South America

Highlights

- Good performance of lending activity and the acquisition of customer funds

- Favorable evolution of net interest income and NTI

- Year-on-year improvement of the efficiency ratio of the area at constant exchange rates

- Lower adjustment for hyperinflation in Argentina in the quarter

BUSINESS ACTIVITY (1)

(VARIATION AT CONSTANT EXCHANGE RATES COMPARED TO 31-12-23)

(1) Excluding repos.

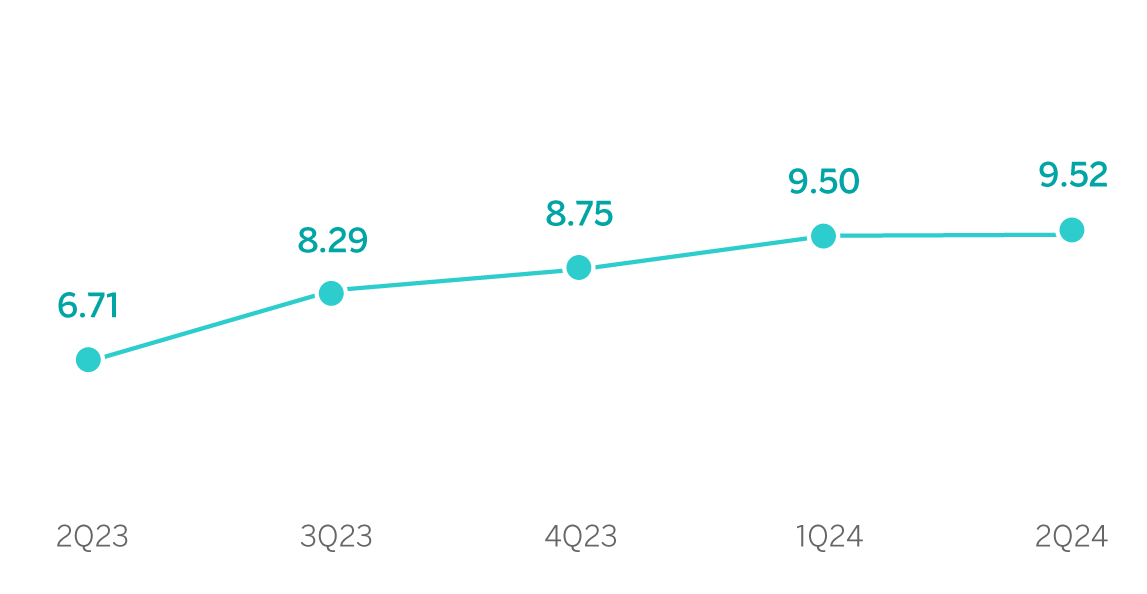

NET INTEREST INCOME / AVERAGE TOTAL ASSETS

(PERCENTAGE AT CONSTANT EXCHANGE RATES)

