Results

In the first half of 2017, BBVA has generated a net attributable profit of €2,306m, a year-on-year increase of 25.9%. This positive trend is explained by the good performance of more recurring revenues and the heading of other operating income and expenses, together with the control of operating expenses and a reduction in impairment losses on financial assets.

Unless expressly indicated otherwise, to better understand the changes in the main headings of the Group's income statement, the percentage changes given below refer to constant exchange rates.

Consolidated income statement: quarterly evolution (Million euros)

| 2017 | 2016 | |||||

|---|---|---|---|---|---|---|

| 2Q | 1Q | 4Q | 3Q | 2Q | 1Q | |

| Net interest income | 4,481 | 4,322 | 4,385 | 4,310 | 4,213 | 4,152 |

| Net fees and commissions | 1,233 | 1,223 | 1,161 | 1,207 | 1,189 | 1,161 |

| Net trading income | 378 | 691 | 379 | 577 | 819 | 357 |

| Dividend income | 169 | 43 | 131 | 35 | 257 | 45 |

| Share of profit or loss of entities accounted for using the equity method | (2) | (5) | 7 | 17 | (6) | 7 |

| Other operating income and expenses | 77 | 108 | 159 | 52 | (26) | 66 |

| Gross income | 6,336 | 6,383 | 6,222 | 6,198 | 6,445 | 5,788 |

| Operating expenses | (3,175) | (3,137) | (3,243) | (3,216) | (3,159) | (3,174) |

| Personnel expenses | (1,677) | (1,647) | (1,698) | (1,700) | (1,655) | (1,669) |

| Other administrative expenses | (1,139) | (1,136) | (1,180) | (1,144) | (1,158) | (1,161) |

| Depreciation | (359) | (354) | (365) | (372) | (345) | (344) |

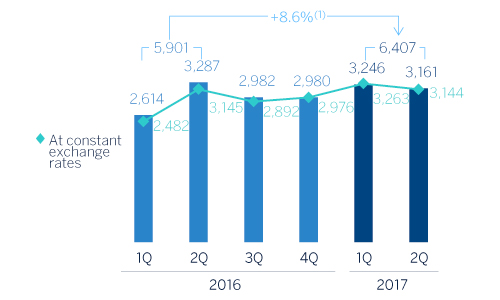

| Operating income | 3,161 | 3,246 | 2,980 | 2,982 | 3,287 | 2,614 |

| Impairment on financial assets (net) | (997) | (945) | (687) | (1,004) | (1,077) | (1,033) |

| Provisions (net) | (193) | (170) | (723) | (201) | (81) | (181) |

| Other gains (losses) | (3) | (66) | (284) | (61) | (75) | (62) |

| Profit/(loss) before tax | 1,969 | 2,065 | 1,285 | 1,716 | 2,053 | 1,338 |

| Income tax | (546) | (573) | (314) | (465) | (557) | (362) |

| Profit/(loss) for the year | 1,422 | 1,492 | 971 | 1,251 | 1,496 | 976 |

| Non-controlling interests | (315) | (293) | (293) | (286) | (373) | (266) |

| Net attributable profit | 1,107 | 1,199 | 678 | 965 | 1,123 | 709 |

| Earning per share (euros) (1) | 0.16 | 0.17 | 0.09 | 0.13 | 0.16 | 0.10 |

- (1) Adjusted by additional Tier 1 instrument remuneration.

Consolidated income statement (Million euros)

| 1H17 | ∆% | ∆% at constant exchange rates | 1H16 | |

|---|---|---|---|---|

| Net interest income | 8,803 | 5.2 | 9.6 | 8,365 |

| Net fees and commissions | 2,456 | 4.5 | 8.0 | 2,350 |

| Net trading income | 1,069 | (9.1) | (2.4) | 1,176 |

| Dividend income | 212 | (29.6) | (29.5) | 301 |

| Share of profit or loss of entities accounted for using the equity method | (8) | n.s. | n.s. | 1 |

