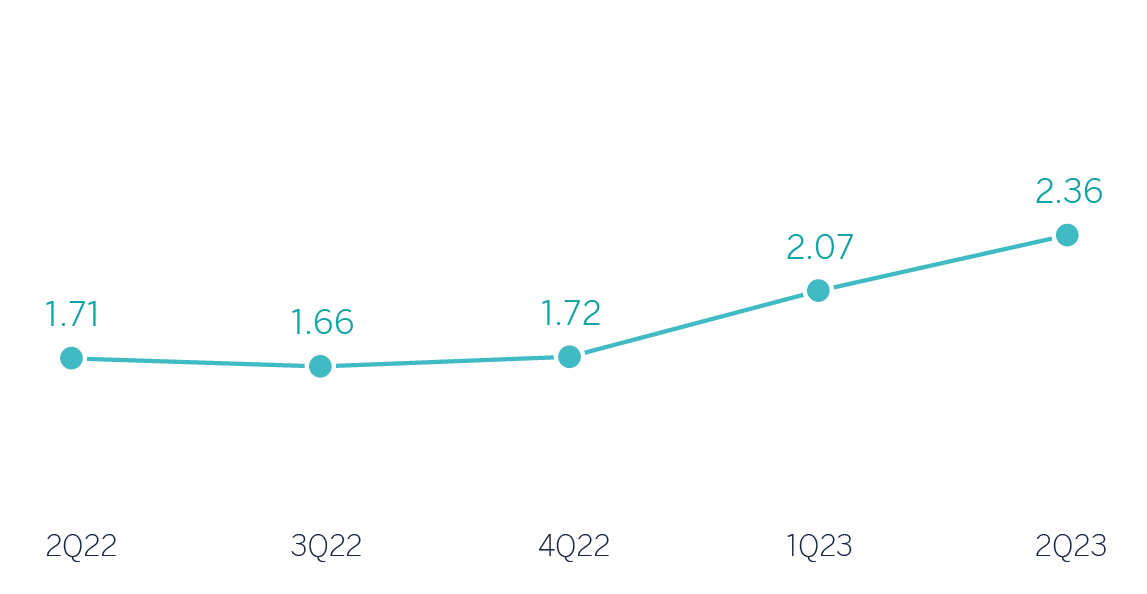

Gross income / AVERAGE TOTAL ASSETS

(Percentage. Constant exchange rates)

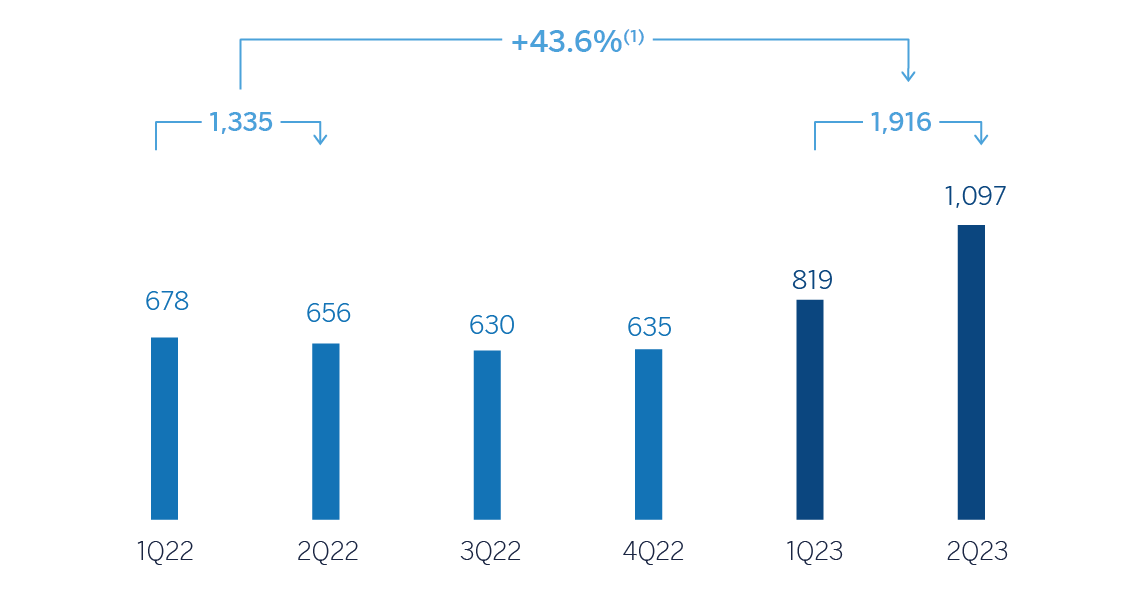

Operating income

(Millions of euros at constant exchange rates)

(1) At current exchange rates: +31.2%.