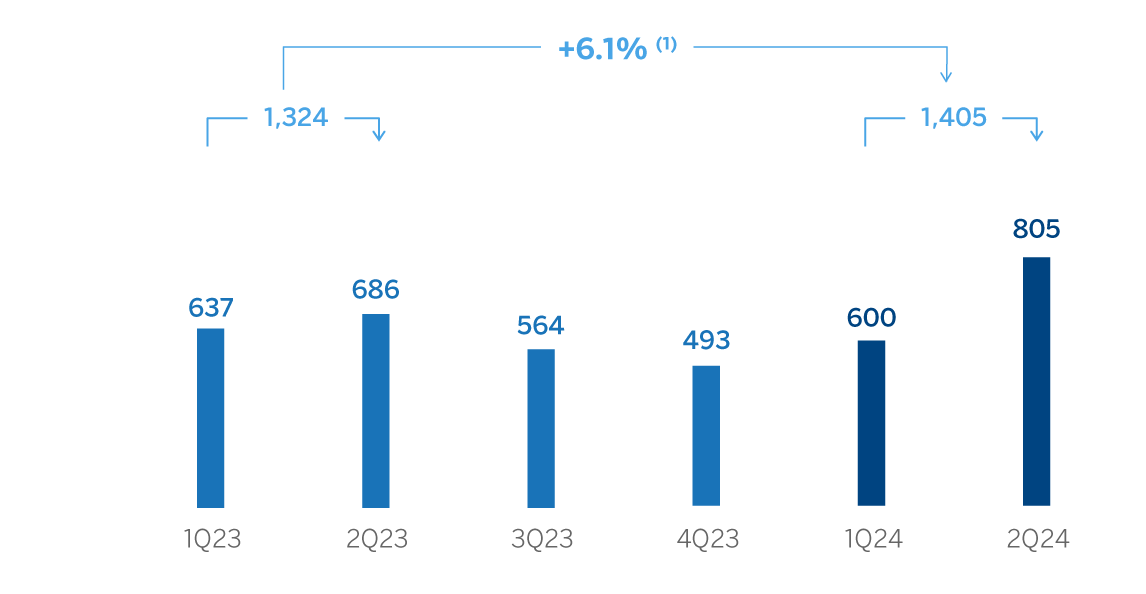

OPERATING INCOME

(MILLIONS OF EUROS AT CURRENT EXCHANGE RATES)

(1) At constant exchange rates: +83.2%.

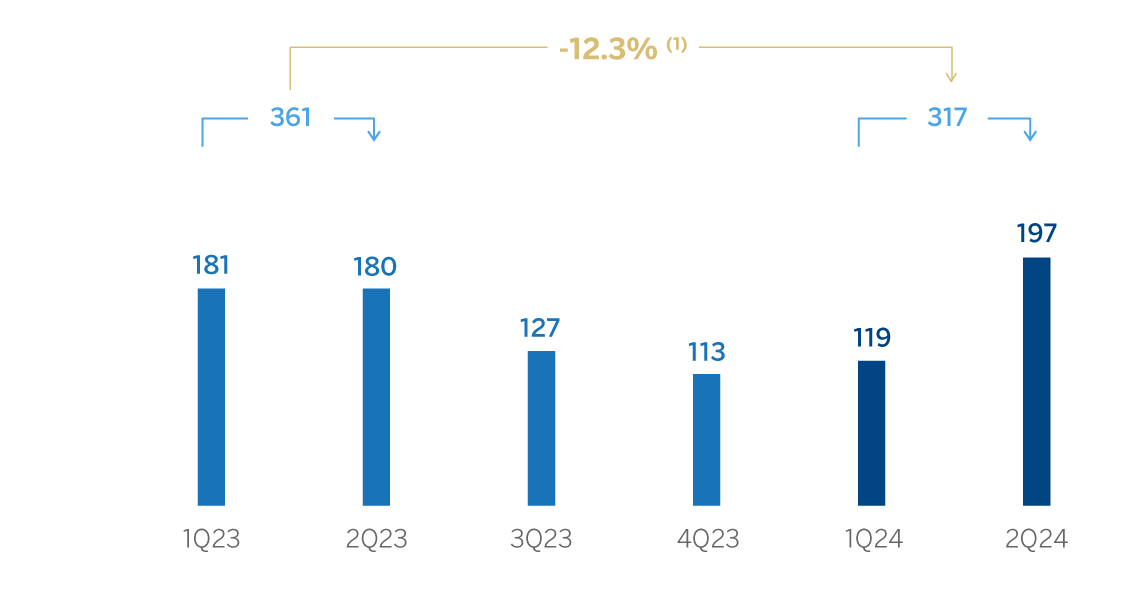

NET ATTRIBUTABLE PROFIT (LOSS)

(MILLIONS OF EUROS AT CURRENT EXCHANGE RATES)

(1) At constant exchange rates: +99.7%.