| Other operating income and expenses | 185 | n.s. | 97.7 | 40 |

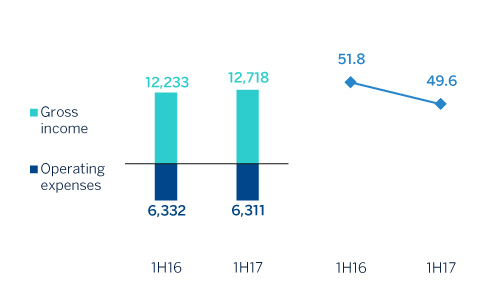

| Gross income | 12,718 | 4.0 | 7.8 | 12,233 |

| Operating expenses | (6,311) | (0.3) | 2.2 | (6,332) |

| Personnel expenses | (3,324) | (0.0) | 2.2 | (3,324) |

| Other administrative expenses | (2,275) | (1.9) | 1.0 | (2,319) |

| Depreciation | (712) | 3.4 | 6.3 | (689) |

| Operating income | 6,407 | 8.6 | 13.9 | 5,901 |

| Impairment on financial assets (net) | (1,941) | (8.0) | (4.9) | (2,110) |

| Provisions (net) | (364) | 38.6 | 32.1 | (262) |

| Other gains (losses) | (69) | (50.0) | (51.1) | (137) |

| Profit/(loss) before tax | 4,033 | 18.9 | 27.2 | 3,391 |

| Income tax | (1,120) | 21.8 | 32.9 | (920) |

| Profit/(loss) for the year | 2,914 | 17.9 | 25.2 | 2,471 |

| Non-controlling interests | (607) | (5.0) | 7.7 | (639) |

| Net attributable profit | 2,306 | 25.9 | 30.8 | 1,832 |

| Earning per share (euros) (1) | 0.33 | 0.26 |

- (1) Adjusted by additional Tier 1 instrument remuneration.

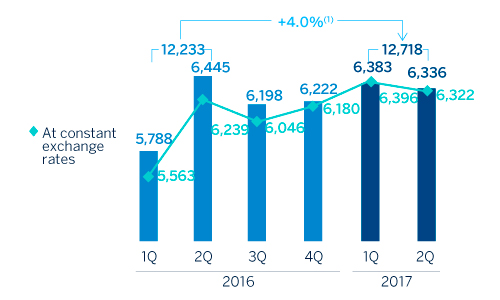

Gross income

Cumulative gross income grew 7.8% year-on-year, again strongly supported by the positive performance of the more recurring items.

Gross income (Million euros)

(1) At constant exchange rates: +7.8%.

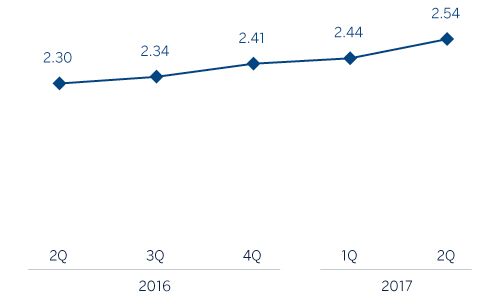

Net interest income grew 9.6% year-on-year and 3.3% over the quarter. Once more, the trend can be explained by the growth in activity in emerging economies and good management of customer spreads. Performance was positive in all the business areas except for Banking activity in Spain, where the current environment of very low interest rates, lower volumes of activity and sales in the wholesale portfolios have had a negative impact on performance.

Net interest income/ATA (Percentage)

First-half net fees and commissions have also performed well year-on-year in all the Group's areas, strongly influenced by good diversification, the recovery of activity in the wholesale businesses and fees from asset management, credit cards and online banking.

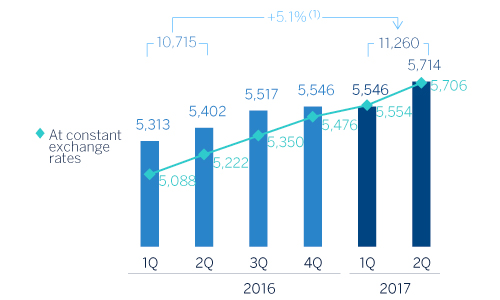

As a result, more recurring revenues (net interest income plus fees and commissions) have increased 9.2% year-on-year (2.7% over the last three months).

