South America

Highlights

- Growth in lending activity and customer funds

- NPL and NPL coverage ratio improvement in the quarter

- Favorable behavior of recurring income in the quarter

- Improvement of the efficiency ratio

Business activity (1)

(VARIATION AT CONSTANT EXCHANGE RATES COMPARED TO

31-12-21)

(1) Excluding repos.

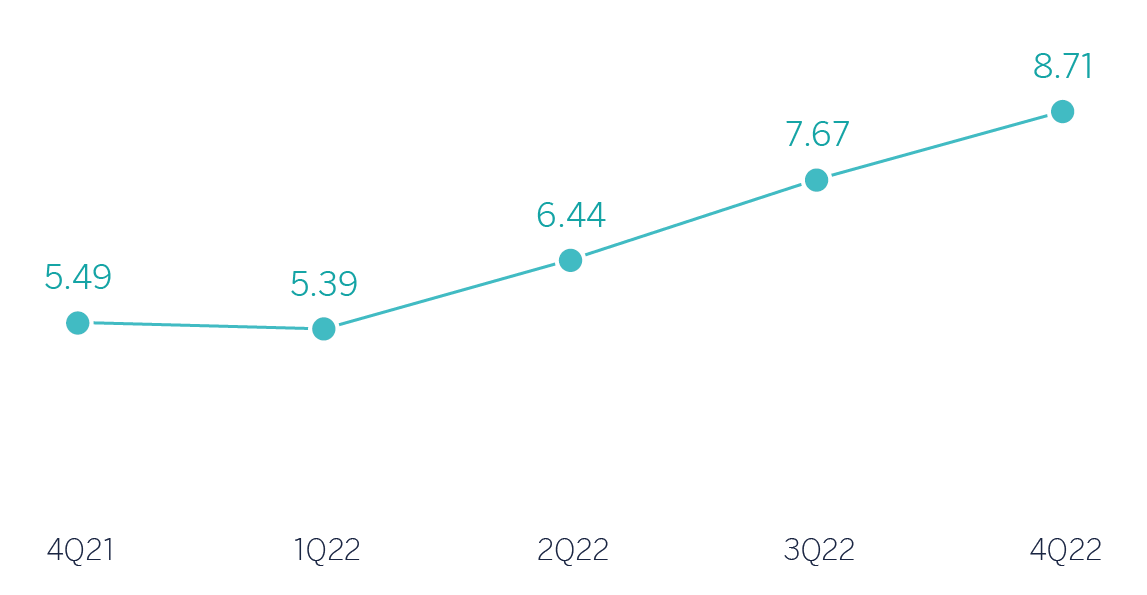

Net interest income / AVERAGE TOTAL ASSETS

(PERCENTAGE AT CONSTANT EXCHANGE RATES)