| FINANCIAL STATEMENTS AND RELEVANT BUSINESS INDICATORS (MILLIONS OF EUROS AND PERCENTAGE) | ||||

|---|---|---|---|---|

| Income statement | 1H24 | ∆ % | ∆ % (2) | 1H23 (1) |

| Net interest income | 3,075 | 22.8 | 73.9 | 2,503 |

| Net fees and commissions | 410 | (0.4) | 23.5 | 411 |

| Net trading income | 391 | 46.0 | 79.7 | 268 |

| Other operating income and expenses | (1,236) | 61.2 | 83.7 | (767) |

| Gross income | 2,639 | 9.3 | 60.5 | 2,415 |

| Operating expenses | (1,234) | 13.1 | 40.6 | (1,091) |

| Personnel expenses | (565) | 11.8 | 43.0 | (505) |

| Other administrative expenses | (566) | 13.9 | 42.8 | (497) |

| Depreciation | (103) | 15.6 | 19.6 | (89) |

| Operating income | 1,405 | 6.1 | 83.2 | 1,324 |

| Impairment on financial assets not measured at fair value through profit or loss | (755) | 40.2 | 60.4 | (539) |

| Provisions or reversal of provisions and other results | (25) | 87.8 | n.s. | (13) |

| Profit (loss) before tax | 625 | (19.0) | 111.9 | 772 |

| Income tax | (116) | (48.6) | 98.6 | (226) |

| Profit (loss) for the period | 509 | (6.8) | 115.2 | 546 |

| Non-controlling interests | (192) | 3.8 | 146.4 | (185) |

| Net attributable profit (loss) | 317 | (12.3) | 99.7 | 361 |

Balance sheets | 30-06-24 | ∆ % | ∆ % (2) | 31-12-23 |

| Cash, cash balances at central banks and other demand deposits | 7,061 | 7.2 | 10.4 | 6,585 |

| Financial assets designated at fair value | 10,763 | 2.4 | 5.6 | 10,508 |

| Of which: Loans and advances | 266 | (55.1) | (52.6) | 592 |

| Financial assets at amortized cost | 45,499 | 2.2 | 5.0 | 44,508 |

| Of which: Loans and advances to customers | 43,055 | 4.5 | 7.1 | 41,213 |

| Tangible assets | 1,187 | 26.4 | 27.5 | 939 |

| Other assets | 3,239 | 44.7 | 48.9 | 2,239 |

| Total assets/liabilities and equity | 67,749 | 4.6 | 7.5 | 64,779 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 2,090 | (36.4) | (33.4) | 3,289 |

| Deposits from central banks and credit institutions | 5,057 | (1.6) | 0.1 | 5,140 |

