Counterparty exposure involves that part of the original exposure corresponding to derivative instruments, repurchase and resale transactions, securities or commodities lending or borrowing transactions and deferred settlement transactions.

4.3.1. Policies on managing counterparty risk

4.3.1.1. Methodology: allocation of internal capital and limits to exposures subject to counterparty risk

The Group has an economic model for calculating internal capital through exposure to counterparty risk in treasury operations. This model has been implemented in the Risk unit systems in Market areas. It is used to measure the credit exposures for each of the counterparties for which the entity operates.

The generation of exposures is undertaken in a manner that is consistent with those used for the monitoring and control of credit risk limits. The time horizon is divided up into intervals, and the market risk factors (interest rates, exchange rates, etc.) underlying the instruments that determine their valuation are simulated for each interval. The exposures are generated from 500 different scenarios using the Monte Carlo method for risk factors (subject to counterparty risk) and applying the corresponding mitigations to each counterparty (in other words, applying collateral and/or netting agreements as applicable.

The correlations, loss given defaults, internal ratings and associated probabilities of default are consistent with the Group’s economic model for general credit risk.

The capital for each counterparty is then calculated using the exposure profile and taking into account the analytical formula adopted by Basel. This figure is modified by an adjustment factor for the possible maturity subsequent to one year of the operations in a similar vein to the general approach adopted by Basel for the treatment of credit risk.

Counterparty limits are specified within the financial programs authorized for each subsidiary within the line item of treasury limits. It stipulates both the limit and the maximum term for the operation. The use of transactions within the limits is measured in terms of mark-to-market valuation plus the potential risk with Monte Carlo Simulation methodology (95% confidence level) and bearing in mind possible mitigating factors (such as netting, break clauses or collateral contracts).

Management of consumption by lines in the Markets area is carried out through a corporate platform that enables online monitoring of the limits and availabilities established for the different counterparties and clients. This control is completed by independent units of the business area to guarantee proper segregation of functions.

4.3.1.2. Policies for ensuring the effectiveness of collaterals and establishing the value adjustments for impairment to cover this risk

The Group has concluded collateral contracts with many of its counterparties that serve as a guarantee of the mark-to-market valuation of derivatives operations. The collateral consists mostly of deposits, which means that no situations of impairment are forthcoming.

A tool has been specifically designed to process and manage the collateral contracts concluded with counterparties. This application enables the management of collateral at the transaction level -useful for controlling and monitoring the status of specific operations- as well as at the position level by providing accumulated information according to different parameters or characteristics. Furthermore, said tool feeds the applications responsible for estimating counterparty risk by providing all the necessary parameters for considering the impact of mitigation in the portfolio due to the agreements signed.

Likewise, there is also an application that reconciles and adjusts the positions serving the Collateral and Risks units.

In order to uphold the effectiveness of collateral contracts, the Group carries out a daily monitoring of the market values of the operations governed by such contracts and of the deposits made by the counterparties. Once the amount of the collateral to be delivered or received is obtained, the collateral demand (margin call), or the demand received, is carried out at the intervals established in the contract, usually daily. If significant variations arise from the process of reconciliation between the counterparties, they are reported by the Collateral unit to the Risks unit for subsequent analysis and monitoring. Within the control process, the Collateral unit issues a daily report on the guarantees which includes the description by counterparty of the exposure and collateral, making special reference to those guarantee deficits at or beyond the set warning levels.

4.3.1.3. Policies regarding the risk of adverse effects occurring due to correlations

Derivatives contracts may give rise to potential adverse correlation effects between the exposure to the counterparty and its credit quality (wrong-way-exposures). The Group has strict policies on the treatment of exposures of this nature. First, they follow specific admission processes for each individual operation; and second, they compute the effects of risk, not for the potential value of the exposure but for 100% of its nominal value.