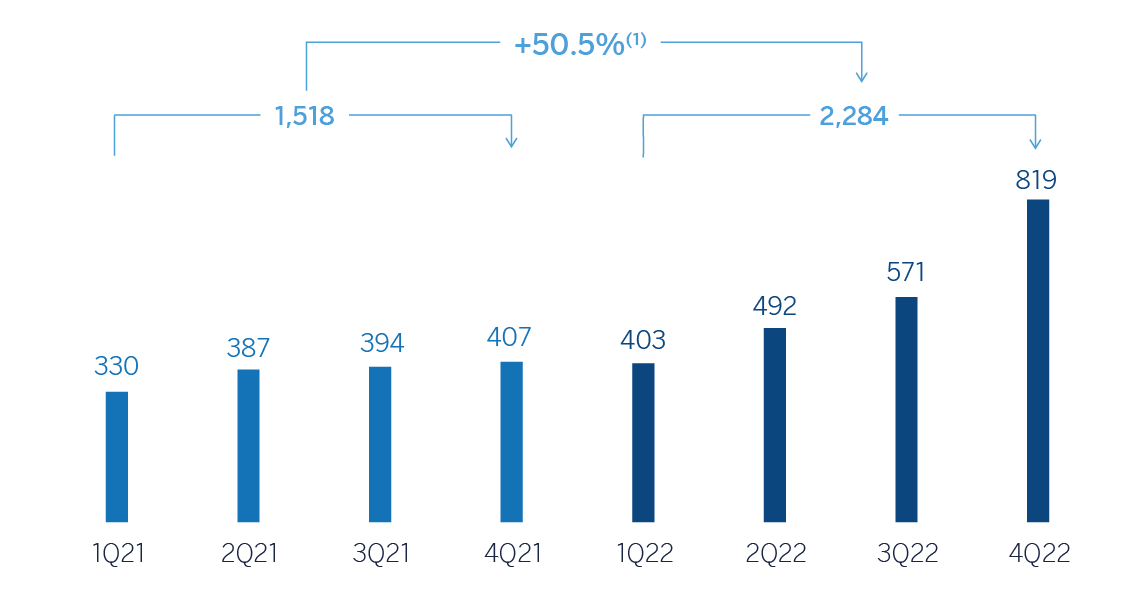

Operating income

(Millions of euros at constant exchange rates)

(1) At current exchange rates: +39.3%.

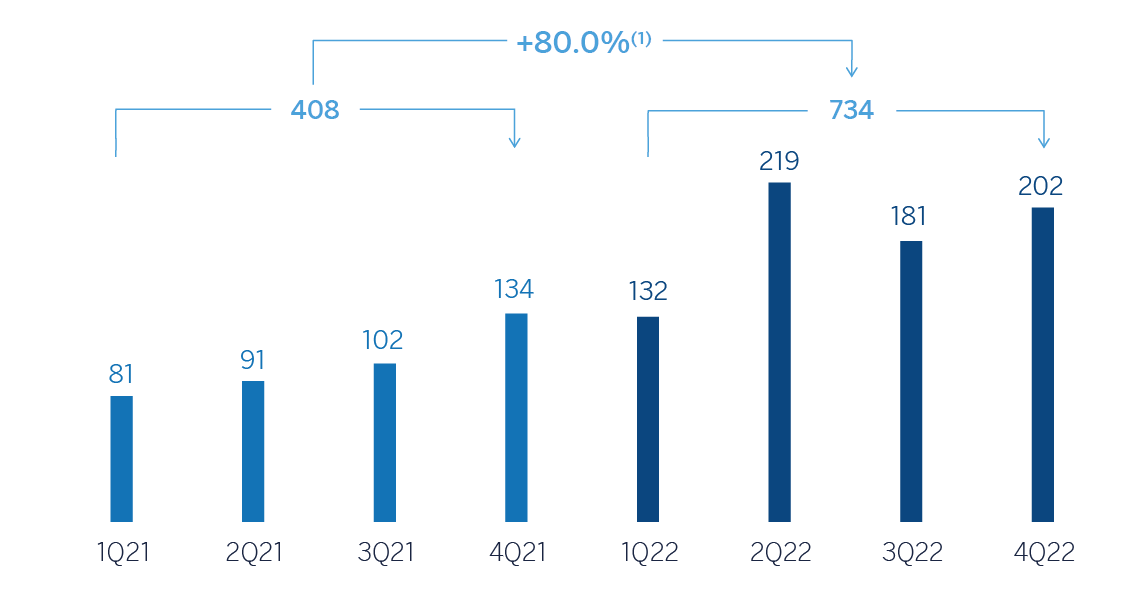

Net attributable profit (LOSS)

(Millions of euros at constant exchange rates)

(1) At current exchange rates: +54.4%.