| Deposits from customers | 45,757 | 7.5 | 10.4 | 42,567 |

| Debt certificates | 3,075 | 3.0 | 6.7 | 2,986 |

| Other liabilities | 5,282 | 17.3 | 20.7 | 4,502 |

| Regulatory capital allocated | 6,488 | 3.1 | 6.2 | 6,294 |

Relevant business indicators | 30-06-24 | ∆ % | ∆ % (2) | 31-12-23 |

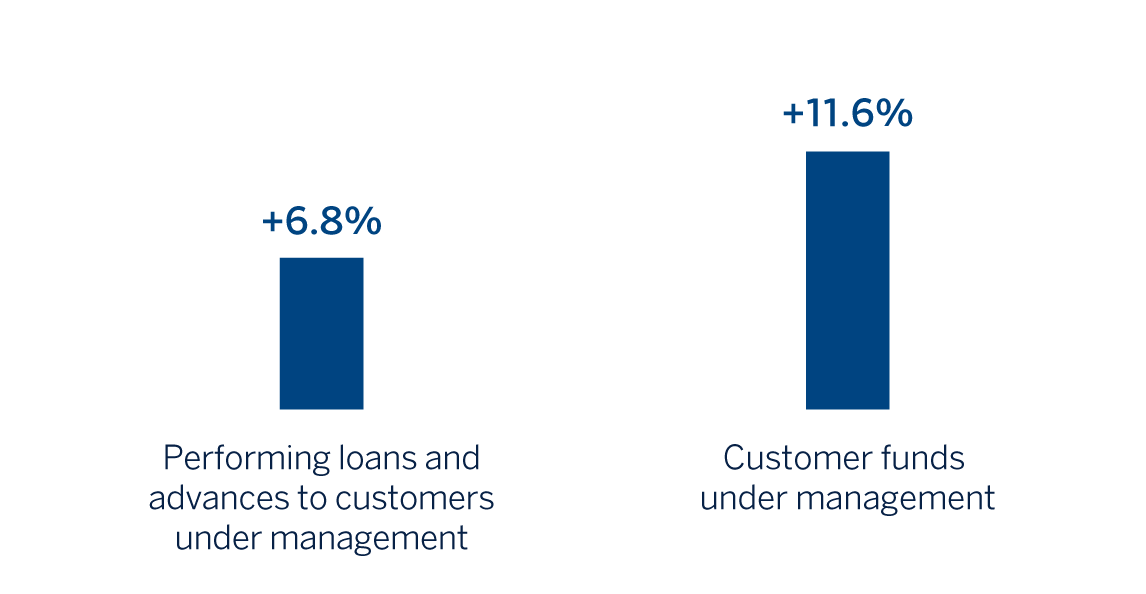

| Performing loans and advances to customers under management (3) | 42,719 | 4.2 | 6.8 | 41,013 |

| Non-performing loans | 2,471 | 7.3 | 9.6 | 2,302 |

| Customer deposits under management (4) | 45,757 | 7.5 | 10.4 | 42,567 |

| Off-balance sheet funds (5) | 6,378 | 15.4 | 20.8 | 5,525 |

| Risk-weighted assets | 52,338 | 6.6 | 9.4 | 49,117 |

| Efficiency ratio (%) | 46.8 | 45.0 | ||

| NPL ratio (%) | 5.0 | 4.8 | ||

| NPL coverage ratio (%) | 83 | 88 | ||

| Cost of risk (%) | 3.12 | 2.51 | ||

(1) Revised balances. For more information, please refer to the “Business Areas” section.

(2) At constant exchange rate.

(3) Excluding repos.

(4) Excluding repos and including specific marketable debt securities.

(5) Includes mutual funds, customer portfolios in Colombia and Peru.

| SOUTH AMERICA. DATA PER COUNTRY (MILLIONS OF EUROS) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

Country | |||||||||

| 1H24 | ∆ % | ∆ % (1) | 1H23 (2) | 1H24 | ∆ % | ∆ % (1) | 1H23 (2) | ||

| Argentina | 337 | (11.6) | n.s. | 381 | 103 | 4.5 | n.s. | 99 | |

| Colombia | 323 | 28.1 | 9.3 | 252 | 57 | (39.7) | (48.5) | 94 | |

| Peru | 630 | 18.7 | 18.5 | 530 | 110 | 1.2 | 1.0 | 109 | |

| Other countries (3) | 116 | (27.6) | (24.3) | 160 | 47 | (21.7) | (20.1) | 60 | |

| Total | 1,405 | 6.1 | 83.2 | 1,324 | 317 | (12.3) | 99.7 | 361 | |

(1) Figures at constant exchange rates.

(2) Revised balances. For more information, please refer to the “Business Areas” section.