Net interest income plus fees and commissions (Million euros)

(1) At constant exchange rates: +9.2%.

The positive contribution of NTI has moderated in the half-year compared with the same period in 2016. This is mainly because capital gains of €204m before tax from the sale on the market of 1.7% of China Citic Bank (CNCB) in the first quarter of the year are lower than those from the VISA transaction booked in the same period last year (€225m).

The dividend income heading mainly includes dividends from the Group's stake in the Telefónica Group (€53m). The amount is lower than that paid in the second quarter of 2016 as a result of the reduction of the dividend paid by the entity (from €0.4 to €0.2 per share). In 2016 it also included those from CNCB.

Finally, other operating income and expenses have grown 97.7% year-on-year as a result of the positive contribution of the insurance business (up 14.4% in the last twelve months) due to the improvement in both written premiums and claims on the same period in 2016. In addition, this line includes the annual contribution of €100m in the second quarter to the Single Resolution Fund (SRF) (€122m in the same period of 2016).

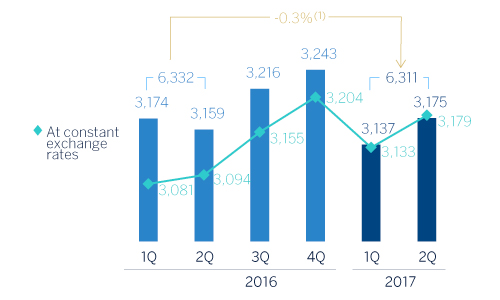

Operating income

The year-on-year increase in operating expenses continues limited, and stands at 2.2%. The above is due to the cost discipline implemented in all the areas of the Group through "efficiency" plans that are beginning to deliver results, and the materialization of some synergies (mainly those resulting from the integration of Catalunya Banc - CX). By business area there has been a reduction in Spain (where in May 59 branches were closed in addition to the 129 in February), the Rest of Eurasia and the Corporate Center, and an increase close to inflation levels in the rest of the geographic areas.

Operating expenses (Million euros)

(1) At constant exchange rates: +2.2%.

Breakdown of operating expenses and efficiency calculation (Million euros)

| 1H17 | ∆% | 1H16 | |

|---|---|---|---|

| Personnel expenses | 3,324 | (0.0) | 3,324 |

| Wages and salaries | 2,590 | 0.1 | 2,587 |

| Employee welfare expenses | 478 | (1.0) | 482 |

| Training expenses and other | 256 | 0.5 | 255 |

| Other administrative expenses | 2,275 | (1.9) | 2,319 |

| Property. fixtures and materials | 528 | (3.4) | 547 |

| IT | 499 | 4.6 | 477 |

| Communications | 149 | (1.4) | 151 |

| Advertising and publicity | 186 | (9.3) | 205 |

| Corporate expenses | 51 | (1.9) | 52 |

| Other expenses | 625 | (5.2) | 659 |

| Levies and taxes | 237 | 4.0 | 228 |

| Administration costs | 5,599 | (0.8) | 5,644 |

| Depreciation | 712 | 3.4 | 689 |

| Operating expenses | 6,311 | (0.3) | 6,332 |

| Gross income | 12,718 | 4.0 | 12,233 |

| Efficiency ratio (operating expenses/gross income; %) | 49.6 | 51.8 |

Number of employees

Number of ATMs

Number of branches

As a result of the above, the efficiency ratio stands at 49.6% (51.8% in the first half of 2016 and 51.9% for the whole of 2016), and the operating income has risen 13.9% in the last twelve months.

Efficiency (Million euros) and efficiency ratio (Percentage)

Operating income (Million euros)

(1) At constant exchange rates: +13.9%.