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 2022 | ∆% | ∆% (1) | 2021 (2) |

|---|---|---|---|---|

| Net interest income | 4,137 | 44.7 | 57.7 | 2,859 |

| Net fees and commissions | 778 | 32.2 | 38.7 | 589 |

| Net trading income | 447 | 37.7 | 40.9 | 324 |

| Other operating income and expenses | (1,102) | 80.4 | 94.9 | (611) |

| Gross income | 4,261 | 34.8 | 45.1 | 3,162 |

| Operating expenses | (1,977) | 29.8 | 39.2 | (1,522) |

| Personnel expenses | (947) | 30.7 | 40.5 | (724) |

| Other administrative expenses | (860) | 31.7 | 43.6 | (653) |

| Depreciation | (170) | 17.3 | 15.9 | (145) |

| Operating income | 2,284 | 39.3 | 50.5 | 1,639 |

| Impaiment on financial assets not measured at fair value through profit or loss | (762) | 22.4 | 21.9 | (622) |

| Provisions or reversal of provisions and other results | (94) | 21.8 | 23.4 | (77) |

| Profit (loss) before tax | 1,429 | 52.0 | 74.9 | 940 |

| Income tax | (345) | 23.0 | 39.7 | (281) |

| Profit (loss) for the period | 1,083 | 64.3 | 90.2 | 659 |

| Non-controlling interests | (349) | 90.1 | 115.9 | (184) |

| Net attributable profit (loss) | 734 | 54.4 | 80.0 | 476 |

- (1) At constant exchange rates.

- (2) Restated balances. For more information, please refer to the “Business Areas” section.

| Balance sheets | 31-12-22 | ∆% | ∆% (1) | 31-12-21 |

|---|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 7,695 | (10.0) | (4.7) | 8,549 |

| Financial assets designated at fair value | 10,563 | 47.2 | 56.3 | 7,175 |

| Of which: Loans and advances | 152 | (3.3) | 10.0 | 157 |

| Financial assets at amortized cost | 40,755 | 8.0 | 11.6 | 37,747 |

| Of which: Loans and advances to customers | 38,526 | 11.3 | 13.4 | 34,608 |

| Tangible assets | 1,088 | 21.6 | 24.5 | 895 |

| Other assets | 1,966 | 11.8 | 20.0 | 1,758 |

| Total assets/liabilities and equity | 62,067 | 10.6 | 15.3 | 56,124 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 2,813 | 49.4 | 62.0 | 1,884 |

| Deposits from central banks and credit institutions | 5,610 | 2.0 | (4.3) | 5,501 |

| Deposits from customers | 40,042 | 10.2 | 15.7 | 36,340 |

| Debt certificates | 2,956 | (8.0) | (8.1) | 3,215 |

| Other liabilities | 4,770 | 13.4 | 30.7 | 4,207 |

| Regulatory capital allocated | 5,874 | 18.0 | 23.0 | 4,977 |

| Relevant business indicators | 31-12-22 | ∆% | ∆% (1) | 31-12-21 |

|---|---|---|---|---|

| Performing loans and advances to customers under management (2) | 38,566 | 11.5 | 13.7 | 34,583 |

| Non-performing loans | 1,835 | 1.3 | 1.3 | 1,813 |

| Customer deposits under management (3) | 40,074 | 10.2 | 15.7 | 36,364 |

| Off-balance sheet funds (4) | 17,760 | 9.5 | 10.3 | 16,223 |

| Risk-weighted assets | 46,834 | 8.1 | 12.6 | 43,334 |

| Efficiency ratio (%) | 46.4 | 48.2 | ||

| NPL ratio (%) | 4.1 | 4.5 | ||

| NPL coverage ratio (%) | 101 | 99 | ||

| Cost of risk (%) | 1.69 | 1.65 |

- (1) At constant exchange rates.

- (2) Excluding repos.

- (3) Excluding repos and including specific marketable debt securities.

- (4) Includes mutual funds, customer portfolios in Colombia and Peru and pension funds.

South America. Data per country (Millions of euros)

| Operating income | Net attributable profit (loss) | |||||||

|---|---|---|---|---|---|---|---|---|

| Country | 2022 | ∆% | ∆% (1) | 2021 (2) | 2022 | ∆% | ∆% (1) | 2021 (2) |

| Argentina | 468 | 84.4 | n.s. | 254 | 185 | 218.0 | n.s. | 58 |

| Colombia | 605 | 7.8 | 8.9 | 561 | 238 | 6.6 | 7.6 | 223 |

| Peru | 932 | 37.3 | 20.7 | 679 | 206 | 74.3 | 53.1 | 118 |

| Other countries (3) | 279 | 91.6 | 82.8 | 145 | 106 | 38.3 | 32.6 | 76 |

| Total | 2,284 | 39.3 | 50.5 | 1,639 | 734 | 54.4 | 80.0 | 476 |

- (1) Figures at constant exchange rates.