(3) Chile (Forum), Uruguay and Venezuela. Additionally, it includes eliminations and other charges.

| SOUTH AMERICA. RELEVANT BUSINESS INDICATORS PER COUNTRY (MILLIONS OF EUROS) | ||||||||

|---|---|---|---|---|---|---|---|---|

| 30-06-24 | 31-12-23 | 30-06-24 | 31-12-23 | 30-06-24 | 31-12-23 | |||

| Performing loans and advances to customers under management (1) (2) | 3,944 | 2,066 | 16,294 | 16,084 | 17,822 | 17,257 | ||

| Non-performing loans (1) | 65 | 35 | 937 | 846 | 1,290 | 1,208 | ||

| Customer deposits under management (1) (3) | 6,119 | 3,714 | 17,713 | 16,960 | 17,884 | 17,015 | ||

| Off-balance sheet funds (1) (4) | 1,944 | 1,321 | 2,387 | 2,378 | 2,044 | 1,580 | ||

| Risk-weighted assets | 7,644 | 4,997 | 19,100 | 19,467 | 19,586 | 18,825 | ||

| Efficiency ratio (%) | 57.6 | 54.1 | 46.8 | 47.5 | 35.0 | 36.7 | ||

| NPL ratio (%) | 1.6 | 1.6 | 5.3 | 4.8 | 5.8 | 5.5 | ||

| NPL coverage ratio (%) | 126 | 136 | 84 | 89 | 77 | 84 | ||

| Cost of risk (%) | 4.29 | 2.18 | 2.83 | 2.13 | 3.49 | 3.04 | ||

(1) Figures at constant exchange rates.

(2) Excluding repos.

(3) Excluding repos and including specific marketable debt securities.

(4) Includes mutual funds and customer portfolios (in Colombia and Peru).

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and results, will be given at constant exchange rates. These rates, together with the changes at current exchange rates, can be found in the attached tables of the financial statements and relevant business indicators.

Activity and results

The most relevant aspects related to the area's activity during the first half of the year 2024 were:

- Lending activity (performing loans under management) increased by 6.8%, with the increase focused on the wholesale portfolio, which grew more than the retail portfolio (+8.4% versus +5.1%), mainly favored by the evolution of commercial loans which increased by +8.8%. In the retail portfolio, the growth of credit cards (+18.5%) and mortgage loans (+5.0%) stood out, in line with Group BBVA's strategy which is focused in growing in the most profitable segments.

- Customer funds under management increased (+11.6%) compared to the closing balances at the end of 2023, with an increase both in customer deposits (+10.4%) and off-balance sheet funds (+20.8%).

The most relevant aspects related to the area's activity during the second quarter of the year 2024 have been:

- Lending activity grew by 4.5%, with the same dynamics that explain the evolution of the semester: the dynamism of commercial loans (+5.9%), credit cards (+10.8%) and mortgage loans (+2.8%) stand out.

- With regard to asset quality, the NPL ratio at regional level stood at 5.0%, remaining practically stable with respect to the previous quarter (+4 basis points), favored by the activity evolution. In general, and excluding this effect, the trend of the last few months continues in terms of additions to non-performing loans, which remain mostly focused on the retail portfolio. For its part, the NPL coverage ratio, stood at 83%.

- Customer funds under management increased by 7.6%, supported by higher balances of time deposits (+9.9%), the increase of demand deposits (+5.4%) and, to a lesser extent, the evolution of off-balance sheet funds (+11.1%).

South America generated a cumulative net attributable profit of €317m at the end of the first half of 2024, which represents a year-on-year increase of 99.7%, driven by the good performance of recurring income (+65.9%) and the net trading income, which offset the increase in expenses and the more negative impact of "Other operating income and expenses". This line mainly includes the impact of the adjustment for hyperinflation in Argentina, whose net monetary loss stood at €1,020m in the period from January-June 2024, which is higher than the €571m registered in the period from January-June 2023.

More detailed information on the most representative countries of the business area is provided below.