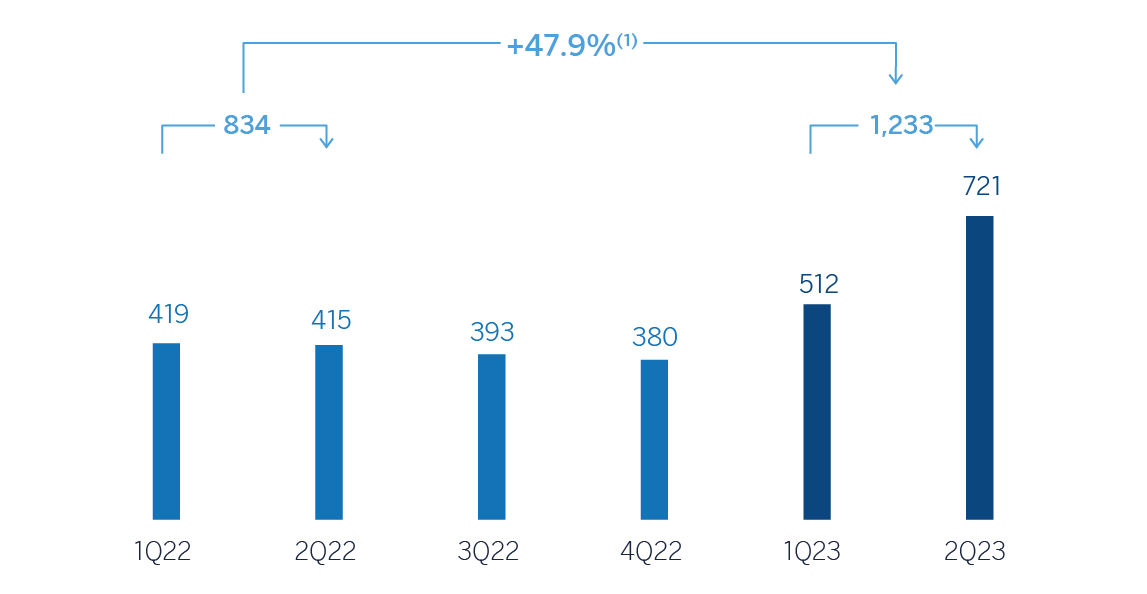

Net attributable profit (LOSS)

(Millions of euros at constant exchange rates)

(1) At current exchange rates: +38.5%.

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 1H23 (1) | ∆% | ∆% (2) | 1H22 |

|---|---|---|---|---|

| Net interest income | 1,000 | 5.8 | 13.5 | 945 |

| Net fees and commissions | 537 | 24.0 | 28.9 | 433 |

| Net trading income | 1,026 | 64.8 | 82.8 | 623 |

| Other operating income and expenses | (41) | 160.9 | 157.2 | (16) |

| Gross income | 2,523 | 27.0 | 36.9 | 1,986 |

| Operating expenses | (607) | 15.5 | 19.4 | (525) |

| Personnel expenses | (284) | 18.9 | 21.3 | (239) |

| Other administrative expenses | (271) | 15.6 | 22.5 | (234) |

| Depreciation | (52) | (0.8) | (2.1) | (52) |

| Operating income | 1,916 | 31.2 | 43.6 | 1,461 |

| Impairment on financial assets not measured at fair value through profit or loss | (19) | n.s. | 103.1 | 5 |

| Provisions or reversal of provisions and other results | 12 | 35.6 | 54.2 | 9 |

| Profit (loss) before tax | 1,909 | 29.5 | 43.2 | 1,475 |

| Income tax | (523) | 25.8 | 38.6 | (416) |

| Profit (loss) for the period | 1,386 | 30.9 | 45.0 | 1,059 |

| Non-controlling interests | (154) | (8.9) | 25.8 | (169) |

| Net attributable profit (loss) | 1,233 | 38.5 | 47.9 | 890 |

| Balance sheets | 30-06-23 | ∆% | ∆% (2) | 31-12-22 |

|---|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 5,354 | (3.1) | (4.0) | 5,524 |

| Financial assets designated at fair value | 157,133 | 33.2 | 31.4 | 117,958 |

| Of which: Loans and advances | 72,812 | 60.5 | 60.6 | 45,360 |

| Financial assets at amortized cost | 89,267 | (0.2) | 0.2 | 89,440 |

| Of which: Loans and advances to customers | 75,870 | (1.7) | (1.1) | 77,208 |

| Inter-area positions | - | - | - | - |

| Tangible assets | 54 | 3.5 | 2.3 | 52 |

| Other assets | 13,755 | n.s. | n.s. | 862 |

| Total assets/liabilities and equity | 265,563 | 24.2 | 23.5 | 213,836 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 129,517 | 31.1 | 29.7 | 98,790 |