- (2) Restated balances. For more information, please refer to the “Business Areas” section.

- (3) Bolivia, Chile (Forum), Uruguay and Venezuela. Additionally, it includes eliminations and other charges.

South America. Relevant business indicators per country (Millions of euros)

| Argentina | Colombia | Peru | ||||

|---|---|---|---|---|---|---|

| 31-12-22 | 31-12-21 | 31-12-22 | 31-12-21 | 31-12-22 | 31-12-21 | |

| Performing loans and advances to customers under management (1) (2) | 3,900 | 2,058 | 13,292 | 10,840 | 16,943 | 17,267 |

| Non-performing loans and guarantees given (1) | 64 | 50 | 600 | 613 | 1,054 | 1,073 |

| Customer deposits under management (1) (3) | 6,964 | 3,755 | 13,061 | 11,261 | 16,219 | 15,483 |

| Off-balance sheet funds (1) (4) | 2,303 | 1,059 | 2,046 | 2,088 | 1,453 | 1,813 |

| Risk-weighted assets | 8,089 | 6,775 | 15,279 | 14,262 | 17,936 | 18,016 |

| Efficiency ratio (%) | 61.3 | 69.0 | 40.6 | 37.0 | 37.2 | 38.2 |

| NPL ratio (%) | 1.6 | 2.3 | 4.2 | 5.0 | 4.9 | 4.9 |

| NPL coverage ratio (%) | 173 | 146 | 106 | 103 | 91 | 89 |

| Cost of risk (%) | 2.59 | 2.20 | 1.56 | 1.85 | 1.58 | 1.59 |

- (1) Figures at constant exchange rates.

- (2) Excluding repos.

- (3) Excluding repos and including specific marketable debt securities.

- (4) Includes mutual funds and customer portfolios (in Colombia and Peru).

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and results, will be given at constant exchange rates. These rates, together with the changes at current exchange rates, can be found in the attached tables of the financial statements and relevant business indicators.

Activity and results

The most relevant aspects related to the area's activity during the year 2022 were:

