Non Core Real Estate

Highlights

- Positive trend in Spanish real-estate sector figures continues.

- Agreement with Cerberus for the transfer of real-estate assets to a new company and subsequent sale of 80% of this company to Cerberus.

- Further decline in net exposure, NPLs and losses.

Industry trends

The real-estate market remains on an upward path. According to the latest available information from the Quarterly National Accounting for the third quarter of 2017, investment in housing increased by 0.7% over the previous quarter.

The most recent data from the General Council of Spanish Notaries (CIEN) shows that 432,500 homes were sold in Spain during the first ten months of 2017, a year-on-year increase of 16.4%. This trend reflects the growth of the economy and its capacity to generate employment, against a backdrop of low interest rates that is boosting new lending for home purchases. In addition, household confidence in the future of the economy has remained relatively high.

Growth of demand in a context of declining housing stock once more resulted in an increase in price in the third quarter of 2017: According to data from the INE for the close of the third quarter, housing prices increased by 6.6% in year-on-year terms, one percentage point more than in the previous quarter. This is also the biggest rate of growth since the series was created in the first quarter of 2007.

Monetary policy has continued to maintain the cost of finance at relatively low levels, which has encouraged people to take out mortgage loans. The 12-month Euribor hit a new low in December (-0.190%). New residential mortgage lending, without stripping out refinancing, increased by 16.4% year-on-year in the first eleven months of the year, according to data from the Bank of Spain. Taking into account refinancing, new lending increased 1.7% in the same period.

Finally, construction activity is still responding to the positive impetus from demand. According to data from the Ministry of Public Works, nearly 68,100 new housing construction permits were approved from January to October 2017, up 28.0% on the figure from the same period in 2016.

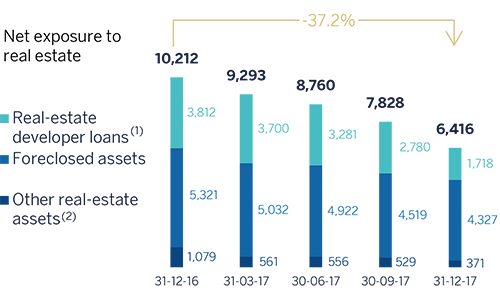

Evolution of Net exposure to real-estate

(Million euros)

- (1) Compared to Bank of Spain’s Transparency scope (Circular 5/2011 dated November 30), real-estate developer loans do not include €2.1 Bn (December 2017) mainly related to developer performing loans transferred to the Banking activity in Spain area.

- (2) Other real-estate assets not originated from foreclosures.

Coverage of real-estate exposure (Million euros as of 31-12-2017)

| Gross Value | Provisions | Net exposure | % Coverage | |

|---|---|---|---|---|

| Real-estate developer loans (1) | 3,146 | 1,428 | 1,718 | 45 |

| Performing | 530 | 15 | 515 | 3 |

| Finished properties | 462 | 12 | 449 | 3 |

| Construction in progress | 11 | 0 | 11 | 2 |

| Land | 44 | 2 | 41 | 5 |

| Without collateral and other | 13 | 1 | 13 | 6 |

| NPL | 2,616 | 1,412 | 1,203 | 54 |

| Finished properties | 1,285 | 588 | 697 | 46 |

| Construction in progress | 38 | 14 | 23 | 38 |

| Land | 1,056 | 658 | 398 | 62 |

| Without collateral and other | 237 | 152 | 85 | 64 |

| Foreclosed assets | 11,686 | 7,359 | 4,327 | 63 |

| Finished properties | 7,100 | 3,938 | 3,162 | 55 |

| Construction in progress | 541 | 359 | 182 | 66 |

| Land | 4,045 | 3,062 | 983 | 76 |

| Other real-estate assets (2) | 981 | 609 | 371 | 62 |

| Real-estate exposure | 15,813 | 9,396 | 6,416 | 59 |

- (1) Compared to Bank of Spain's Transparency scope (Circular 5/2011 dated November 30), real-estate developer loans do not include €2.1 Bn (December 2017) mainly related to developer performing loans transferred to the Banking activity in Spain area.

- (2) Other real-estate assets not originated from foreclosures.