| Deposits from central banks and credit institutions | 27,114 | 29.2 | 28.5 | 20,987 |

| Deposits from customers | 55,331 | 14.8 | 14.6 | 48,180 |

| Debt certificates | 5,757 | 8.8 | 7.4 | 5,292 |

| Inter-area positions | 30,159 | 17.8 | 18.9 | 25,609 |

| Other liabilities | 6,565 | 59.2 | 47.5 | 4,124 |

| Regulatory capital allocated | 11,121 | 2.5 | 5.0 | 10,855 |

| Relevant business indicators | 30-06-23 | ∆% | ∆% (2) | 31-12-22 |

|---|---|---|---|---|

| Performing loans and advances to customers under management (3) | 75,796 | (1.9) | (1.3) | 77,291 |

| Non-performing loans | 785 | 4.2 | 33.8 | 753 |

| Customer deposits under management (3) | 48,633 | 2.9 | 2.7 | 47,270 |

| Off-balance sheet funds (4) | 4,166 | 138.0 | 167.8 | 1,750 |

| Efficiency ratio (%) | 24.0 | 28.5 |

(1) For the translation of the income statement in those countries where hyperinflation accounting is applied, the punctual exchange rate as of March 31, 2023 is used.

(2) At constant exchange rates.

(3) Excluding repos.

(4) Includes mutual funds, customer portfolios and other off-balance sheet funds.

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and results, will be given at constant exchange rates. For the conversion of these figures in those countries in which accounting for hyperinflation is applied, the end of period exchange rate as of June 30, 2023 is used. These rates, together with changes at current exchange rates, can be found in the attached tables of financial statements and relevant business indicators.

Activity

The most relevant aspects related to the area's activity in the first half of 2023 were:

- Lending activity (performing loans under management) was -1.3% lower than at the end of December 2022. By products, the evolution of Investment Banking & Finance is noteworthy, and by geographical areas, in the United States the evolution of corporate loans (Corporate Lending) stands out. The evolution of this line in the rest of the geographies continues to be slower than expected.

- Customer funds grew by (7.9%) between January and June 2023, maintaining the positive trend in price management.

The most relevant aspects related to the area's activity in the second quarter of 2023 were:

- Lending activity remained stable -0.2%, highlighting the evolution of Investment Banking & Finance.

- Customer funds grew by 4.8% mainly due to the performance in Mexico.

Results

CIB generated a net attributable profit of €1,233m in the first half of 2023. These results, which do not include the application of hyperinflation accounting, represent an increase of 47.9% on a year-on-year basis and reflects the contribution of the diversification of products and geographical areas, as well as the progress of the Group's wholesale businesses in its strategy, leveraged on globality and sustainability, with the purpose of being relevant to its clients.

The contribution by business areas, excluding the Corporate Center, to CIB's accumulated net attributable profit at the end of June 2023 was as follows: 16% Spain, 24% Mexico, 30% Turkey, 14% South America and 16% Rest of Business. By business line, GTB's contribution was particularly noteworthy, thanks to factoring and confirming campaigns and liability price management, although all lines recorded a positive evolution.

The most relevant aspects of the year-on-year evolution in the income statement of this aggregate are summarized below:

- Net interest income was 13.5% higher than in the same period last year, partly thanks to the good year-on-year performance of the business. GTB stands out, which evolved favorably in all geographic areas.

- Net fees and commissions grew by 28.9%, with positive evolution of all business lines, especially in GTB and Global Markets, benefited from an increase in operations in the primary debt market. By geographical areas, all had a favorable evolution, especially Spain and Mexico.

- Excellent NTI performance (+82.8%), mainly due to the performance of the Global Markets unit due to revenues generated by foreign currency operations in emerging markets. As for the geographical areas, all except Spain showed growth.

- The operating expenses increased by 19.4%, driven by higher personnel expenses, partly due to measures taken by the Group to compensate for the loss in purchasing power of the workforce and salary review processes, as well as the increase in the number of employees in the area. On the other hand, general expenses continue to be affected by inflation and higher technology-related expenses. Despite this, the efficiency ratio improved to at 24.0%, which represents an improvement compared to the same period of the previous year.

- Provisions for impairment on financial assets increased mainly originating in Turkey.

In the second quarter of 2023 and excluding the effect of the variation in exchange rates, the Group's wholesale businesses generated a net attributable profit of €721m (+40.9% compared to the previous quarter). This performance was mainly due to the good performance of NTI together with recurring income (net interest income and net fees and commissions).