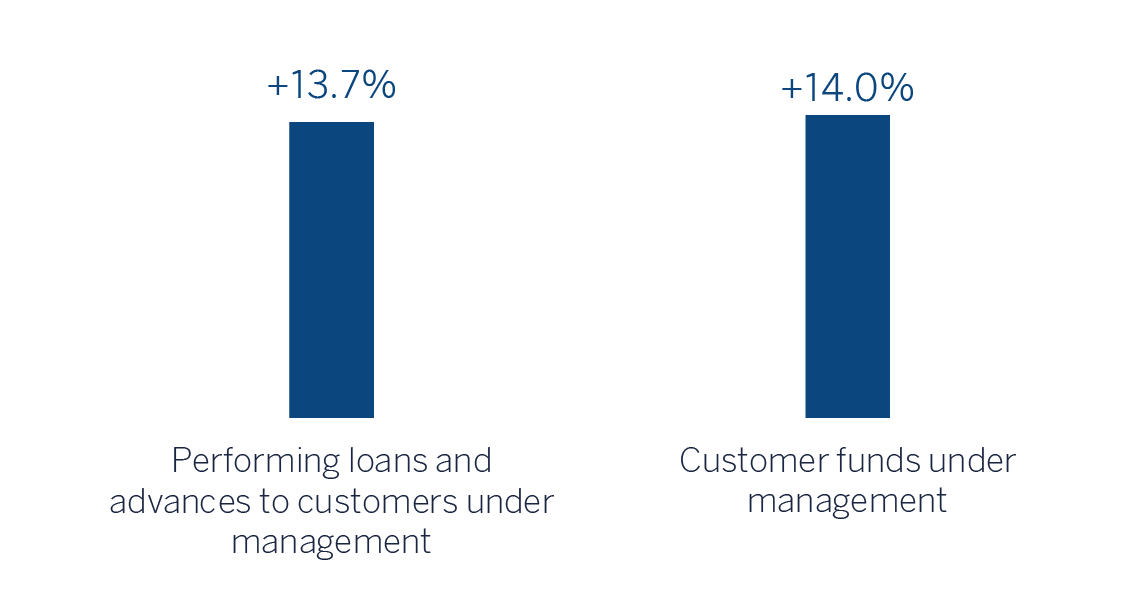

- Lending activity (performing loans under management) recorded an increase of +13.7%, with growth in all segments, particularly in the corporate (+10.0%) consumer (+20.3%) and credit cards (+56.3%) portfolios.

- Customer funds under management increased (+14.0%) compared to the closing balances at the end of 2021, with higher contribution from time deposits (+69.0%) in an environment of rising benchmark rates and, to a lesser extent, on off-balance sheet funds (+10.3%).

The most relevant aspects of the evolution of the area's activity in the last quarter of 2022 were:

- Lending activity (performing loans under management) was higher than in the previous quarter (+3.9%) with growth in all segments, in particular, the corporate (+3.3%), credit cards (+15.1%) and public sector (+18.0%) portfolios.

- With regard to asset quality, the NPL ratio stood at 4.1%, with reduction of 2 basis points in the quarter at the regional level, favored by the aforementioned growth in activity, with only Argentina and Chile as the countries with increase in the ratio. For its part, the NPL coverage rate reached 101%.

- Total customer funds increased by 2.0%, boosted by growth in customer deposits (+0.7%) and off-balance sheet funds (+4.9%).

South America generated a net attributable profit of €734m in the year 2022, which represents a year-on-year variation of +80.0%, mainly due to the improved performance of recurring income (+54.3%) and NTI, widely offsetting the growth of expenses, which in a highly inflationary environment throughout the region, increase below the gross income, the higher impact of the hyperinflation in Argentina, and higher loan-loss provisions for impairments on financial assets. With regard to the aforementioned inflation impact in Argentina, it stood at €-819m at the end of December 2022, notably above the €-395m accumulated at the end of December 2021. The aforementioned impacts are registered in the "Other operating income and expenses" heading of the area's income statement.

In the fourth quarter of 2022, and excluding the effect of exchange rate fluctuations, South America generated a net attributable profit of €202m, 11.9% above the previous quarter, which is mainly explained by both the good evolution of recurring income, especially by the net interest income, and the less negative adjustment for inflation in Argentina. This offset the higher operating expenses, both personal expenses -with wages improvement in some countries in a higher inflation environment and higher variable remuneration- and general expenses -especially in IT-, and the higher loan-loss provisions for impairments on financial assets.

More detailed information on the most representative countries of the business area is provided below:

Argentina

Macro and industry trends

Despite the less favorable global context and a local environment shaped by difficulty in correcting current macroeconomic distortions and meeting the targets set in the agreement reached in March with the International Monetary Fund, economic activity exhibited some dynamism in 2022. Available evidence suggests, according to BBVA Research, that GDP could have grown by close to 5.0% in 2022, one percentage point higher than previously forecast. Furthermore, the global environment, high inflation (94.8% in December; expected to reach around 99% in 2023 on average), financial volatility, uncertainty as to policy developments and limited scope for further stimulus measures support expectations of a slight contraction in GDP in 2023.

The balance sheet of the banking sector continues to grow at a stable pace but remains driven by high inflation. At the end of November 2022, total lending grew by 64.0% compared to the same month in 2021, favored by both consumer and corporate portfolios, which reached year-on-year growth rates of 66.7% and 65.6%, respectively. Meanwhile, deposits sped up their growth compared to previous months: they grew by 94.1% year-on-year in November 2022. Finally, the NPL ratio remained stable at 3.1% in October 2022 (181 basis points lower than in the same month in 2021).

