Eurasia highlights in the fourth quarter

- Recovery of deposit gathering in the corporate segment.

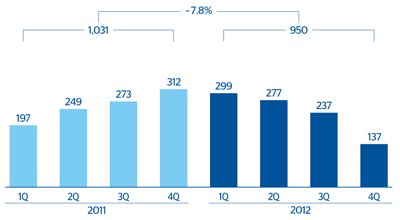

- Reduction in CIB portfolios.

- Good performance of Garanti and provisions in Portugal.

- Three new international distinctions reward the management of Garanti.

Industry Trends

In the fourth quarter of 2012, the macroeconomic environment in Europe continued to be very difficult, although clear progress was being made toward banking and fiscal integration. In fact, the first steps were taken to set up single banking supervision, which is considered key to breaking the link between sovereign and banking risk.

In Turkey, the prospects for a more moderate inflation rate, a steadily improving current-account deficit and a slight slowdown in growth of domestic demand, have in the second half of 2012 led to a fall in the official interest rate for the first time in a year and a reduction in the overnight rate. The year-on-year growth in lending has remained high (20%), although below the 2011 figures, and the NPA ratio remains low. Finally, it should be noted that in November Fitch credit rating agency upgraded Turkey from speculative (BB+) to investment grade (BBB–) with a stable outlook. Among the reasons given for this are the Turkish economy’s sound banking sector and favorable growth prospects in the medium and long term.

Finally, in China the financial sector plan was published in September, following on from the twelfth Five-Year Plan (2011-2015). This plan restates the intention to abolish interest-rate controls, promote financial innovation and bolster the framework of financial regulation. The Plan also establishes a goal of increasing the weight of the financial sector as a proportion of GDP in terms of added value from 4.4% in the last decade to 15% by 2015. In this context, growth in the banking sector remains relatively stable. However, the proportion of long-term loans has increased, reflecting the fact that credit flows are already moving toward public infrastructure projects and corporate investment.