Activity

BBVA has taken another highly significant step forward in its strategy of reducing real-estate exposure. In the fourth quarter of 2017, BBVA reached an agreement with a subsidiary of Cerberus to create a joint venture to which part of BBVA’s real-estate business in Spain will be transferred. The business includes: (i) foreclosed real-estate assets, as described in the Significant Event published on November 29, 2017, for a gross value of approximately €13 billion (based on their situation as of June 26, 2017); and (ii) the assets and employees needed to manage the activity in an autonomous manner. In executing this agreement, BBVA will transfer the business to a single company, and at the closing date of the transaction, it will sell 80% of the shares in the said company to Cerberus.

For the purpose of this agreement, the business has been valued at approximately €5 billion, so the sale of 80% of the shares would amount to €4 billion. The final price paid will be determined by the volume of assets actually provided, which may vary depending on factors such as sales between the reference date of June 26, 2017 and the closing date of the transaction, and compliance with the normal conditions for transactions of this type. At the close of the transaction, which is expected to take place in the second half of 2018, and once the volume of assets actually transferred is known, its final impact will be determined both in the net attributable profit and in the Group's capital ratios.

From the point of view of loans to developers, it is worth noting that in 2017, the outstanding performing portfolio was transferred from Non Core Real Estate to Banking Activity in Spain for an amount exceeding €1bn.

Thus, as of 31-Dec-2017, the net exposure to the real-estate sector of €6,416m was down by 37.2% in year-on-year terms, due basically to the wholesale operations carried out over the year. These figures include all the assets in the Cerberus agreement, which will not mean a reduction in exposure until the transaction has been completed.

With respect to sales, 25,816 units were sold in 2017 for a total sale price of €2,121m. This represents a significant increase on 2016, both in the number of units and price.

Total real-estate exposure, including loans to developers, foreclosed and other assets, was reflected in a coverage ratio of 59% at the end of December 2017. The coverage ratio of foreclosed assets rose to 63%, a relatively high percentage given the proportion of these assets on the balance sheet.

Non-performing loans fell again, thanks to a low volume of net additions to NPL over the period and the sale of a non-performing loan portfolio in the third quarter. The NPL coverage ratio closed 31-Dec-2017 at 56%.

Results

This business area posted a cumulative loss of €501m in 2017, compared with the loss of €595m in 2016. This illustrates a decline in losses, together with a very significant reduction in real-estate exposure.

Financial statements (Million euros)

| Income statement | 2017 | ∆% | 2016 |

|---|---|---|---|

| Net interest income | 71 | 19.5 | 60 |

| Net fees and commissions | 3 | (50.7) | 6 |

| Net trading income | 0 | n.s. | (3) |

| Other income/expenses | (91) | 33.2 | (68) |

| Gross income | (17) | 157.8 | (6) |

| Operating expenses | (115) | (7.1) | (124) |

| Personnel expenses | (63) | (4.5) | (66) |

| Other administrative expenses | (34) | 11.3 | (31) |

| Depreciation | (18) | (33.8) | (27) |

| Operating income | (132) | 1.2 | (130) |

| Impairment on financial assets (net) | (138) | 0.4 | (138) |

| Provisions (net) and other gains (losses) | (403) | (15.2) | (475) |

| Profit/(loss) before tax | (673) | (9.4) | (743) |

| Income tax | 170 | 15.4 | 148 |

| Profit/(loss) for the year | (502) | (15.6) | (595) |

| Non-controlling interests | 1 | n.s. | (0) |

| Net attributable profit | (501) | (15.8) | (595) |

| Balance sheet | 31-12-17 | ∆% | 31-12-16 |

|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 12 | 30.3 | 9 |

| Financial assets | 1,200 | 108.9 | 575 |

| Loans and receivables | 3,521 | (40.8) | 5,946 |

| of which loans and advances to customers | 3,521 | (40.8) | 5,946 |

| Inter-area positions | - | - | - |

| Tangible assets | 0 | - | 464 |

| Other assets | 4,981 | (25.9) | 6,719 |

| Total assets/liabilities and equity | 9,714 | (29.2) | 13,713 |

| Financial liabilities held for trading and designated at fair value through profit or loss | - | - | - |

| Deposits from central banks and credit institutions | - | - | - |

| Deposits from customers | 13 | (47.6) | 24 |

| Debt certificates | 785 | (5.8) | 834 |

| Inter-area positions | 5,775 | (39.3) | 9,520 |

| Other liabilities | (0) | (62.7) | (0) |

| Economic capital allocated | 3,141 | (5.8) | 3,335 |

| Memorandum item: | |||

| Risk-weighted assets | 9,691 | (10.8) | 10,870 |