Activity and results

- For the year as a whole, performing loans under management increased by 89.6%, a figure that is well below inflation, with growth in both the business portfolio (+117.2%) and the retail portfolio (+71.8%), highlighting in the latter credit cards (+74.6%) and, to a lesser extent, consumer loans (+69.0%). The NPL ratio stood at 1.6%, which represents an increase compared to the previous quarter (+5 basis points) due to new NPL entries from retail portfolios, but well below the end of 2021. For its part, the NPL coverage ratio increased in the quarter to 173% due to the increase in loan-loss provisions. In the last quarter of 2022 the lending activity evolution was driven by a positive performance of the business loans (+33.6%) and credit cards portfolio (+21.6%).

- Balance sheet funds grew by 85.5% in 2022, mainly due to the evolution of time deposits, both in the retail and wholesale segments, followed by demand deposits and mutual funds. Between October and December 2022, demand deposits increased above the time deposits (+27.8% versus +18.0%), and the mutual funds also performed favorably (+29.6%).

- The cumulative net attributable profit at the end of December 2022 stood at €185m, well above the figure achieved in 2021, mainly explained by strong growth of the net interest income derived from the activity increase and the higher securities portfolio contribution in a rising interest rates context. The year-on-year performance of commissions and NTI was also positive. The aforementioned was partially offset by a more negative inflation adjustment in the year and higher expenses and loan-loss provisions, mainly related to the fixed-income portfolio. In the fourth quarter of 2022 the net interest income performed favorably (+26.2%) which, together with a less negative inflation, offset the higher loan-loss provisions for impairments on financial assets, provisions and the higher tax expense.

Colombia

Macro and industry trends

Economic activity, in general, and domestic demand, in particular, have shown greater dynamism than expected in recent months. Growth in 2022 could reach 8.0%, above BBVA Research's previous forecast of 7.6%. In addition, high inflation (13.1% in December) prompted the Bank of the Republic to raise interest rates to 12.0% in December. In this context, and taking into account financial volatility and economic policy uncertainty, BBVA Research estimates further upward adjustments to interest rates in the near term, to around 13.0%. Inflation will remain relatively high in 2023 (11.7%, on average) and growth will slow significantly to around 0.7% in 2023 (unchanged from the previous forecast).

Total lending growth in the banking sector stood at 17.5% year-on-year in October 2022, driven by lending to households, especially consumer loans. Corporate credit growth sped up to 16.3% year-on-year as of September. Total deposits showed 15.1% year-on-year growth at the end of October 2022. There was a strong move toward time deposits (up 39.3% year-on-year) and a slowdown in the growth of demand deposits (up 4.9% year-on-year). The system's NPL ratio remained stable at around 3.70% in October 2022, a drop of 60 basis points from the same month in 2021.

Activity and results

- Lending activity showed a positive evolution throughout the year, accelerating quarter after quarter its growth rate compared to the end of 2021, reaching a year-on-year increase of 22.6% at the end of 2022. Noteworthy was the more dynamic performance in the wholesale portfolio (+37.9%), due to the business segment, although the retail portfolio also showed a favorable evolution (+13.4%). In terms of asset quality, slight decrease in the NPL ratio in the last quarter of the year (-3 basis points), which at the end of 2022 stood at 4.2%, favored by the aforementioned activity increase, and closing the year below the figure at the end of 2021. For its part, the NPL coverage ratio declined slightly in the quarter to 106%, but it stood above the previous year-end level. In the quarter, the lending activity increased by 5.3%, boosted by the wholesale segment, with growth in business (+9.4%) and public sector (+14.9%) portfolios.

- Customer deposits under management increased by 16.0% during the year 2022, as a result of the growth in time deposits (+54.0%), resulting from the successive rate hikes implemented by the central bank. In the fourth quarter of 2022, customer deposits increased by 4.5% thanks to the positive evolution of time deposits (+12.2%). For its part, off-balance sheet funds increased by 3.9% over the fourth quarter, but fell by 2.0% during the year.