4.3.1.4. Impact of collaterals in the event of a downgrade in their credit rating

In derivatives operations, as a general policy the Group does not subscribe collateral contracts that involve an increase in the amount to be deposited in the event of the Group being downgraded.

The general criterion applied to date with banking counterparties is to establish a zero threshold within collateral contracts, independently of the mutual rating provision will be made as collateral of any difference that arises through mark-to-market valuation, however small it may be.

4.3.2. Amounts of counterparty risk

The calculation of the original exposure for the counterparty risk of derivatives, according to Rule Seventy-One in Bank of Spain Circular 3/2008, can be made by means of the following methods: original risk, mark-to-market valuation, standardized and internal models.

The Group calculates solely the value of exposure to risk through the mark-to-market method obtained as the aggregate of the positive mark-to-market value after contractual netting agreements plus the potential future risk of each transaction or instrument.

There follows a specification of the amounts in million euros involved in the counterparty risk of derivatives as at December 31, 2012 and 2011:

| Derivatives counterparty risk | 2012 | 2011 |

|---|---|---|

| Gross positive fair value of the contracts | 53,616 | 49,989 |

| Add-on | 21,154 | 25,213 |

| Positive effects of netting agreements | 48,648 | 42,565 |

| Credit exposure after netting and before collateral assigned | 26,122 | 32,636 |

| Collateral assigned | 6,314 | 4,081 |

| Credit exposure in derivatives after netting and before collateral assigned | 19,808 | 28,555 |

The management of new netting and collateral agreements has reduced counterparty exposure.

The total exposure to counterparty risk, composed basically of repo transactions and OTC derivatives, is €66,633 million and €109,581 million, as of December 31, 2012 and 2011 respectively (after applying any compensation agreements applicable).

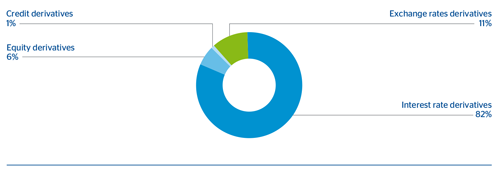

Below is the EAD for derivatives broken down by products:

2012

(Million euros)

| Products | Currency risk | Interest-rate risk | Equity risk | Commodity risk | Credit risk | Other risks | TOTAL |

|---|---|---|---|---|---|---|---|

| Term operations | 1,652 | 51 |

|

|

|

|

1,703 |

| FRAs |

|

126 | 312 | 2 |

|

|

441 |

| Swaps | 484 | 14,361 | 144 | 25 |

|

|

15,014 |

| Options | 55 | 1,555 | 795 | 4 |

|

10 | 2,419 |

| Other products |

|

31 |

|

|

201 |

|

231 |

| TOTAL | 2,191 | 16,123 | 1,252 | 32 | 201 | 10 | 19,808 |

EAD for derivatives by product

4.3.2.1. Operaciones con derivados de crédito

The table below shows the amounts corresponding to transactions with credit derivatives used in intermediation activities:

As of December 31, 2012 and 2011 the Group did not hold any credit derivatives for use in its own lending portfolio.

2012

(Million euros)

|

|

|

Types of derivatives | |||

|---|---|---|---|---|---|

| Classification of derivatives | Total notional amount of the transactions | On individual names (CDS) | On indexes (CDSI) | Nth to default baskets | Derivatives on tranches (CDO) |

| Protection purchased | 23,700 | 12,841 | 9,373 | 930 | 557 |

| Protection sold | 23,969 | 13,931 | 9,386 | 85 | 567 |

2011

(Million euros)

|

|

|

Types of derivatives | |||

|---|---|---|---|---|---|

| Classification of derivatives | Total notional amount of the transactions | On individual names (CDS) | On indexes (CDSI) | Nth to default baskets | Derivatives on tranches (CDO) |

| Protection purchased | 44,159 | 16,232 | 26,313 | 986 | 628 |

| Protection sold | 43,422 | 16,630 | 26,122 | 10 | 659 |