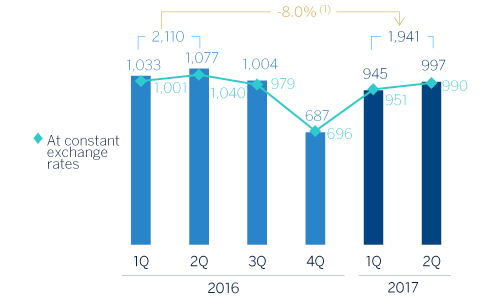

Provisions and other

Impairment losses on financial assets totaled €1,941m in the first half of the year, below the amount for the first six months of last year. By areas there was a year-on-year reduction in Spain, where the loan-loss provisioning requirements were lower; the United States, as in the first quarter of the previous year provisions were included following the rating downgrades of some companies belonging to the energy and metals & mining sectors; and, to a lesser extent, Turkey. In contrast, Mexico and South America have reported increases over the last twelve months, largely related to the increase in lending activity, and to a lesser extent, to the impact of increased requirements for insolvency provisions associated with some wholesale customers in the case of South America.

Impairment on financial assests (net) (Million euros)

(1) At constant exchange rates: -4.9%.

Finally, there was also a slight increase in the allocation to provisions (net) and other gains (losses) (up 4.0% year-on-year), which include the provisions for contingent liabilities, contributions to pension funds and provisions for buildings and foreclosed assets, among others. This increase is mainly explained by higher restructuring costs, basically affecting Banking activity in Spain, the area where increasing efficiency is a priority focus.

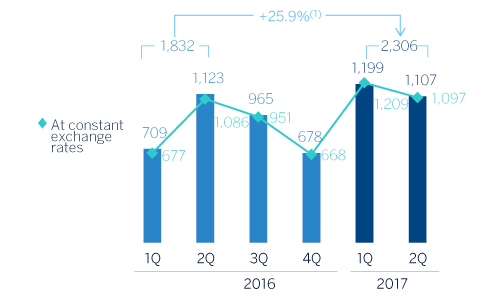

Results

As a result of the above, the Group's net attributable profit has been very positive (up 30.8% year-on-year). It is important to note that since March 2017 this figure has included the additional stake of 9.95% in the capital of Garanti, which has made a positive impact of around €54m of less non-controlling interests.

By business area, Banking activity in Spain has generated a profit of €670m, Non Core Real Estate generated a loss of €191m, the United States contributed €297m, Mexico €1,080m, Turkey €374m, South America €404m and the Rest of Eurasia €73m.

Net attributable profit (Million euros)

(1) At constant exchange rates: +30,8%.

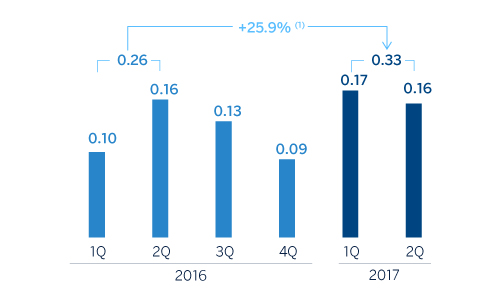

Earnings per share (1) (Euros)

(1) Adjusted by additional Tier 1 instrument remuneration.

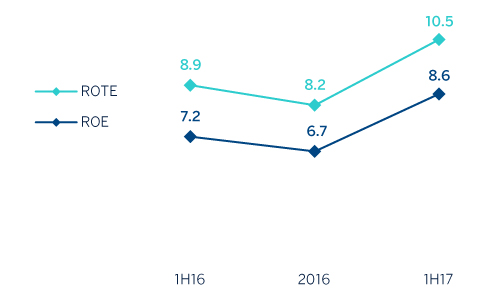

ROE and ROTE (1) (Percentage)

(1) The ROE and ROTE ratios include in the denominator the Group’s average shareholders’ funds, but do not take into account the caption within total equity named “Accumulated other comprehensive income” with an average balance of -€4,218m in 1H 2016, -€4,492m in 2016 and -€6,015 in 1H 2017.

ROA and RORWA (Percentage)