- The cumulative net attributable profit at the end of the year 2022 stood at €238m, or 7.6% above that achieved in the previous year, favored by the evolution of recurring income and the NTI, as well as a contained level of provisions for impairment on financial assets. This offset the increase in operating expenses and income tax as a result of the increase in the tax rate from 34% to 38%. In the fourth quarter of 2022, the net interest income benefited from a higher managed lending volumes and more favorable rates in business portfolio, but it was offset by an operating expenses increase (+31.8%), impacted by the inflation and the higher variable remuneration to employees, as well as by an increase in provisions for impairment of financial assets (+23.2%), due to the recording of additional provisions in certain portfolios and sectors most vulnerable to the current environment -mainly rising interest rates, inflation and higher energy costs-. Thus, the result generated by BBVA Colombia between October and December 2022 reached €38m, a 34.0% below the previous quarter.

Peru

Macro and industry trends

Against a context of political instability, which could have a negative impact on economic activity, the recent indicators suggest GDP could have grown close to 2.7% in 2022, four tenths of a percentage point above BBVA Research's previous forecast. Furthermore, uncertainty about future policies, high inflation, high interest rates and the global economic slowdown will impact negatively on growth going forward. Thus, BBVA Research estimates growth to be around 2.5% in 2023, unchanged from its previous expectation. Inflation could remain high in 2023 (around 6,4%, on average), while official interest rates could reach around 8.0% in the coming months.

Total lending growth in the banking industry continued to moderate, reaching 3.1% year-on-year in November 2022. The biggest slowdown continues to be seen in credit to businesses, with the balance contracting to -2.9% year-on-year. However, consumer loans remained dynamic, growing by 24.2% year-on-year in November 2022, while the mortgage portfolio maintained a stable growth rate of around 8.0% year-on-year. The industry's total deposits continued to drop moderately (-0.4% year-on-year in November 2022), with a greater shift toward time deposits (24.9% year-on-year) to the detriment of demand deposits (-8.9% year-on-year). The NPL ratio across the banking system deteriorated slightly to 3.19% in November 2022 (15 basis points above the same month in 2021).

Activity and results

- The year-on-year variation of lending activity stood at -1.9% at the end of December 2022, with an unfavorable evolution of the business segment (-8.1%), mainly due to the difficulty of offsetting the amortizations of the program Reactiva Peru. Apart from the above, very dynamic performance of consumer loans (+26.3%) and credit cards (+43.2%). In the quarter, the NPL ratio fell slightly to 4.9%, below the level at the end of 2021, favored by recoveries and write-offs management. For its part, the NPL coverage ratio increased compared to the previous quarter and stood at 91%, also below the level at the end of 2021. During the fourth quarter, consumer and credit cards portfolios increased by 2.5% and 8.8%, respectively, while business loans continued to show an unfavorable evolution (-3.3%).

- Customers funds under management increased by 2.2% during the year 2022, due to the favorable performance of time deposits (+84.9%), supported by the rise in benchmark rates by the central bank, which offset lower balances in demand deposits (-10.9%) and in off-balance sheet funds (-19.9%). In the fourth quarter, the customer deposits recorded a decline compared to the previous quarter (-6.6%) as a result of the preference for liquidity in a turbulent sociopolitical environment of the country at the end of the year.

- BBVA Peru's net attributable profit stood at €206m at the end of December 2022, 53.1% higher than the figure achieved at the end of the previous year. During the year 2022, recurring income grew by 20.4%, thanks to the favorable evolution of the net interest income, which benefited from the increase in the customer spread and, to a lesser extent, commissions. On the lower part of the income statement, higher operating expenses (+15.8%) -without an efficiency ratio deterioration, which improved 96 basis points in the year- and lower provisions for impairment on financial assets (-1.4%) were recorded. In the fourth quarter, BBVA's net interest income in Peru continued to show a positive evolution (+6.2%), due to the higher yield on the excess liquidity and activity evolution, which did not offset the increase in both provisions for impairments on financial assets -mainly due to the needs of the Reactiva group- and operating expenses, due to a higher variable remuneration to employees, in line with the improved result reached in the year. Thus, the result generated between October and December was 25.9% lower than the one of the previous quarter.