Argentina

Macro and industry trends

The significant fiscal consolidation, relative exchange rate stability and the sharp contraction in economic activity have led to a gradual moderation of inflation in recent months. Despite the uncertainty and related risks, it is likely, according to BBVA Research, that ongoing adjustments, eventually complemented by additional measures, could set the bases for an inflation slowdown continuation along the year. On the other hand, although the sharp deterioration of economic activity could be reversed by mid-year if the adjustment plan is successful, it is expected that, after falling by 1.6% in 2023, GDP will be decrease by 4.0% in 2024 (unchanged since the last forecast).

The banking system continues to grow at a stable pace but is affected by high inflation. At the end of June 2024, total credit had grown by 211% compared to the same month in 2023, favored by both consumer and corporate portfolios above all, which reached year-on-year growth rates of 182% and 252% year-on-year, respectively. On the other hand, deposits continued the trend of the previous months and had grown by 144% year-on-year at the end of June. Finally, the NPL ratio improved significantly to 1.8% as of April 2024 (123 basis points below the level of May 2023).

Activity and results

- In the first half of 2024, performing loans under management increased by 90.9%, (+45.4% in the second quarter, with growth in all products), although still well below the year-on-year inflation rate, showing positive evolution in both the corporates portfolio (+97.9%, mainly corporates) and the households portfolio (+83.1%), highlighting in the latter the growth in credit cards (+71.1%). In the second quarter, the NPL ratio stood at 1.6%, remaining stable with respect to the previous quarter (-2 basis points in the quarter), thanks to the positive dynamic of the activity. On the other hand, the NPL coverage ratio stood at 126%, far below the end of March 2024, as a result of the increase in entries to non performing loans in the retail portfolio (mainly in credit cards and consumer).

- Balance sheet funds grew by 64.7% between January and June 2024 (+25.6% in the second quarter), with growth of both demand deposits (+44.3%) and time deposits (+122.9%). Mutual funds (off-balance resources) also had a good performance (+47.2% in the same period).

- The cumulative net attributable profit at the end of June 2024 stood at €103m. Net interest income continued to be driven by both higher activity and better customer spreads. For its part, NTI registered a positive evolution. On the other hand, there was a more negative adjustment for hyperinflation (mainly reflected in the other operating income and expenses line) and higher expenses, both in personnel due to salary revisions in a context of high inflation, and general expenses. The profit of the quarter stood at €82m, which is a significant improvement compared to the previous quarter, as a result of a less negative hyperinflation adjustment.

Colombia

Macro and industry trends

After a period of weakness in economic activity, during the year 2023 and to some extent also at the beginning of 2024, BBVA Research forecasts a recovery starting in the middle of this year. A further decrease in inflation, which reached 7.2% in June and would fall to around 5.4% in December, and in interest rates, from 11.25% in June to around 8.5% in December, would likely allow GDP growth to increase to 1.8% this year (+30 basis points above the previous forecast, mainly due to the first quarter data, which surprised upwards) from 0.6% in 2023.

Total credit growth for the banking system stood at 0.9% year-on-year in April 2024. As in previous months, system's credit continues to be driven by the growth in corporate lending and mortgages at 2.0% and 11.3% respectively. Noteworthy is the slowdown in consumer credit, which changed from a year-on-year growth rate of 20% during 2022, to year-on-year decreases since October 2023. In April 2024, consumer credit has decreased by 4.3% compared to the same month in 2023. On the other hand, total deposits showed a year-on-year growth rate of 9.9% year-on-year at the end of April 2024, with a much more balanced development in portfolios than in previous quarters. Thus, demand and time deposits grew by 8.2% and 12.0% year-on-year respectively. The NPL ratio of the system has increased slightly in recent months to 5.3% at the end of April 2024, 69 basis points higher than in the same month of 2023.

Activity and results

- Lending activity grew 1.3% compared to the end of 2023, mainly due to the favorable evolution during the second quarter of 2024 in corporate loans (+6.6%, +7.6% from December 2023) and mortgage loans (+1.4%, +1.9% from December 2023). that offset the reduction in consumer loans (-2.0%, -3.9% from December 2023). In terms of asset quality, in the second quarter, the NPL ratio stood at 5.3%, increasing compared to the previous quarter (+16 basis points), affected by the NPL entries in the retail portfolio, mainly in the consumer loans, and, to a lesser extent, in credit cards. For its part, the NPL coverage ratio reduced in the quarter to 84% due to the new NPL inflows as mentioned.

- Customer deposits increased by 4.4% compared to the end of 2023, mainly thanks to the favorable evolution of demand deposits (+5.4%, +6.9% in the second quarter).

- The cumulative net attributable profit at the end of June 2024 stood at €57m, that is 48.5% below the result of the same period of the previous year. The significant growth of the net interest income (+22.4%) stood out, favored by the increase in the customer spread accompanied by a greater volume of deposits and a good performance of the securities portfolio, compensated by the provisions for impairment on financial assets, due to higher portfolio requirements (especially in retail). The profit of the quarter stood at €37m, 85.8% above the previous quarter, as a result of good performance of recurring income, where the 21.3% growth in net fees and commissions stands out (favored by the revenues of Project Finance fees and Investment Banking fees and other atypical elements), lower operating expenses, impairments on financial assets and provisions.

Peru

Macro and industry trends

BBVA Research expects economic activity to continue to recover in 2024, a context of more favorable weather conditions and relatively high prices for the country's exports (particularly metals such as copper). Relatively controlled inflation (2.3% in June, and probably around this level in the second half of 2024) and the gradual reduction of interest rates (from 5.75% in June to around 5.00% in December 2024) should also favor an increase in economic dynamism in the next months. Thus, GDP is expected to grow by around 2.9% this year, 20 basis points above the previous forecast and well above the evolution observed in 2023 (-0.6%).

Total credit in the Peruvian banking system fell by 0.5% year-on-year in May 2024. Performance by portfolios is uneven, with the biggest slowdown in corporate lending, with a year-on-year contraction of 2.5%. In contrast, consumer finance remained buoyant, growing by 0.6% year-on-year as of May 2024, while the mortgage portfolio maintained a stable growth rate of around 5.4% year-on-year, in line with previous months. Total deposits in the system increased at the end of May 2024 by 4.5% year-on-year, with very similar behavior for portfolios. The demand and time deposits grew by 4.8% and 3.9% year-on-year respectively. The NPL ratio across the banking system rose very slightly to 4.5%.

Activity and results

- Lending activity increased compared to the end of December 2023 (+3.3%), mainly due to the positive evolution of corporate loans (+2.7%, favored by CIB operations, and despite the expiration of the Reactiva Perú program), and consumer loans (+5.8%) and mortgages (+5.4%). In terms of credit quality indicators, the NPL ratio increased compared to March 2024 (+12 basis points) standing at 5.8%, as a result of an almost stable activity and NPL inflows in retail portfolio, mainly SMEs, partially mitigated by portfolio sales and write-offs. On the other hand, the NPL coverage ratio stood at 77%, impacted by the increase in NPLs.

- Customers funds under management increased during the first half of 2024 (+7.2%), boosted by both the good performance of customer deposits (+5.1%) and off-balance sheet funds (+29.4%).

- BBVA Peru's net attributable profit stood at €110m at the end of June 2024, in line with the figures achieved at the end of the first half of 2023. Good performance of the net interest income, favored by the higher volume of lending and a growing customer spread, fee income and NTI (with an outstanding quarterly performance thanks to the management of the ALCO portfolios), which together offset the increase in operating expenses, leading to double-digit gross margin growth. The increase of provisions for impairment of financial assets (+55.7%) stands out negatively, with higher requirements mainly due to the impairment of the retail portfolio and at the wholesale one, due to the effect of the cancellation of a one-time customer guarantee (neutral in results as the associated provision was released). The profit of the quarter stood at €67m, which is a variation of 57.8% compared to the previous quarter, mainly as a result of the significant growth in NTI and reduction in operating expenses.